Office of Energy

Research and Development

Aussi disponible en français sous le titre : Approche stratégique visant l’innovation des batteries

For information regarding reproduction rights, contact Natural Resources Canada

at copyright-droitdauteur@nrcan-rncan.gc.ca.

Cat. No. M159-22/2024E-PDF / ISBN 978-0-660-73792-8

© His Majesty the King in Right of Canada, as represented by the Minister of Natural Resources, 2024

Table of Contents

- Preface

- Why a Strategic Approach

- Battery Innovation Context

- Strategic Approach to Battery Innovation

- Pillar#1: Supporting innovation that accelerates battery value chain decarbonization, security, and competitiveness

- Pillar #2: Supporting the development of world-class battery innovation infrastructure in Canada

- Pillar #3: Strengthening the network of Canadian battery innovators and help grow world-class Canadian firms in the battery value chain

- Battery Innovation Priorities

- Frameworks for Understanding Innovation Drivers

- Annex A: Stakeholder Innovation Opportunities

- References

Preface

This document complements the Office of Energy Research and Development (OERD) corporate planning and accountability processes, such as the Departmental Results Framework and Performance Information Profile, which articulate and align program objectives and activities with departmental core responsibilities, outcomes, and key priorities. This is intended to be an evergreen document to reflect current priorities and meet the evolving needs of the energy system.

Why a Strategic Approach

The energy system is complex and constantly changing. OERD employs “missions” to realize a clean energy future and a sustainable natural resources sector. Its main activities include funding clean energy projects and developing partnerships with stakeholders with the goals of reducing harmful emissions and supporting innovation and economic opportunities in the energy sector. Each OERD mission is comprised of energy technology focus areas listed in Figure 1. The Strategic Approach to Battery Innovation (SABI) pulls together elements of four focus areas serving two missions as identified below, in large part by advancing the science and technology cross cutting themes. The SABI provides a comprehensive articulation of OERD’s work in the battery innovation space for innovators from across academia, industry, and governments. The decision-making frameworks used to elaborate the SABI are shared for the benefit of other actors in Canada’s battery innovation ecosystem.

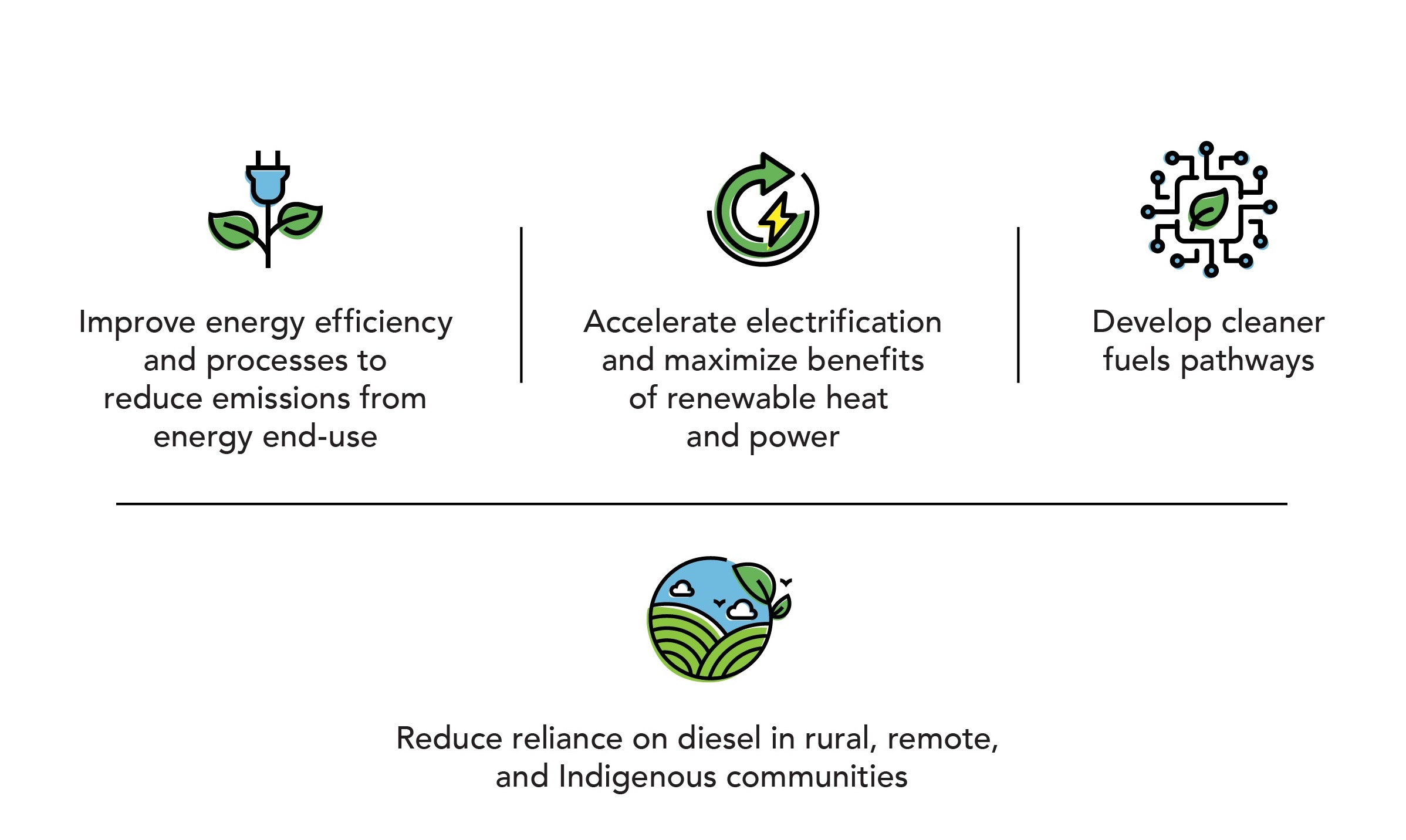

Figure 1: OERD’s missionsFootnote 1 and focus areas within the Battery Innovation Portfolio

Text version

OERD’s missions:

- Improve energy efficiency and processes to reduce emissions from energy end-use

- Accelerate electrification and maximize benefits of renewable heat and power

- Develop cleaner fuels pathways

- Reduce reliance on diesel in rural, remote, and Indigenous communities

Focus areas supporting these missions:

- Efficient Vehicles and Supporting Infrastructure

- Industrial Decarbonization

- Resilient Net-Zero Grid and Grid Readiness for Affordable Electrification

- Electrification of Transportation

Cross Cutting Themes:

- Advanced Materials and Manufacturing Processes

- Digitalization and Harnessing Data Science, Machine learning, & AI for Energy

- End of Life Impacts

- Non-Technical Barriers and Support to Policies, Markets and Regulations

- Net-Zero Pathway Modelling

- Affordable Energy Storage

Battery Innovation Context

The following context describes the high-level market dynamics and battery ecosystem characteristics which inform the interventions needed to advance innovation towards commercialization and growth of a highly innovative battery industry in Canada.

The impact of batteries on the energy transition

Several clean technologies will play important roles in the energy transition. Batteries are one of the few to have already made a significant difference by directly offsetting internal combustion engine vehicle emissions and facilitating electricity emission reductions. Because batteries can accept, store, and release electrical energy on demand, they represent a highly flexible and valuable tool for maintaining clean and reliable energy. With global cumulative battery demand from road transport alone set to increase 90-fold from 2023 to 2050 to stay on track for net-zero by 2050,Footnote 2 without innovative solutions the ability for the supply chain to meet demand will become increasingly strained.

In 2023, global electric vehicle (EV) sales reached 14 million units, representing 18% of all new cars sold worldwide.Footnote 2 In the same year, global stationary storage capacity installations approached 100 GWh with 21% compounded annual growth expected to 2030.Footnote 3 In Canada, 185,000 EVs were sold in 2023, representing a 11% share of new domestic cars sales,Footnote 2 and stationary storage installations increased by more than 50% over the previous year to 0.54 GWh.Footnote 4

Innovation is needed to respond to market drivers

To achieve net-zero by 2050, the pace of battery adoption needs to accelerate.Footnote 5 The rise of battery adoption in the past decade correlated with a 90% total cost reduction. Innovation in technological performance was the biggest driver for battery price reduction observed between the late 1990s and mid-2010s, with the largest share of this originating from public and private research and development, followed by economies of scale of production.Footnote 6 Companies with a competitive edge have relied heavily upon innovation to capture growing market shares, and vertical integration strategies to accelerate development and testing of battery solutions across segments of the value chain.Footnote 7 Therefore, solutions that consider the entire value chain are needed to meet demand and bring manufacturing costs down and this informs the business strategy of most competitors in this space.

Building Canada’s battery innovation ecosystem

Canada has a strong battery innovation pedigree, backed by groundbreaking contributions advancing battery technology. Over the past forty years Canadian universities, industry, and government have made major contributions to battery innovation that today have global impact.Footnote 8

Battery production and innovation is supported across the value chain and along technology readiness levels by many public and private institutions in Canada. This support mainly occurs through programs with broader focuses on clean tech and energy innovation, including technology development, manufacturing scaleup, and recycling. Other programs target the upstream supply chain for these technologies, which include batteries as part of a larger portfolio, by supporting development of critical mineral supply chains in both extraction and refinement. Since 2022, Canada has announced a series of Investment Tax Credits (Clean Technologies Investments, Clean Technologies Manufacturing, and Clean Electricity Investments) to support the domestic commercial deployment and manufacturing of clean technologies, including batteries.

Investments in RD&D across the battery value chain help to advance technology readiness levels and offer a pathway for Canadian battery innovators to establish their place in the ecosystem and secure off-take agreements, ultimately connecting them to the related transportation and electricity value chains.

Strategic Approach to Battery Innovation

OERD's Strategic Approach to Battery Innovation (SABI) supports the vision of a clean, competitive and innovative battery ecosystem in Canada and is organized under three Pillars shown in Figure 2. In addition to an analysis of the context described above, the pillars were informed by industry analysis and consultation, notably the Battery Innovation Roadmap for CanadaFootnote 9 (led by Accelerate Alliance Inc.), and stakeholder engagements on a federal battery initiative that began in 2019. These revealed how Canada has an opportunity to capitalize on its battery innovation assets to produce economic, social, and environmental value for Canadians during the energy transition. The product of the analysis and industry insight is captured in the Battery Sustainability Framework (Figure 5) developed by OERD to organize innovation priorities under four key drivers: energy equity, environmental benefit, economic competitiveness, and energy security.

Value Chain Decarbonization, Security, and Competitiveness

Promote leadership in full value chain decarbonization

Target innovation in critical battery applications that reduce reliance on insecure supply chains

Support innovation-led domestic commercial growth to create long-term economic benefits for Canada

Innovation Infrastructure

Support Canadian innovation infrastructure at each stage of the supply chain

Support the “missing middle” in infrastructure to support expensive, high-risk innovation activities

Support battery workforce growth and transition

Promote local-to-global awareness and collaboration

Firms

Support innovative companies, particularly in areas where Canada has natural advantage or innovation addresses unique Canadian use case

Grow/encourage connections between Canadian companies, academics, industry associations, adopters, federal labs

Support Canadian IP development and retention

Increase the value for companies to stay in Canada

Promote Canadian innovators

SABI Pillars and Associated Objectives

Pillar #1: Supporting innovation that accelerates battery value chain decarbonization, security, and competitiveness.

This Pillar is cross-cutting and depends on innovation infrastructure (Pillar #2) and strong innovators and firms (Pillar #3) growing within Canada to be sustainably realized. In other words, establishing a fully decarbonized value chain for batteries that is secure and competitive requires Canada to have: the innovation infrastructure to develop homegrown solutions and expertise; and domestically located firms to take these innovations to market.

By promoting leadership in full value chain decarbonization, this strategic approach builds on the existing battery innovation ecosystem to optimize batteries for the clean energy transition.

By targeting innovations that reduce reliance on insecure supply chains, this strategic approach ensures that critical infrastructure and essential commodities remain resilient to fluctuating global market dynamics.

By supporting innovation-led domestic commercial growth, this strategic approach creates long-term economic benefits for Canada.

Pillar #2: Supporting the development of world-class battery innovation infrastructure in Canada.

This Pillar establishes innovation infrastructure as a public good to serve a growing and innovative battery industry. This includes the physical and technological infrastructure, skilled and collaborative resources, and facilities that accelerate the development of new ideas by encouraging innovative thinking and risk taking. Activities under this Pillar support the development, attraction, and retention of Highly Qualified Personnel (HQP), investment, and activity from domestic and international companies and investors.

Support to Canadian innovation infrastructure projects along every stage of the supply chain allows low to middle technology readiness level (TRL) innovation to de-risk future investments and enables research, development and demonstration (RD&D) without heavy investment in testing equipment and facilities. This enables innovation in otherwise expensive or high-risk ventures.

The collaborative nature of innovation infrastructure supports the development of the Canadian battery workforce, by establishing the need for and opportunity to train HQPs and skilled trades. This is an enabling factor for the clean energy transition.

Integrated within innovation hubs, innovation infrastructure can promote and connect Canadian innovators with international partners, and foster collaboration amongst the local and global innovation community.

Pillar #3: Strengthening the network of Canadian battery innovators and help grow world-class Canadian firms in the battery value chain.

This Pillar targets the development and growth of innovative Canadian firms throughout the battery value chain. Activities under this Pillar foster connections between domestic firms to share knowledge, needs, and ideas. A healthy network that connects Canadian companies, academia, industry associations, adopters and federal labs can help identify Canada’s natural strengths, opportunities, and threats while promoting Canadian innovation and knowledge development. This network can also leverage Canada’s natural advantages to address unique Canadian use cases. These include solutions tailored to the various communities and climates within Canada to ensure an equitable clean energy transition for all Canadians.

By fostering connections, OERD anticipates that: development of Canadian IP will be informed and guided through strategic considerations among stakeholders from an early stage; collaboration among Canadian battery innovators from industry, academia, federal labs, and adopters will be enhanced; and that favourable conditions will be created for Canadian companies to remain in the Canadian battery ecosystem.

Battery Innovation Priorities

OERD has identified nine near-term Battery Innovation Priorities which it can champion to deliver on the SABI Pillars and their Objectives. These leverage near-term opportunities for investments and supports that will have the greatest impact on long term success under each of the three Pillars. In other words, this strategic approach guides OERD work planning, where the Pillars and Objectives are supported by near-term priorities, which are used to select the most effective OERD tool or activity to achieve the objectives.

- New and improved battery materials, components, cells, and packs that increase performance while reducing cost and environmental footprint.

- New and improved methods for materials production, cell manufacturing, vertical integration, and high production quality of batteries.

- Identification and analysis of promising new battery types, use cases, business models, and markets.

- New knowledge and identification of opportunities for circularity and waste minimization in the battery value chain.

- Improved and useable analysis tools to assess national and regional battery demand and to delineate performance requirements for battery applications in the Canadian environment (including MHDVs, short and long duration energy storage, low-temperature operation).

- Improved and useable battery modelling, lifecycle, and techno-economic analysis tools to evaluate battery concepts across technology readiness levels and for economic, environmental, and security impacts.

- Analysis and assessment of capacity building, skills, and human resources needs to accelerate battery innovation in Canada.

- New and improved networking, information sharing, coordinating, consensus-building, and intellectual property supports for Canadian firms innovating in batteries.

- Enhancing Canada's battery innovation infrastructure to accelerate the development and scaleup of new and improved battery concepts.

Importantly, these near-term priorities respond to multiple innovation needs or opportunities on the outer ring of the Battery Sustainability Framework (Figure 5) and are targeted more specifically through application of the four other frameworks. This demonstrates how OERD is working within the frameworks included below, and how stakeholders in the battery innovation ecosystem can similarly use these frameworks to help identify priorities for investment.

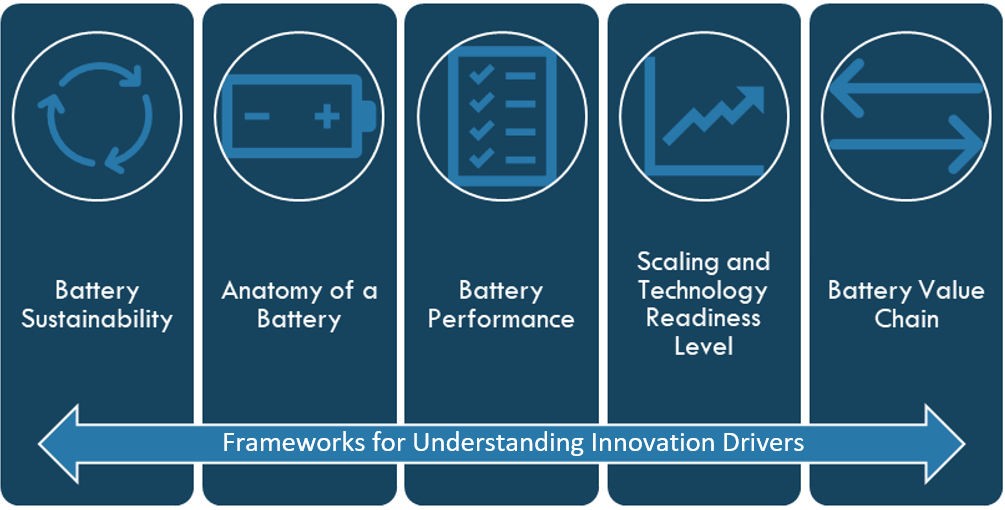

Frameworks for Understanding Innovation Drivers

The SABI Pillars articulate how OERD will influence the pace and direction of battery innovation. As described above, the Pillars were derived through an analysis of the Canadian and global context and industry insights, and further analysis identified the primary battery innovation opportunities and drivers for battery innovation in Canada. This iterative analysis leveraged five conceptual and technical frameworks that characterize the progression of innovation and problems faced by the Canadian battery sector. These frameworks are shared to promote a common understanding of the complex and multi-faced considerations when making strategic decisions within the battery innovation ecosystem, whether they come from a scientific, engineering, economic, or a public policy discipline.

Figure 4 Frameworks for Understanding Innovation Drivers

Text version

A visual representation of Frameworks for Understanding Innovation Drivers. It consists of 5 sections:

- Battery Sustainability - represented by a circular recycling symbol.

- Anatomy of a Battery - symbolized by a battery icon with a '+' and '-' sign.

- Battery Performance - displayed as a checklist.

- Scaling and Technology Readiness Level - shown with a graph of increasing performance.

- Battery Value Chain - indicated by horizontal arrows pointing in opposite directions.

The sections are unified by an arrow running horizontally beneath them, labeled "Frameworks for Understanding Innovation Drivers.

Battery Sustainability Framework

This framework is derived from the World Energy Trilemma and Sustainability frameworks, with additional connections made to the battery value chain. It recognizes that the energy sector transition is supported by, and reciprocally supports, battery innovation along multiple axes. Therefore, strategic thinking incorporating Equity, Environmental, Economic, and Security drivers must factor prominently into battery innovation programming decision-making.

Environmental: the drive to decarbonize Canadian transportation

and power.

Energy Security: the drive to secure resilient supply chains for

Canadian batteries.

These central drivers promote pathways that over the next decade can lead to a battery innovation ecosystem capable of serving and thriving within a net zero emissions economy in 2050. These pathways are shown in the middle ring of the framework. The outer ring identifies innovation needs and opportunities Footnote 10 along the value chain responding to the central drivers. This conceptual framework is depicted in Figure 5.

This framework is fundamental to the SABI because the drivers define what needs to be achieved, and from there OERD identifies the Pillars for its Strategic Approach by selecting the pathways from the middle ring that it can directly support through battery innovation measures. These inform programming and help to select impactful investments and inform other non-funding initiatives OERD can support which respond to multiple needs or opportunities shown in the outer ring.

Figure 5: Battery Sustainability Framework

Text version

- Innovation Driver 1 – Supply Chain Resiliency

- Pathway (security) – Manage Global Battery Supply Chain Risk

- Need – Critical Battery Materials & Chemistries

- Need – Abundant Battery Materials & Chemistries

- Pathway (security) – Manage Battery Resource Dependency Risk

- Opportunity – Trade Partnerships & International Initiatives

- Need – Decoupling from Unreliable Supply Chains

- Pathway (security) – Manage Global Battery Supply Chain Risk

- Innovation Driver 2 – Industrial Transformation & Competitiveness

- Pathway (economic) – Support Innovation Infrastructure

- Opportunity – Design & Chemistry

- Need – Prototype Development & Scale-up

- Pathway (economic) – Grow Innovative Firms

- Opportunity – Markets & Value Chains

- Opportunity – Globally Competitive & Collaborative

- Pathway (equity) – Support Equitable Transition

- Need – Skilled Workforce

- Need – Affordable Batteries

- Need – Underserved Canadian Use Cases

- Pathway (economic) – Support Innovation Infrastructure

- Innovation Driver 3 – Decarbonized Transport & Power

- Pathway (environmental) – Decarbonize Battery Supply Chains

- Need – Industrial Decarbonization

- Need – Battery Circularity

- Need – Clean Electricity Input

- Pathway (environmental) – Support Net Zero Applications

- Need – Stationary Storage

- Need – Off-road Mobility Applications

- Need – On-road Mobility Applications

- Pathway (environmental) – Decarbonize Battery Supply Chains

Energy Equity

This Battery Sustainability Framework considers equity central to the economic transition. While nested within an economic driver, its applicability extends across all drivers for clean energy transition. To support accessibility and affordability of battery enabled technologies and opportunities within the battery industry, each segment along the sustainability framework must apply an energy equity lens to seek opportunities beneficial to all Canadians. For instance, applying this lens to growing innovative firms, can ensure equitable opportunities for investments and promote companies owned by Indigenous and underrepresented groups, or supporting skills transfer to diverse Canadians. In another example, applying this lens to supporting net zero applications can ensure regional access to affordable solutions that meet the needs of that community (e.g. Indigenous, remote, underserved or experiencing energy poverty). This lens even applies to supply chain resiliency to ensure material is sourced from communities that ensure human rights are at the forefront of their industries for both its employees and surrounding communities.

This driver supports: the Government of Canada’s commitments to reconciliation, gender equity and the reduction of racism and discrimination; and NRCan’s Departmental Sustainable Development Strategy (DSDS)Footnote 11 which is leading the Federal Sustainable Development Strategy (FSDS)Footnote 12 for Goal 7 “Increase Canadians’ access to clean energy” while also contributing to Goal 5 “Champion Gender Equality”, and Goal 8 “Encourage inclusive and sustainable economic growth in Canada”. The SABI supports the commitment to Goal 7 and 8 by accelerating the development of clean energy technologies for Canada’s diverse needs.

Decarbonizing Transport & Power

Batteries play a key role in decarbonizing transport because they provide an alternative to fossil fuels by extending the reach of electrification and its impact, especially when powered by non-emitting energy sources. They support net zero emissions power as a flexible resource to balance increased renewable energy supply and increasing peak demand caused by increasing electrification of energy end use. To be impactful along this driver, batteries selected for net zero applications should be sourced from decarbonized supply chains that reduce waste and emissions from material and component processing. This will require tools to benchmark and quantify decarbonization efforts and help mitigate the environmental risk exposure of Canada’s battery value chains.

Industrial Transformation & Competitiveness

The global battery ecosystem is emerging as a major economic driver, underpinning not only the establishment and growth of battery material, component, and cell production industries, but also the future of the automotive and extractive industries. The maturity of battery technologies coupled with a large projected growth makes batteries a relatively low risk investment. With the fundamentals established, battery innovation offers Canada a competitive industry advantage, particularly in the fields of material science and manufacturing innovation.

An ambitious vision for Canada's battery ecosystem could capitalize on the innovation imperative defining the global industry and contribute to generating high-quality and fairly compensated jobs less sensitive to material flows and commodity pricing. Measures which support connections between Canada’s academic and industry strengths to grow innovative firms domestically could capitalize on Canadian assets, countering the risks from competing markets. Additional domestic assets could be developed in public infrastructure and industry capacity required to transform existing manufacturing strengths to be oriented toward this global growth market.

Resilience & Security

Several jurisdictions have shifted towards developing domestic supply and value chains for battery innovation and manufacturing, starting with China’s National Battery Strategy published in 2013. In response, states with the resources and technologies to compete on a global scale have brought forward their own public policies to support enhanced production of battery technologies. Today, China leads the world in battery production, while the US, European Union, South Korea, and Japan follow.

The outsized global economic and environmental implications outlined above elevate batteries and battery innovation to issues of national security. Battery demand is large, growing, and global, while the battery value chain is currently dominated by a few companies and state actors. Today’s battery input materials are also concentrated in few geographies (including Canada), and multiple countries have developed and executed battery-specific industrial strategies to reap the benefits from control of the battery supply chain.

A nation’s ability to provision itself and maintain its autonomy depends on its ability to serve domestic battery needs, especially for critical infrastructure such as grid and defense applications. In this backdrop, homegrown innovation in batteries, including strategies for bringing to market, protecting intellectual property, and collaborating internationally, becomes a critical lever for supply chain resiliency and economic competitiveness.

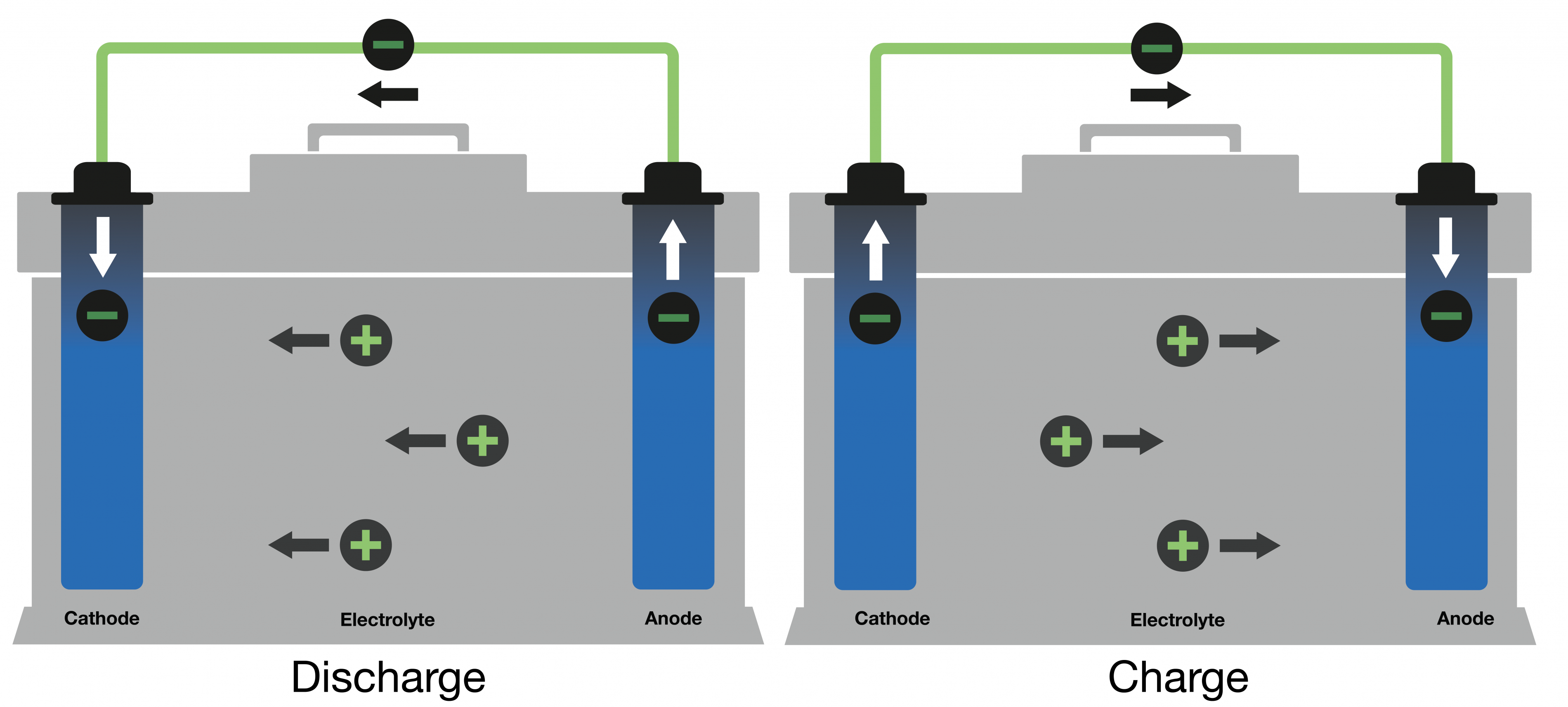

Anatomy of a Battery Framework

This framework outlines the components of a battery to understand the various opportunities for innovation along multiple design features. Fundamentally, a battery is capable of accepting, storing, and releasing electricity through the selection, arrangement, and interaction of three cell components—the anode, cathode, and electrolyte, shown schematically in Figure 6 for a typical lithium-ion battery.

The illustration in Figure 6 not only shows the simple operating principle of a battery, but it also captures the strict relationship between the quantity of electrical energy that can be stored and the amount of active electrode material needed, demonstrating how battery technology is intrinsically tied to material intensity. Therefore, innovation that promotes materials substitution of supply-constrained material inputs and scales up alternative chemistries from earth-abundant minerals can further reduce battery production costs and alleviate supply chain bottlenecks.

The general operating principle of a battery from Figure 6 applies to several other battery designs including metal air batteries, solid state batteries, sodium-ion batteries, and flow batteries, which underscores the importance of evaluating battery innovations at the cell level in addition to the end-use application level.

Figure 6: Illustrative example of a Li-ion battery

Text version

In this battery design, the energy is stored in solid electrode materials (in the anode and cathode active materials). Lithium ions are shuttled back and forth through the liquid electrolyte, which conducts the ions (shown as positive charges) but not electrons (shown as negative charges) which are shuttled back and forth between anode and cathode through the external circuit, providing electricity on demand.

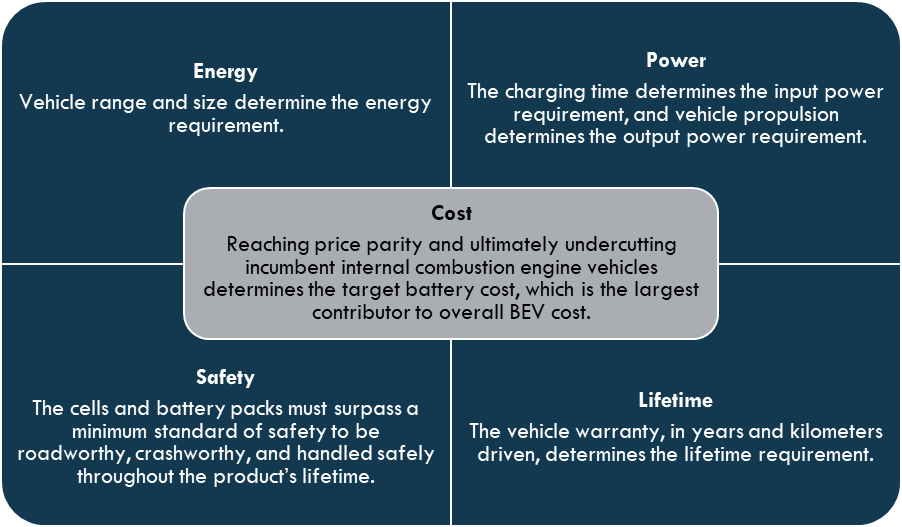

Battery Performance Framework

The requirements of a battery’s end-use application can be mapped onto five key battery performance metrics: energy, power, safety, lifetime and cost. Battery materials, cells, and packs ultimately determine the end-use application’s performance envelope, which must meet or exceed the targets defined by the application requirements. Therefore, the innovation challenge is to balance the performance metrics trade-offs across materials, cells, and packs in consideration of their end use. For example, Figure 7 connects battery performance to the requirements of an electric passenger vehicle.

By framing battery innovation in terms of closing gaps between battery performance and application requirements, researchers and decision makers can more objectively assess projects and chart pathways to commercialization. This drives the performance of the end product, and ultimately, its marketability.

Figure 7: Key requirements for a passenger battery EV

Text version

- Cost: Reaching price parity and ultimately undercutting incumbent internal combustion engine vehicles determines the target battery cost, which is the largest contributor to overall BEV cost.

- Energy: Energy Vehicle range and size determine the energy requirement.

- Power: The charging time determines the input power requirement, and vehicle propulsion determines the output power requirement.

- Safety: The cells and battery packs must surpass a minimum standard of safety to be roadworthy, crashworthy, and handled safely throughout the product’s lifetime.

- Lifetime: The vehicle warranty, in years and kilometers driven, determines the lifetime requirement.

Scaling and Technology Readiness Level Framework

Mapping the development of key battery components as they are scaled into the intended battery application along the technology readiness level (TRL) can help to frame the market drivers and level of financial risk for investments in innovation projects. This is due to battery modular design and mass producibility which has shown rapid advancement and commercialization of battery technologies. Investment in battery innovation for a given application is informed by this scalability and the level of risk associated at each scale. This hybrid framework is derived from two models: the first is a general sizing of different battery applications and projected demand for those applications; the second, important to any innovation programming, is the Technology Readiness Levels (TRL).

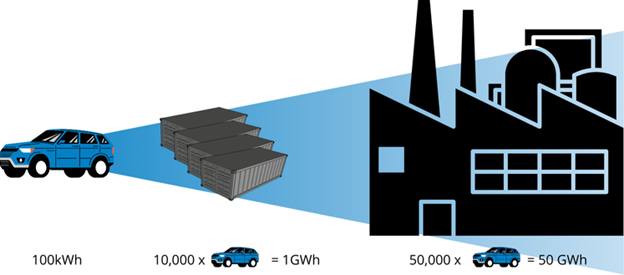

The first model leverages the fact that batteries have implications across a range of scales spanning over 8 orders of magnitude. For instance, Figure 8 depicts how, at the application level, a large BEV battery pack can contain 100 kWh of energy capacity, a large stationary storage installation can be 1 GWh (equivalent to 10,000 large BEV battery packs), and a modern battery gigafactory can produce around 50 GWh a year (enough for 500,000 large BEV battery packs per year). This helps to understand the global demand for batteries which, in 2023, was just over 1 TWh across all sectors, though primarily from passenger BEVs. This is approximately the annual output of 20 modern battery gigafactories. In the net zero scenario, annual global lithium-ion battery demand will grow to almost 10 TWh in 2035, representing a 10-fold increase in 12 years.Footnote 2

Figure 8: Example of battery scalability

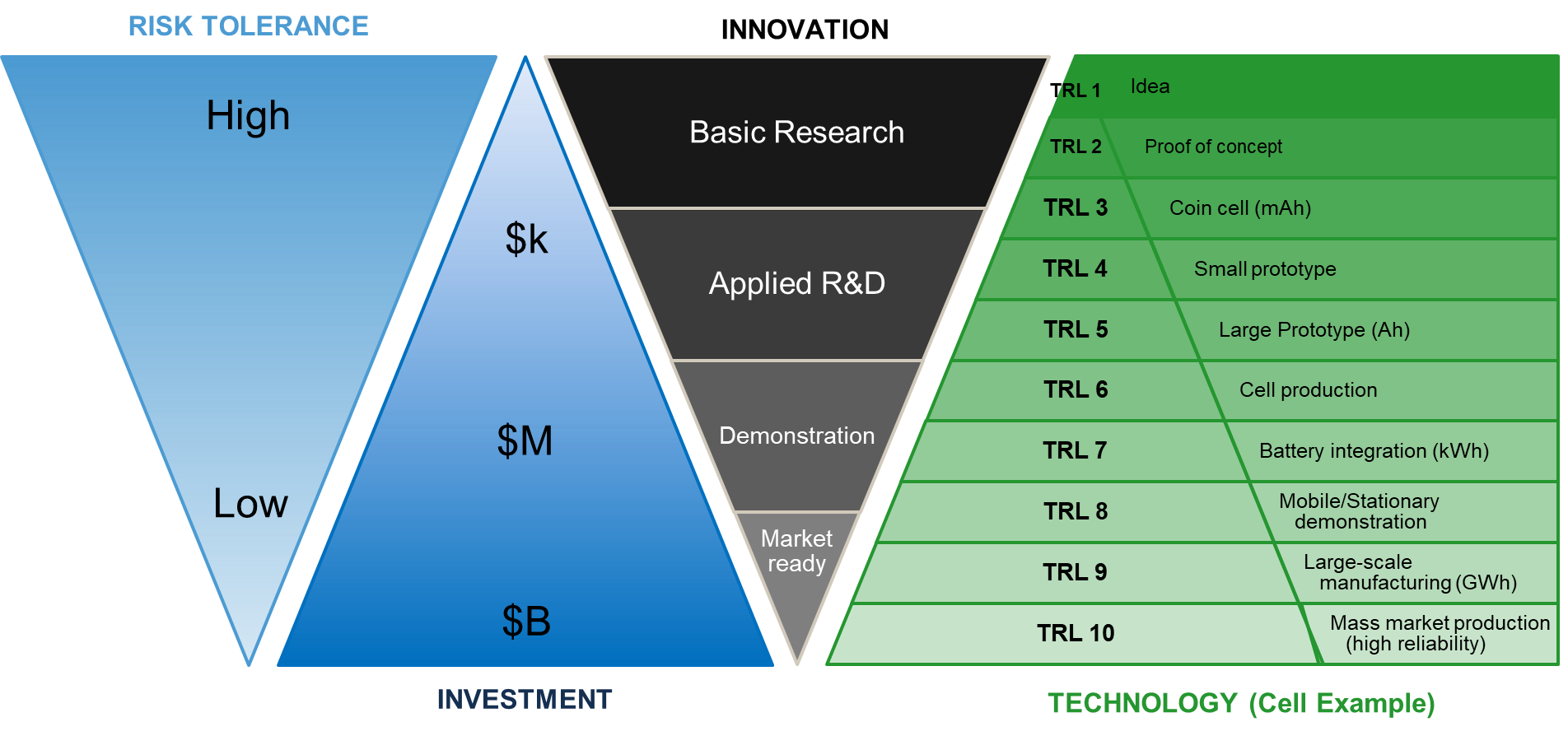

The second model used in the framework is the TRL scale which has been widely adopted by innovation programs across the Canadian government. The TRL scale is a semi-quantitative and generic measure to evaluate a technology’s maturity level progression from basic research (TRL 1-2), applied research and development (TRL 3-5), pilot and demonstration (TRL 6-8), and finally adoption and product maturity (TRL 9+). Each level carries a certain amount of technical and financial risk, where innovation at lower TRL has a higher tolerance to risk of failure, while innovation at high TRL is more sensitive due to the high level of investment needed for a large-scale experiment.

The basis for this framework lies in the scalability of both models, which invites alignment of scales between investment, TRL, and the value chain to balance risks and investment in the innovation space. Figure 9 offers an example for new innovations in cell development and manufacturing, with estimated level of investment. Adapted from Frith et alFootnote 13, TRL scales for innovations along a specific battery value chain segment can correlate with increasing scale of deployment, battery size, and level of investment required. This means that battery innovation will have the greatest impact if it can be scaled, but also if that scaling can be a consideration across all TRLs regardless of the end use.

Figure 9: Technology Readiness Level Scale for BEV Battery Applications, adapted from Frith et al.

Text version

- Risk Tolerance

- High

- Low

- Investment

- $k

- $M

- $B

- Innovation

- Basic Research

- Applied R&D

- Demonstration

- Market ready

- Technology (Cell Example)

- TRL 1: Idea

- TRL 2: Proof of concept

- TRL 3: Coin cell (mAh)

- TRL 4: Small prototype

- TRL 5: Large prototype (Ah)

- TRL 6: Cell production

- TRL 7: Battery integration (kWh)

- TRL 8: Mobile/Stationary demonstration

- TRL 9: Large-scale manufacturing (GWh)

- TRL 10: Mass market production (high reliability)

Battery Value Chain Framework

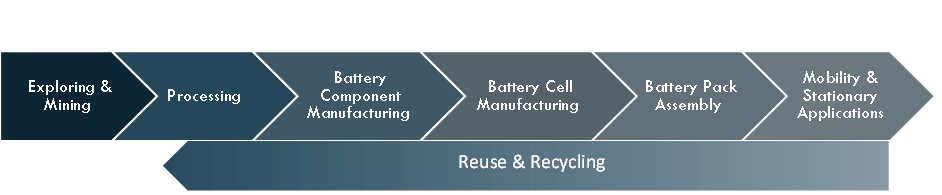

In parallel to the rise of Li-ion batteries this decade in mobility and stationary applications, a global battery supply chain has developed according to stages of production. Various depictions of the battery supply or value chains exist to different degrees of granularity. OERD’s depiction in Figure 10, is based on the highest levels representing the seven major industrial segments of the battery value chain that follow the entire product life cycle through time. It captures the direction of materials and energy flows toward the production and operation of batteries, and these correlate with economic value creation and environmental footprint. Also, key stakeholders and their relationships in the domestic and global battery ecosystem can be categorized by value chain segment with relative ease, but this will become more challenging with the growing trend toward vertical integration spanning multiple segments.

Figure 10: Framework of Battery Value Chain segmenting into areas for investment

Text version

The supply chain spans battery minerals extraction and refining, battery materials and component production, and cell and pack manufacturing. As the supply of battery inputs strains to keep up with growing demand, battery recycling and broader circularity efforts are necessary to extract maximum value and minimize waste, which completes the value chain.

Annex A: Stakeholder Innovation Opportunities

There are a number innovation opportunities that industry stakeholders could consider which respond to the drivers outlined in the Battery Sustainability Framework. To facilitate collaborative conversation with industry stakeholders these opportunities are outlined below:

- Materials Substitution, Abundant Battery Chemistries, and Affordable Batteries. Battery innovation via substitution of costly materials and components with cheaper, more abundant, and geographically diverse alternatives while maintaining or improving performance.

- Application-guided Battery Innovation. Consideration of specific end-use application requirements and operating conditions at all stages of the battery innovation process to accelerate path to market.

- Vertical Integration, Processing, and Advanced Manufacturing of Batteries. Battery innovation that considers upstream and downstream linkages to yield efficiencies spanning segments of the value chain, both in terms of reductions in the materials and energy intensity of production and increases in production throughput and quality.

- Battery Data and Modeling Approaches. Computation and data approaches to battery innovation to accelerate the pace of insight generation and translation from concept to market implementation.

- Battery Circularity. Innovation to minimize the generation of waste across the battery value chain including the generation of emissions in the manufacturing and upstream processes of battery production.

- Battery Standards & Regulations. Innovation to accelerate the generation, development, and adoption of standards & regulations of batteries to advance interoperability, safety, traceability, and environmental practices.

- Battery Services & Business Models. Innovation in support of new market development and new use cases of batteries including for climate adaptation, long duration energy storage, batteries as a service, battery swapping, and vehicle-to-grid (V2G).