Details

- Publication date

- Author(s)

- ISBN

978-0-660-78867-8

Executive Summary

Publicly available assessments and forecasts of Canada’s battery ecosystem and its potential competitiveness often rely upon estimations based on global forecasts and corporate announcements, lacking precision on specific metrics. The benchmarks in this report support a common understanding of battery technology fundamentals, and a holistic stock taking of the strengths and capabilities, which should be referenced when assessing the potential of Canada’s battery ecosystem. The Office of Energy Research and Development (OERD) at Natural Resources Canada (NRCan) performed this benchmarking study, including a review of the Canadian battery ecosystem to help inform its funding and non-funding supports for battery innovation. This report also offers common battery definitions and targets for Canadian battery industry stakeholders, particularly decision-makers and investors.

Using the five battery frameworks introduced in the OERD’s Strategic Approach to Battery Innovation released in March 2024 as the lens for analysis, this report benchmarks the Canadian battery ecosystem along the following axes:

- battery stakeholders including firms and innovation infrastructure;

- battery demand and deployment; and

- application-defined technical battery performance indicators and targets.

Benchmarking data was extensively collected and referenced from consultancy reports, stakeholder engagements, and multiple publicly available sources including firm and institution websites, peer-reviewed literature, commercial battery specifications, and industry reports.

There are about 250 firms downstream of mining and exploration situated along the Canadian battery value chain and distributed across most of Canada. More than a quarter of these firms’ areas of focus span more than one value chain segment. Firms are concentrated in upstream and downstream segments, leaving the midstream punctuated by limited processing capability of raw material inputs into battery grade reagents and limited manufacturing of large-format battery cells. While there are battery firms of all sizes and at all stages of development in Canada, more than 60% are small, and more than half have operations in the R&D, pilot, pre-commercial, or planned stages.

Canada’s battery innovation infrastructure includes universities, research laboratories, pilot and testing facilities which cluster in four geographies—in Western Canada, Southern Ontario, Québec, and Nova Scotia. These innovation clusters provide physical technological infrastructure, skilled and collaborative resources, and facilities that accelerate the development of new ideas by encouraging innovative thinking and risk taking. However, infrastructure capable of producing battery cells in a final product-ready state is currently limited in Canada.

Demand for batteries in Canada is driven largely by the transportation sector, namely on-road light-duty battery electric vehicles, which reached about 18 GWh annual demand in 2024. Battery capacity additions in the electricity sector, while smaller, are expected to reach 4 GWh in 2025 to mostly address the energy shifting services and arbitrage markets. Total demand for batteries is expected to grow significantly in the next decade, and Canada could require 200 GWh of annual battery production in 2035 to meet its domestic needs across both segments. To put in perspective, global demand for batteries is forecast to reach more than 10,000 GWh in 2035 in the net-zero scenario.

Today and in the future, the competitiveness of Canada’s battery ecosystem critically depends on meeting key battery technical performance metrics, which include energy density, power density, cost, safety, lifetime, and sustainability.

Today’s high-performance lithium-ion cells with nickel chemistry (NMC) can cost about $160/kWh, provide energy densities exceeding 300 Wh/kg and 800 Wh/L, reach 500-1000 cycles before end of life, and emit 50-80 kgCO2eq/kWh in their production. Future targets of $95/kWh, 500 Wh/kg and 1150 Wh/L, 2000 cycles, and 20-30 kgCO2eq/kWh are set for 2035 (2040 for cost) for high-performance cells.

Today’s more affordable lithium-ion cells are based on iron chemistry (LFP) and can cost about $110/kWh, provide energy densities around 180 Wh/kg and 380 Wh/L, reach 6000 to 8000 cycles before end of life, and emit 40-70 kgCO2eq/kWh in their production. Future targets of $67/kWh, 270 Wh/kg and 550 Wh/L, 10,000 cycles, and 15-20 kgCO2eq/kWh are set for 2035 (and 2040 for cost) for affordable cells.

Multiple Canadian battery firms and researchers are innovating using a variety of approaches to be competitive today and to ensure their future competitiveness. These include incremental advances across the lithium-ion battery value chain in materials design and synthesis, as well as downstream innovation in the design and production of cells and packs. In addition, Canadian innovators are developing solid-state batteries, batteries with open architectures like flow batteries and metal-air batteries, and batteries with chemistries like sodium and other metal alternatives to lithium.

The Canadian battery ecosystem is still nascent, and in order to meet the objectives of decarbonization, security, and competitiveness, it must address the vulnerability along the middle segments of the battery value chain. Canada can develop a competitive advantage through the following innovations: manufacturing techniques, which can reduce costs and become less environmentally impactful; cell design, which can boost energy density or power density metrics; and battery chemistry innovations, which can tap into properties of alternative battery materials and components to achieve performances which are harder to reach for standard lithium-ion battery cells.

Table of Content

- Executive Summary

- List of Figures

- List of Tables

- 1. Introduction

- 2. Ecosystem

- 3. Battery Deployment

- 4. Battery Technology Benchmarking and Targets

- 5. Conclusion

- Appendix A - Explanation of Key Terms

- Appendix B - Battery Performance Metrics Descriptions

- Appendix C - Cell Energy Density Sample Calculation

- Appendix D - Reference Data

- Annex 1 – Firms in the Canadian Battery Ecosystem

- References

List of figures

- Figure 1: Visualization of the battery value chain

- Figure 2 Distribution of firm count by primary value chain segment along the middle segments of the battery value chain

- Figure 3: Relative size of companies across the middle segments of the battery value chain (Micro: 1-4 employees, Small: 5-99 employees, Medium: 100-499 employees, Large: 500 or more employees)

- Figure 4: Distribution of large companies (500 employees or more) across the middle segments of the battery value chain

- Figure 5: Distribution of companies along the middle of the battery value chain possessing a primary, secondary, and tertiary value chain segment

- Figure 6: Company distribution across battery component manufacturing

- Figure 7: Distribution of companies producing cells by chemistry, format, and commercial status. Large format cells are designated as (>20 Ah), with small format cells being below that threshold

- Figure 8: Distribution of companies operating at a pilot scale, of pre-commercial status, and operating commercially in the Battery Pack Assembly value chain segment

- Figure 9: Count of companies operating in stationery and mobility applications

- Figure 10: Emerging Canadian Battery Innovation Clusters

- Figure 11: National and provincial passenger EV registration statistics in Canada from 2020 to 2024. (Source: Statistics Canada)

- Figure 12: Annual Canadian battery demand for passenger battery electric and plug-in hybrid electric vehicles

- Figure 13: Annual Canadian battery demand in GWh for all vehicle types, assuming net-zero scenario by 2050. (Source: BloombergNEF)

- Figure 14: Projected cumulative stationary storage capacity in Canada assuming no major policy changes. (Source: BloombergNEF)

- Figure 15: Volumetric (measured in Wh/L) and gravimetric (measured in Wh/kg) energy densities for selected commercially available cells labeled by cell format (pouch, cylindrical, or prismatic). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).

- Figure 16: Volumetric (measured in Wh/L) and gravimetric (measured in Wh/kg) energy densities for selected commercially available cells labeled by cell chemistry (NMC, LFP, NCA, Na-ion). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).

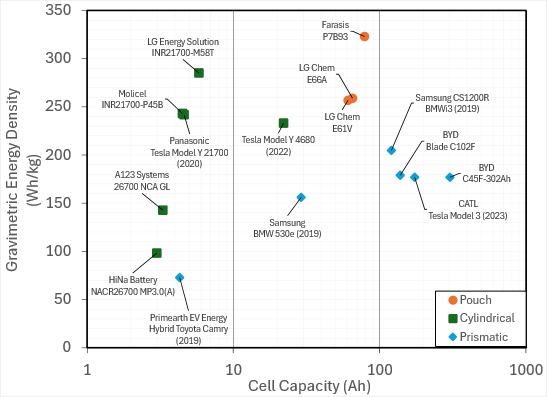

- Figure 17: Gravimetric energy densities (measured in Wh/kg) and nominal cell capacities (measured in Ah) for selected commercially available cells labeled by cell format (pouch, cylindrical, or prismatic). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).

- Figure 18: Continuous discharge power densities (measured in W/kg) and nominal cell capacities (measured in Ah) for selected commercially available cells labelled by cell format (pouch, cylindrical, or prismatic). Continuous discharge power densities are determined from discharging the cell from 100% SOC at 25°C until reaching 10% SOC and either reaching the lower voltage limit (either 2 or 2.5V) or reaching a maximum surface temperature of 68°C.

- Figure 19: Peak discharge power densities (measured in W/kg) and nominal cell capacities (measured in Ah) for selected commercially available cells labelled by cell format (pouch, cylindrical, or prismatic). Peak discharge power densities are determined by discharging the cell from 100% SOC at 25°C for 5 minutes

- Figure 20: Calendar aging dataset showing relative capacity decline and resistance growth of 232 commercial lithium-ion cells stored at four temperatures (24°C, 45°C, 60°C, and 85°C) and two SOC values (50% and 100%)

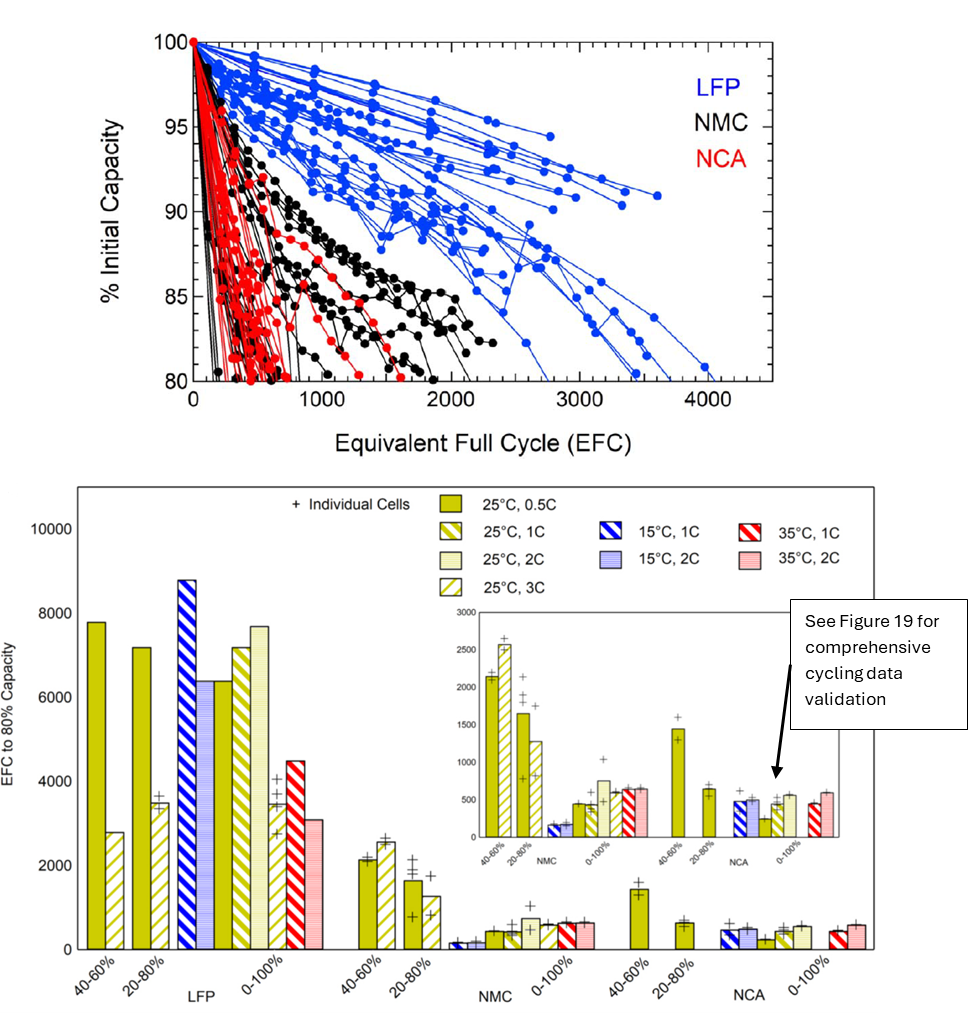

- Figure 21: Discharge capacity retention and equivalent full cycle capacity for commercially available cylindrical cells with 18650 form factor and LFP, NMC, and NCA cathode chemistry, charged at a rate of 0.5C and discharged at variable rates and SOCs. Extrapolated Equivalent Full Cycle (EFC) of LFP, NMC and NCA are show in top graph.

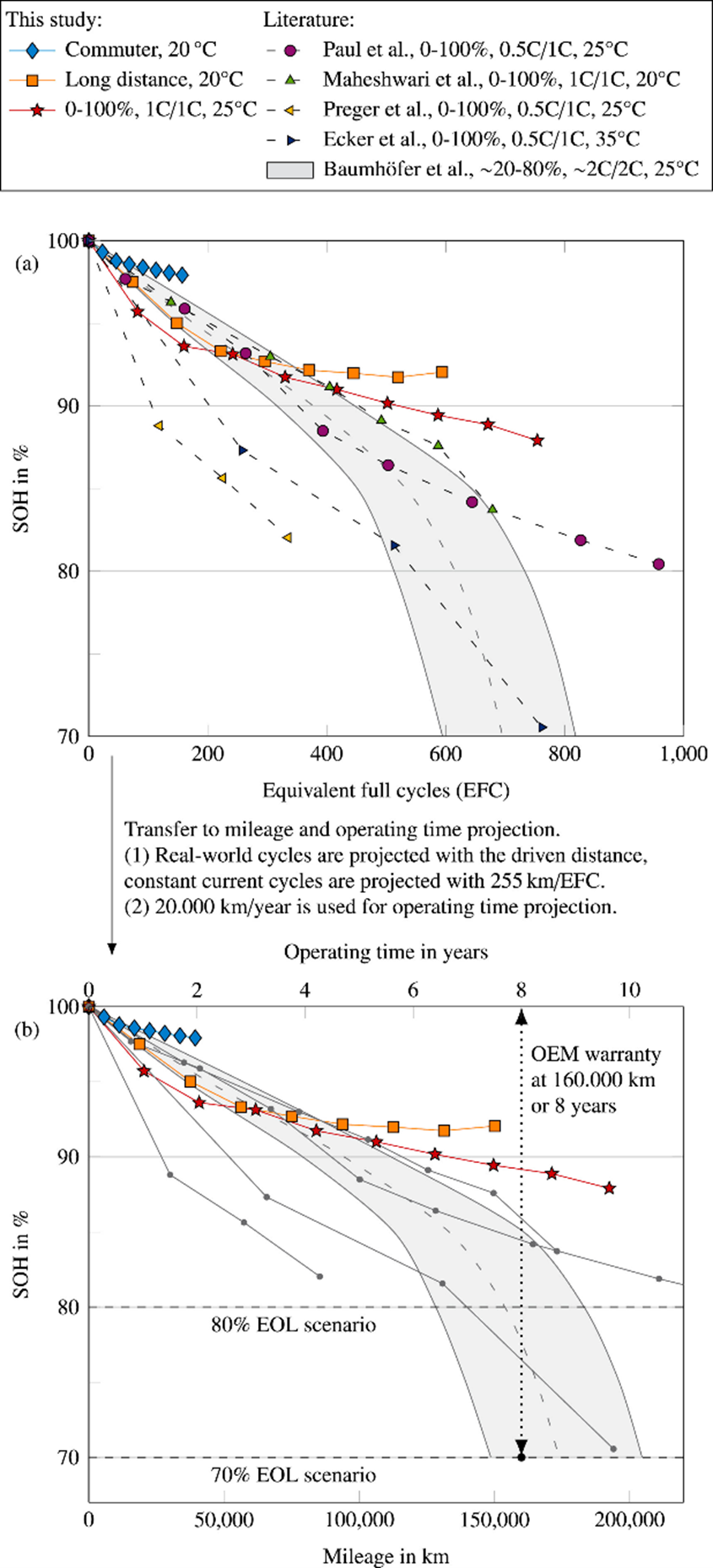

- Figure 22: Capacity retention of a Volkswagen ID.3 battery cell for different duty cycles in terms of (a) equivalent full cycles and (b) conversion to mileage and operating time

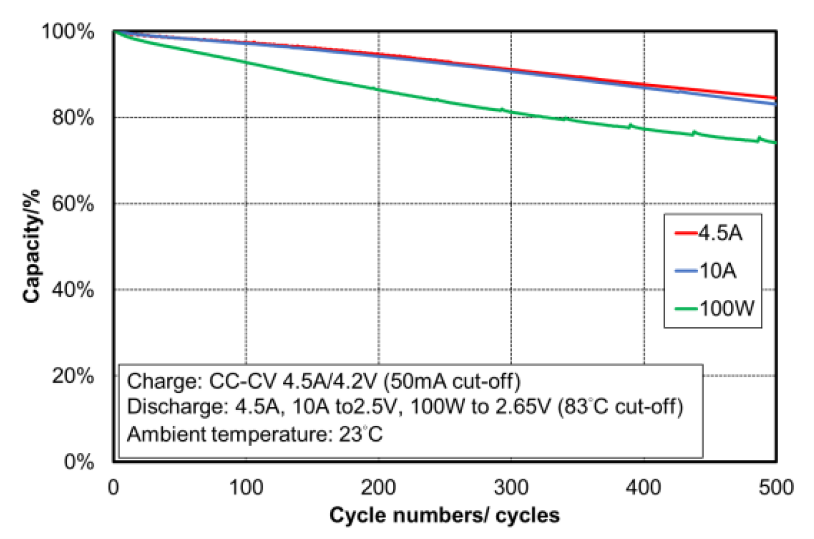

- Figure 23 Capacity retention data for the 4.5 Ah cylindrical INR21700-P45B cell from Molicel

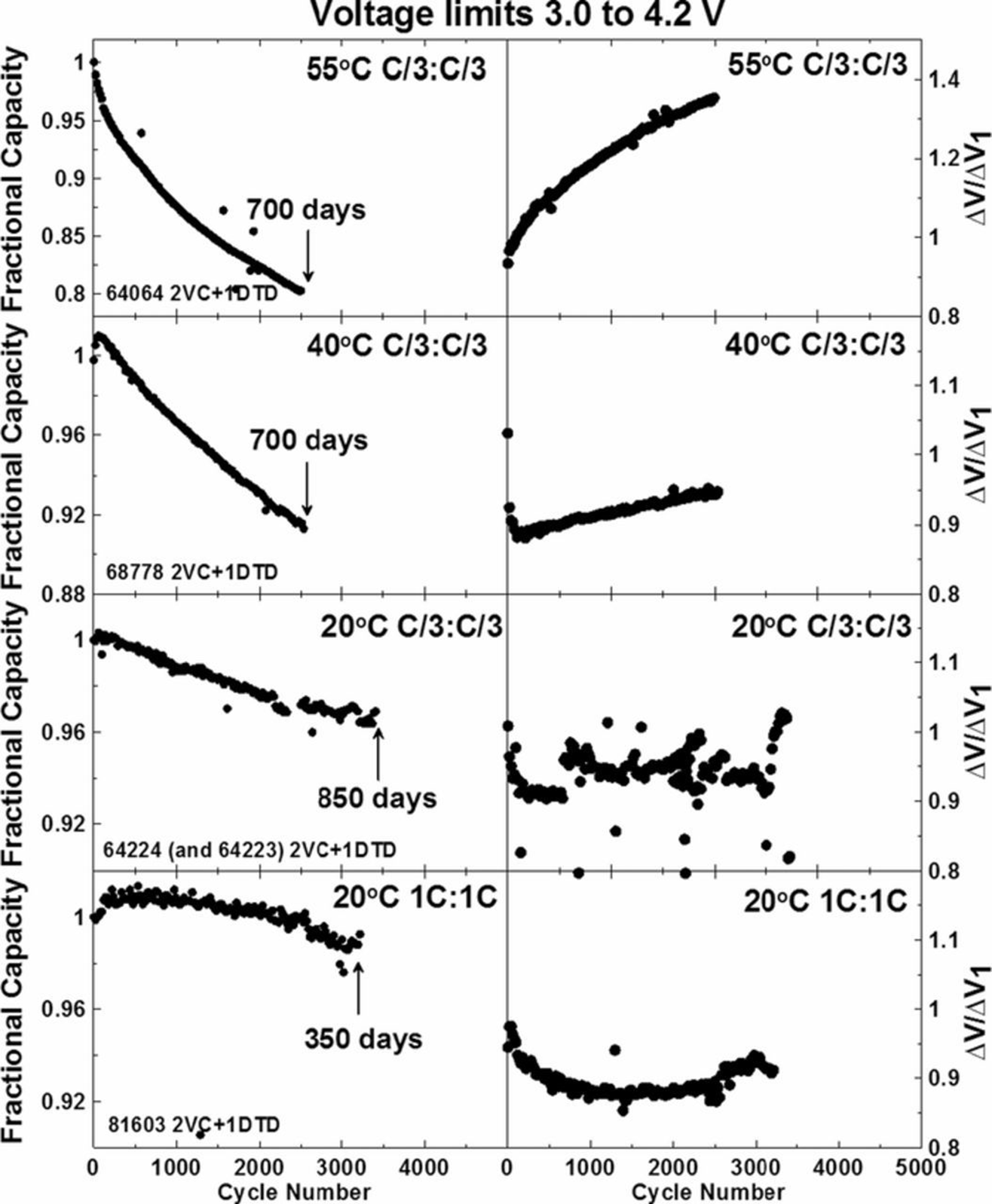

- Figure 24: Fractional capacity and normalized voltage overpotential ∆V (indicative of resistance growth and power fade) of 240 mAh lithium-ion pouch cells constructed with single-crystal nickel manganese cobalt (NMC532) cathode material, artificial graphite, and common electrolytes, cycled from 3.0 to 4.2V at specified C-rates and temperatures

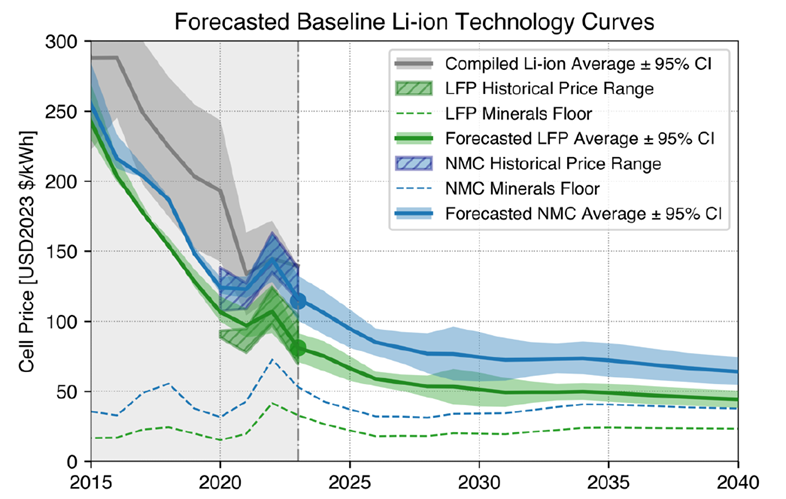

- Figure 25: Historical and future price ranges (USD) of NMC and LFP batteries alongside total cost of input materials

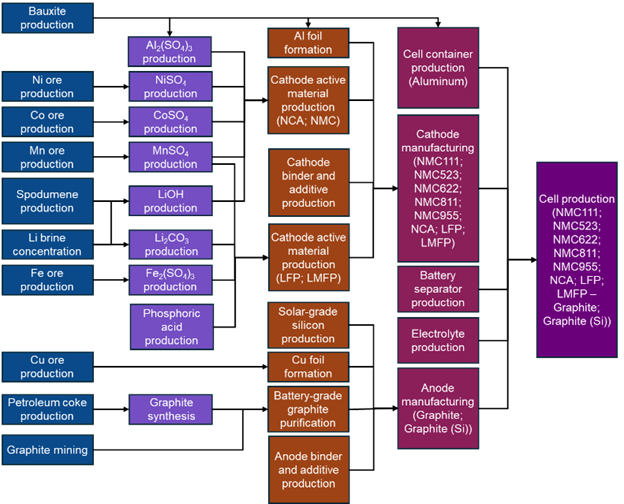

- Figure 26: Flows of all input materials and processing steps from raw materials to cell production of select Li-ion battery chemistries. Adapted from Xu et al

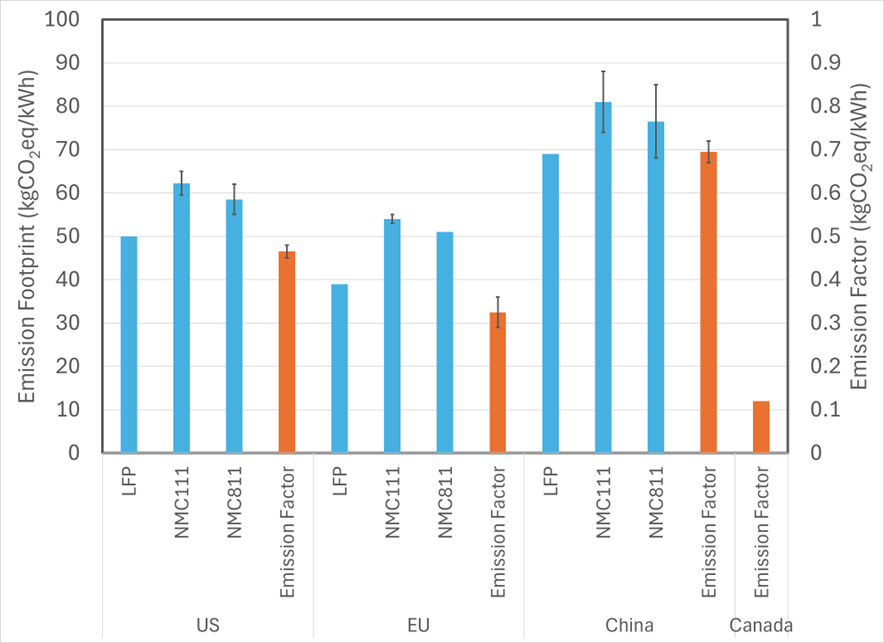

- Figure 27: (left axis, blue bars) LCA-derived GHG emission footprints of LFP and NMC chemistries manufactured in United States, European Union, and China; (right axis, orange bars) Regional electricity production emission factors for United States, European Union, China, and Canada grids. Note: The error bars show the variations in the calculated GHG emission footprint across these sources, and show how assumptions can impact the final accounting, but that nonetheless, there is general convergence between these analyses

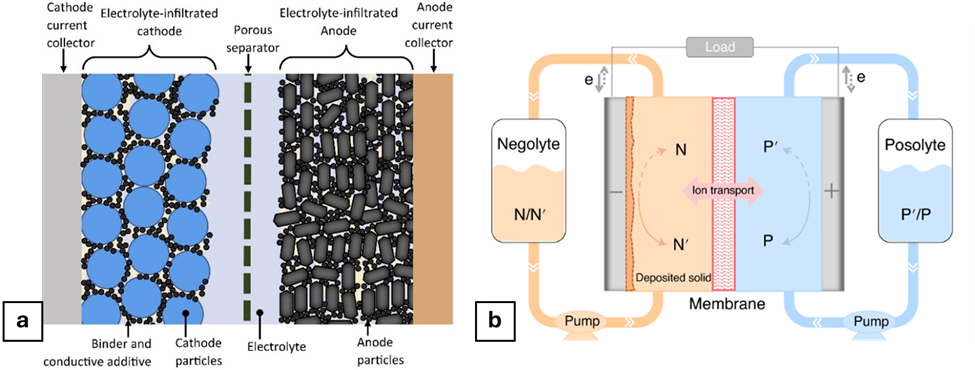

- Figure 28: Schematic depictions of representative closed and open cell architectures, shown for (a) a conventional lithium-ion battery (closed system), and (b) a redox flow battery (open system)

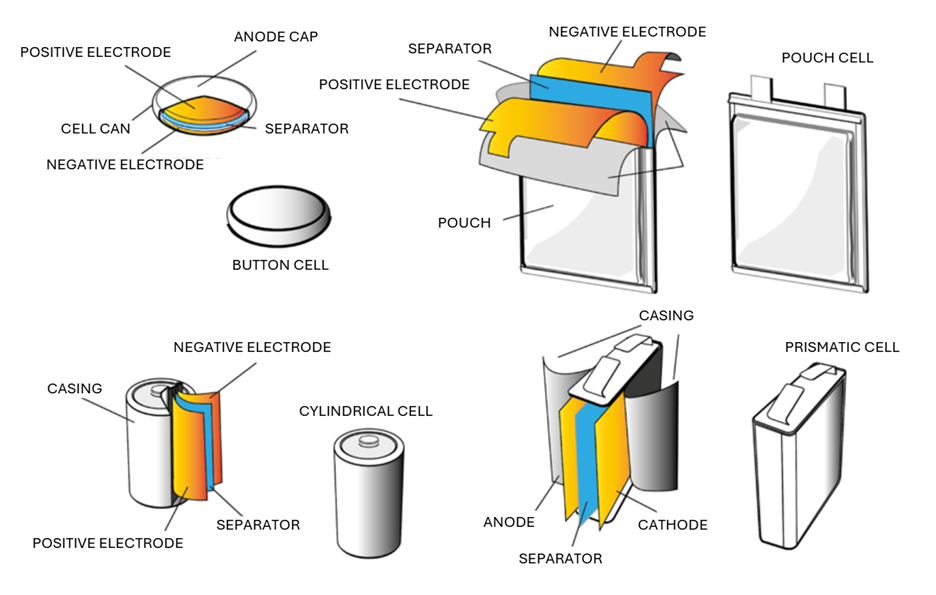

- Figure 29: Typical cell types for commercial lithium-ion batteries

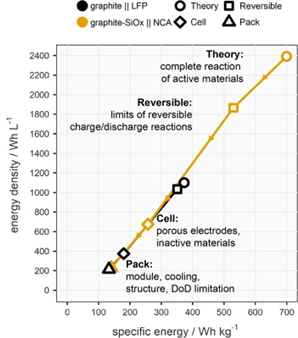

- Figure 30: Gravimetric and volumetric energy densities for LFP/graphite and NCA/graphite-SiOx cathode and anode chemistries at the theoretical and practical materials level, the cell level, and the pack level.

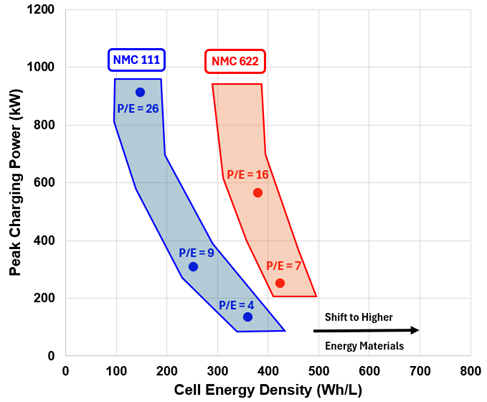

- Figure 31: Estimated battery peak charging power versus cell energy density for groupings of selected cathode active materials paired with graphite anodes for a hypothetical 100 kWh battery pack. Adapted from Masias et al.

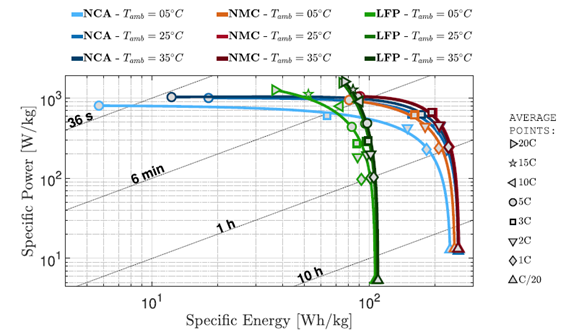

- Figure 32: Energy density and power density trade-off for selected commercial cylindrical lithium-ion cells with NCA, NMC, and LFP cathode chemistry tested at different ambient temperatures.

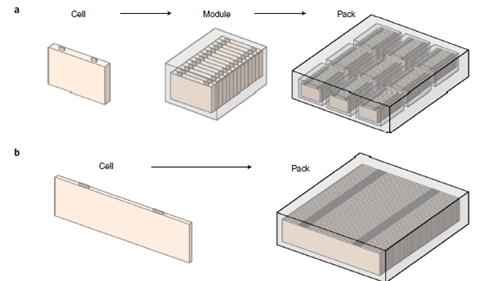

- Figure 33: Image of a BYD Blade C102F prismatic LFP cell.

- Figure 34: A schematic illustration of (a) a conventional battery pack comprised of prismatic cells and (b) a battery pack with cell-to-pack integration.

List of tables

- Table 1: Applications of commercially available cells selected for benchmarking as provided from cell manufacturer websites, cell specifications, and third-party testing

- Table 2: Comparison of selected prismatic lithium-ion cells used in hybrid electric, plug-in hybrid and battery electric vehicles of similar size and their power capabilities

- Table 3: Figure 21 calendar aging results under various storage conditions

- Table 4: EUCAR Classification of battery cell safety hazards

1. Introduction

Batteries are positioned to play an important role in the energy transition, from electrification of transportation, to storing energy generated by renewable energy sources of wind and solar, for example. Leading battery technologies rely on critical minerals to offer high energy density storage solutions balanced against other important performance metrics depending on their end application. Understanding how each of these metrics is achieved as well as their potential, can help decision makers and investors right-fit battery solutions to their needs, as well as understand the relative gains and trade offs of battery innovations. This report supports this understanding by benchmarking the Canadian battery ecosystem of firms and innovation infrastructure, battery demand and deployment, and battery performance and targets.

In 2024, the Office of Energy Research and Development (OERD) at Natural Resources Canada (NRCan) released the Strategic Approach to Battery Innovation (SABI) that outlines three Pillars of a competitive, clean, and innovative battery ecosystem for Canada.Reference [1],Reference [2] The SABI also offers five conceptual and technical frameworks to create a common understanding of the electrochemical battery sector for decision makers, from various backgrounds be it science, policy, economics, or engineering. These five frameworks are: Anatomy of a Battery, the Battery Value Chain, Scales of Battery Technology Readiness Levels, Battery Performance Metrics, and Battery Sustainability.

These frameworks are the basis of this benchmarking report and were used to highlight six main performance metrics for batteries. For each performance metric, current-day benchmark values and targets across leading and emerging technologies are presented for Canadian innovators to compare against and to strive toward in the medium- to long-term. Both the benchmark and target values are derived from commercial specifications, technology roadmaps, literature review, and technology projections, to ensure the continued competitiveness of Canadian innovations. As such, the target values are derived based on multiple considerations and are offered as potential values for each metrics category. Appendix A - Explanation of Key Terms, explains the nuances of each metric.

To fully contextualize the Canadian opportunity, this report first presents the state of the battery ecosystem, including battery firms and innovation infrastructure. The SABI identified these as the two pillars underpinning decarbonization, security, and competitiveness of the Canadian battery value chain. While these were identified as the key pillars for battery innovation, since the battery ecosystem is still nascent in Canada, they can be used to evaluate the state of the ecosystem, not just its innovation arm. By providing a snapshot of the battery ecosystem, practitioners can understand how their work is supporting strengthening the overall battery value chain.

The potential demand for batteries in Canada is then presented based on global projections and domestic policy targets. This section quantifies the two greatest opportunities by market size for electrification supported by batteries: transportation and electricity. This demand feeds into the targets in this report and can be used by decision makers to benchmark future domestic production and import potential for Canada.

The benchmarks presented in this report provide reference data to determine the success of Canada’s battery innovation ecosystem. Decision makers can use the technical benchmarks to decide the relative impact of new battery innovations against the backdrop of an existing, competitive field. Setting competitive targets allows for long-term planning of research, development, and demonstration (RD&D) program goals by prioritizing performance trade-offs to meet intended customer requirements. For OERD, benchmarking the Canadian battery ecosystem allows insight into progress made toward the goals of the SABI, and highlights gaps in the value chain where more support is needed.

2. Ecosystem

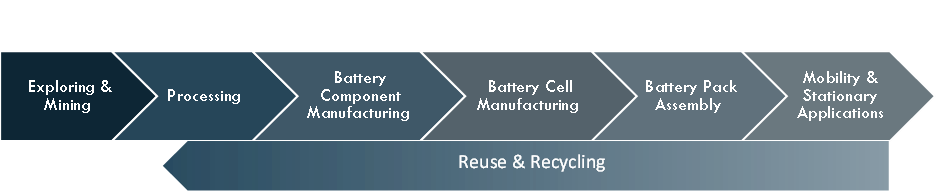

The Canadian battery ecosystem refers to firms and institutions established in Canada and activities involved in RD&D, the production, (re)use, and recycling of batteries. This includes the entire value chain, from sourcing critical minerals and manufacturing battery components to cell production, assembly, and eventual recycling (see Figure 1).

Figure 1: Visualization of the battery value chain

Figure 1 - Text version

The supply chain spans battery minerals extraction and refining, battery materials and component production, and cell and pack manufacturing. As the supply of battery inputs strains to keep up with growing demand, battery recycling and broader circularity efforts are necessary to extract maximum value and minimize waste, which completes the value chain.

Canada is recognized as a leading mining nation, and intends to create competitive supply chains for critical minerals and value-added products, processes and technologies for zero-emission vehicles, including Li-ion batteries, permanent magnets and specialty alloys.Reference [3] Canada has also invested in its transportation and automotive manufacturing industry, building on the fact that Canada is one of the world’s top 12 producers of light vehicles, with five global original equipment manufacturers (OEMs) assembling more than 1.4 million vehicles at their Canadian plants each year.Reference [4] The electrification of the automotive and transportation sectors has been guided by a “mines to mobility” approach. This approach seeks to develop a sustainable Canadian battery ecosystem for transport and electric vehicles (EVs). Large investments have been announced to support EV battery manufacturing, and supports have been put in place, including those under the Canadian Critical Minerals Strategy and through investment tax credits, to support the development of critical minerals mining and processing.Reference [5]

As stated in the SABI:

…establishing a fully decarbonized value chain for batteries that is secure and competitive requires Canada to have: the innovation infrastructure to develop homegrown solutions and expertise; and domestically located firms to take these innovations to market.

The Exploration & Mining segment of the value chain is well established with Canada producing 60 minerals and metals at almost 200 minesReference [6], including copper, graphite, iron, lithium and nickel, considered essential to leading Li-ion battery chemistries.Reference [7] In 2024, BloombergNEF ranked Canada first in its annual Global Lithium-ion Battery Supply Chain Ranking due to its abundance of critical minerals, as well as manufacturing and production advances, strong ESG credentials, and policy commitments. This assesses the potential of countries to build a reliable and sustainable battery supply chain. This year, Canada fell to second place (after China), largely due to slower-than-expected battery demand.Reference [8]

This section examines the approximately 250 firms distributed downstream from the Exploration and Mining segment, and its disproportionality to this upstream segment which motivates a more in-depth analysis of the middle of the value chain supporting its decarbonization, security, and competitiveness.

2.1. Battery Firms in the Supply Chain

This section focuses on the firms that support the segments downstream of Exploration & Mining in the battery value chain. These segments are considered more vulnerable in comparison to the upstream minerals sector (and downstream auto sector) in Canada, since most of the midstream is made up of smaller and less established entities, relying more on Canada's public innovation infrastructure to grow. The vulnerability is inherent to rapidly upscaling innovative technologies in a highly competitive global sector, which is largely affected by market drivers such as EV adoption, domestic policy targets, and trade policies. Furthermore, this vulnerability poses a security risk by overreliance on insecure supply chains and reduces the competitiveness of the transportation and electricity sectors.

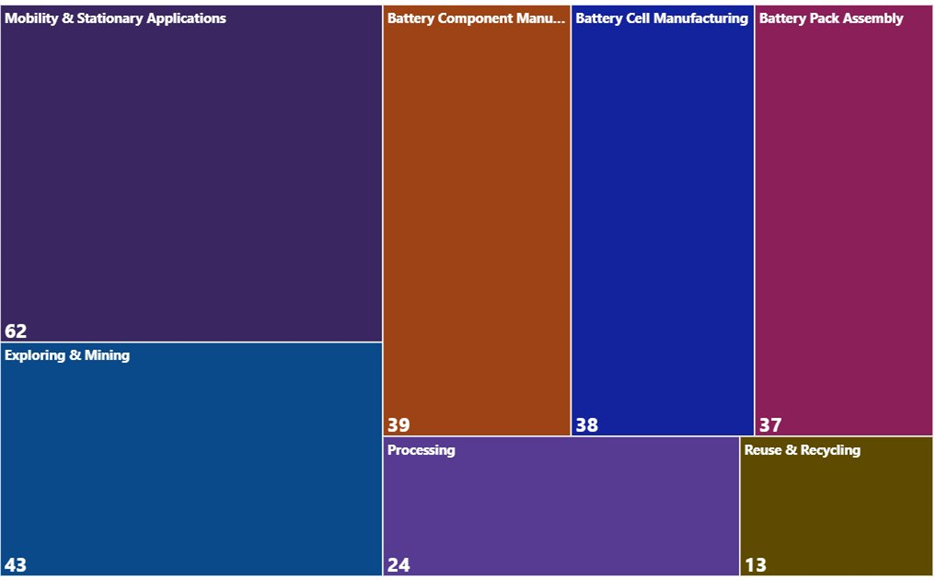

The Canadian battery ecosystem is comprised of around 250 companies along the battery processing, component, cell, pack, application, and reuse and recycling segments of the value chain (see Figure 2). Organizations were classified along the primary value chain associated with their Canadian operations. Both announced and paused operations are included in this accounting and no distinction is made between pre-commercial, foreign-owned, or established firms. This way, this ecosystem reflects the technology potential, rather than the industrial potential for the Canadian battery ecosystem.

Several of the companies have activities that span multiple battery value chain segments, but for the purpose of this review, each company was assigned a single ‘primary’ value chain segment defined as follows.

- Processing is considered the production of battery-grade reagents with >99% purity.

- Battery component manufacturing includes active battery materials and non-active components found inside a cell (as well as cathode precursor).

- Battery cell manufacturing produces semi-finished products that are capable of reversible cycling.

- Battery pack assembly includes assemblies of multiple cells wired together in series and parallel, and includes battery management systems.

- Mobility and stationary storage applications are considered end-use, where mobility includes OEMs of electric land, sea, and air vehicles. Stationary storage applications includes vendors of stationary storage, but not electric utilities of market actors.

- Reuse and recycling include the second-life application of cells after first use and the reconstitution and reinsertion of end-of-life and scrap battery material into upstream segments of the value chain, respectively.

Figure 2: Distribution of firm count by primary value chain segment along downstream segments of the battery value chain

Figure 2 - Text version

The distribution of firms in Canada across the different value chain segments:

- 62 firms having Mobility & Stationary Applications as their primary economic activity

- 43 firms having Exploration & Mining as their primary economic activity

- 39 firms having Battery Component Manufacturing as their primary economic activity

- 38 firms having Battery Cell Manufacturing as their primary economic activity

- 37 firms having Battery Pack Assembly as their primary economic activity

- 24 firms having Processing as their primary economic activity

- 13 firms having Reuse & Recycling as their primary economic activity

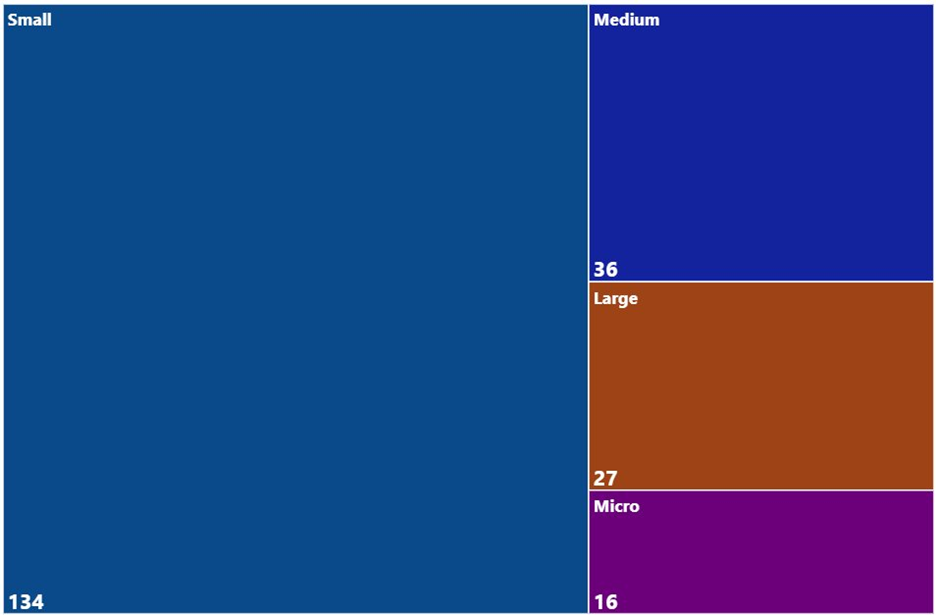

The lack of any large-scale component or cell manufacturing in Canada at time of writing this report reflects the immaturity of these value chain segments. Company size can be used as a rough indication of progress towards commercialization, with companies developing low TRL products likely to be micro-sized and small-sized, while companies with commercialized facilities likely to be large. This is not always true since large companies do invest in R&D at various TRLs. But in the absence of project level TRL data across all organizations, company size is used as a proxy for technology advancement towards commercialization. For instance, 77% of firms in the component segment and 63% of firms in the cell segment are micro- and small-sized. Most companies across all downstream segments, including vendors of mobility and stationary storage applications segment, are small companies, with cell, components, and processing companies having the greatest proportion of their total numbers being small firms (see Figure 3).

Figure 3: Relative size of companies across the downstream segments of the battery value chain (Micro: 1-4 employees, Small: 5-99 employees, Medium: 100-499 employees, Large: 500 or more employees)

Figure 3 - Text version

The distribution of companies in the Canadian Battery Value Chain classified by size:

- 134 small companies (5 to 99 employees)

- 36 medium companies (100 to 499 employees)

- 27 large companies (500+ employees)

- 16 micro companies (1 to 4 employees)

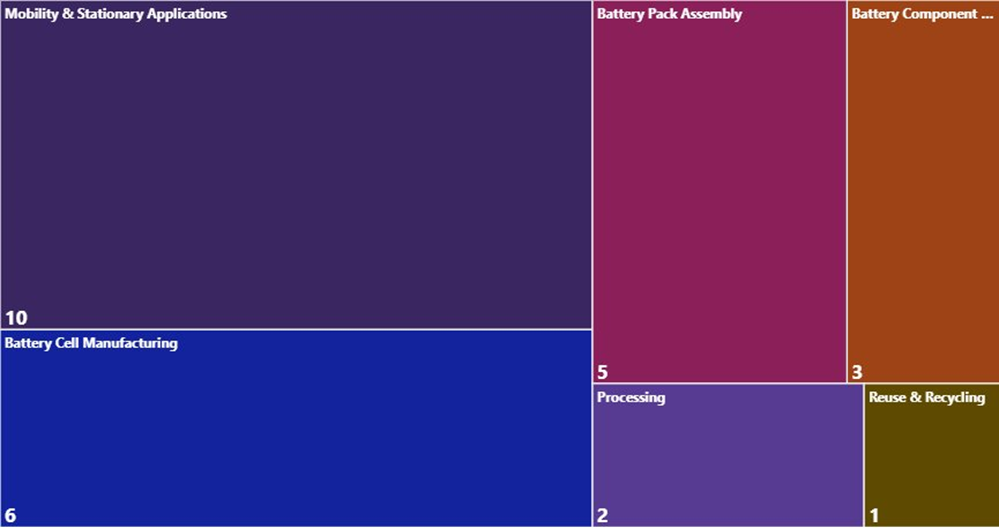

Figure 4 shows that large companies dominate in three segments: Mobility & Stationary Applications, Battery Cell Manufacturing, and Battery Pack Assembly. While the majority of the large companies from the Mobility & Stationary Storage segments are commercial, that is not the case for the other segments. Larger firms in the other segments are higher TRL, but still pre-revenue, and shows the high capital investment needed to build a vertically integrated supply chain in Canada.

Figure 4: Distribution of large companies (500 employees or more) across the downstream segments of the battery value chain

Figure 4 - Text version

The distribution of large companies in the downstream segments of the Canadian Battery Value Chain:

- 10 large companies active in Mobility & Stationary Applications

- 6 large companies active in Battery Cell Manufacturing

- 5 large companies active in Battery Pack Assembly

- 3 large companies active in Battery Component Manufacturing

- 2 large companies active in Processing

- 1 large firm active in Reuse & Recycling

Less than 10% of companies along the middle segments of the battery value chain, regardless of their size, operate across multiple value chain segments (see Figure 5). Presence in multiple value chain segments serves as a proxy for vertically integrated operations, highlighting that even in the case of larger companies, the capital investment demand is burdensome. An example of a vertically integrated company would be one developing an innovative chemistry for Li-ion batteries tailored for their energy storage deployment to support renewable energy generation. Such integration can support end application focussed innovation. However, Canadian companies working in multiple segments tend towards lower TRL and pre-commercial operations, or have planned deployments. This reality reinforces the vulnerability of the middle segments of the value chain.

Figure 5: Distribution of companies along the middle of the battery value chain possessing a primary, secondary, and tertiary value chain segment.

Figure 5 - Text version

The distribution of companies according to their active participation in the Canadian Battery Value Chain:

- 213 companies have economic activities in at least one segment of the value chain.

- 56 companies have economic activities in both a primary and secondary segment.

- 14 companies have economic activities in three or more segments of the value chain.

2.1.1. Processing

Processing of mined materials to battery grade reagents is the value chain segment with the second fewest number of firms in the Canadian battery ecosystem. This includes processing materials intended to supply the battery value chain, specifically Li-ion batteries: lithium, nickel, cobalt, manganese, copper, and graphite.

Battery grade lithium is processed either by refining minerals from spodumene/petalite concentrates or by extraction from underground reservoirs of lithium-rich brine.Reference [9] There are currently two lithium mines operating in Canada that supply within the country, limiting throughput to processing operations, but several advanced projects are in development. Reference [10] Projects planning to process lithium from brine are primarily located in the prairie provinces with projects planning to mine and process mineral concentrates being concentrated primarily in Ontario and Quebec. Canada does not currently have any commercial operations producing lithium battery chemicals.

Graphite is a critical battery mineral for anode electrode composition in li-ion batteries. Currently, Canada has one operating graphite mine (which is also the only one in North America), but this is believed to largely supply non-battery markets. Several advanced projects are in development that could mine and process battery-grade anode material. For nickel and cobalt, essential cathode components for high energy density NMC cells, Canada is a current mined producer but does not have any operating battery chemical production. However, like with lithium and graphite, there are several advanced projects advancing to mine more battery minerals and produce battery chemicals.

There are a number of processing and exploring & mining companies that have prospective operations in both segments, providing a path forward towards the growth of the segment in Canada. These potential processing projects are highly dependent on favorable market conditions and the continued development of the downstream ecosystem to support demand and may face challenges associated with highly concentrated global markets for processed battery minerals. Ongoing efforts in upscaling the processing industry bridges the gap between mining & exploration and end use battery applications, integral towards a vertically integrated “mines-to-mobility” battery industry.

2.1.2. Component Development and Manufacturing

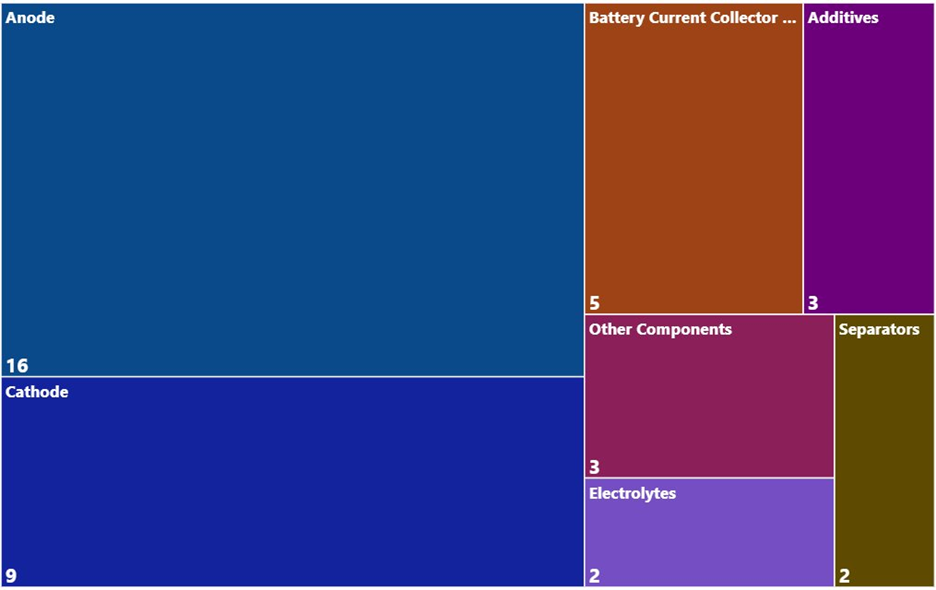

The component development and manufacturing segment has the greatest number of companies after mobility & stationary applications, although the majority are pre-revenue. This segment covers several different types of components, including cathodes, anodes, electrolytes, separators, current collectors, and membranes. Given the variety within this value chain segment, it is logical to see a spread across company sizes. Figure 6 below breaks down these companies into further types of battery components. Companies developing more than one of these components are counted once in each category.

Figure 6: Company distribution across battery component manufacturing

Figure 6 - Text version

Distribution of companies in the battery component manufacturing segment of the value chain:

- Anodes: 16 companies

- Cathodes: 9 companies

- Battery current collector foils: 5 companies

- Additives for battery component production: 3 companies

- Electrolytes: 2 companies

- Separators: 2 companies

- Other components (e.g., redox flow battery electrolyte, non-Li-ion reagents): 3 companies

Anodes show the largest number of companies working in this space but they are only micro-sized and small companies. This is in part due to the focus on next-generation anode materials to replace graphite. Silicon anodes are a promising candidate for this purpose but is still a lower TRL therefore most companies are still small and growing. Some firms working on graphite and lithium metal anodes but with further upstream operations in the value chain were tagged as processing, rather than component manufacturing. Overall, to anchor the battery supply chain in Canada further, more scale-up of domestic anode manufacturing is needed.

Cathode companies, conversely, are generally larger but in fewer numbers. This is driven by foreign direct investment in cathode plants alongside EV manufacturing. While the battery cathode innovation activities that do occur in Canada tend to focus on novel production of commercially mature cathode materials, there is less focus on lower TRL innovation and development of next-generation cathode chemistries. To grow Canada’s competitive advantage, a greater emphasis on new cathode technologies is needed.

There is one company commercially producing current collectors in Canada and a few planned facilities that will produce separators. Although separators are a non-active component of battery cells, they still influence performance of the battery and this provides an opportunity for more innovation focus.Reference [11] Likewise, current collectors are non-active components but affect battery performance depending on electrical conductivity, contact resistance, and corrosion resistance,Reference [12] yet only two companies are situated in the segment, leaving room for greater saturation.

While there are firms in Canada that focus on solid-state electrolyte cells and flow battery electrolytes, there is room for more innovation in conventional and next-generation liquid electrolytes for lithium-ion cells.

Other components include electrolytes, electrodes, and reagents for use in non-Li-ion cell compositions. Generally, companies with this designation are involved in vertically integrated operations towards an end-use application of non-li-ion long duration energy storage systems. These companies are at the first stages of commercialization or pursuing technology deployment at the demonstration scale, highlighting the necessity to produce components upstream in the case of novel architecture or chemistry end-use applications despite the increased capital investment requirement.

Given this relatively sparse presence in the Canadian ecosystem, more investment in these areas could boost the resilience of the supply chain and boost Canadian competitiveness.

2.1.3. Cell Development and Manufacturing

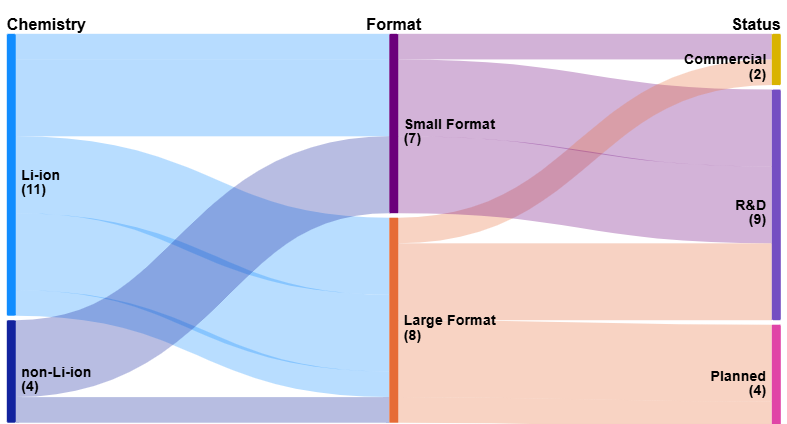

Cell development and manufacturing is a segment that is comprised of both smaller start-ups making cells for specialized applications as well as those targeting large-scale production for the mobility and stationary storage markets. Despite this presence, there is currently no large-scale cell production in Canada, with multiple projects on hold, discontinued or put at risk in recent years (see Figure 7).

Figure 7: Distribution of companies producing cells by chemistry, format, and commercial status. Large format cells are designated as (>20 Ah), with small format cells being below that threshold.

Figure 7 - Text version

The Sankey diagram illustrates the relationships between battery chemistry, format, and status:

Chemistry

- Li-ion: 11

- non-Li-ion: 4

Format

- Small format: 7

- Large format: 8

Status

- Commercial: 2

- R&D: 9

- Planned: 4

Flows indicate that most Li-ion chemistries connect to both small and large formats. Large formats are primarily linked to planned status, while small formats are linked with R&D and some commercial. Non-Li-ion chemistries mainly flow toward small formats and R&D status.

By number of companies, the battery cell development and manufacturing segment is among the larger ones, in the Canadian battery value chain, demonstrating strong potential for the ecosystem. There currently is only one company producing large-format, lithium-ion cells at a commercial scale leaves one company, and it is currently offshoring their cell manufacturing capabilities in Canada.

While lithium-ion is currently the dominant global battery technology, 50% of firms in this segment in the ecosystem specialize in non-lithium chemistries such as sodium-ion, zinc-ion and alternative cell concepts such as metal-air and flow batteries. These technologies are primarily suited to niche applications for the stationary storage market, which prioritize cost and other performance metrics over energy density.Reference [13],Reference [14] As a result, the subsegment is dominated by micro- and small-sized companies, and by proxy, indicates that battery technologies with non-lithium chemistry are generally lower TRL than their lithium-ion counterparts. Less than one third of firms in this segment focus on conventional lithium-ion technology, and the remainder are developing next-generation cell technologies such as lithium-sulfur, lithium-metal, and solid-state batteries. Increasing Canada’s capability to produce large-format lithium-ion cells is a noticeable gap in its battery ecosystem.

2.1.4. Battery Pack Assembly

The battery pack assembly segment is split between three main areas of focus: pack assembly for mobility and stationary use applications; battery management systems responsible for maintaining safe operations; and thermal management of cells so that degradation is minimized and there is no thermal runaway. In contrast to the more upstream segments, most companies in this segment are operating in a commercial capacity (see Figure 8).

Figure 8: Distribution of companies operating at a pilot scale, of pre-commercial status, and operating commercially in the Battery Pack Assembly value chain segment.

Figure 8 - Text version

Distribution of companies operating at different stages of technological development in the Battery Pack Assembly segment of the value chain:

- Pilot: 8%

- Pre-Commercial: 21%

- Commercial: 71%

The pack assembly subsegment accounts for most of the activity in the broader segment. Companies designated as pack assembly firms can be split generally along three business lines: producers; distributors; and integrators. Distributors are companies whose business model centers around the sale of third-party battery packs. Integrators may operate as battery management system configuration and thermal management setup. Distributors and integrators source their product, or critical components of their product from abroad, and these companies are all operating commercially. Producers are concentrated among large automotive OEMs with plans to vertically integrate battery cell manufacturing and pack assembly at their facilities. There remains a barrier of significant capital expense for companies commercializing pack assembly in Canada, necessitating continued support for the segment.

2.1.5. Mobility & Stationary Applications

The Mobility & Stationary Applications segment is the largest among the downstream segments of the battery value chain, and accordingly, has the greatest number of large companies and commercial operations. The stationary applications subsegment holds a wide range of applications, from residential battery storage, low temperature microgrid application for northern communities, and utility scale battery energy storage systems. The overwhelming majority of these companies are operating at a commercial scale, ranging from small to large.

The exception to this are vertically integrated companies specializing in alternative chemistry energy storage systems, which account for ~14% of the stationary storage companies. It is noted that the analysis of the stationary storage subsegment is non-exhaustive, nevertheless the distribution between mobility and stationary applications can be seen in Figure 9, and shows a greater number of stationary storage industry, by number, compared to mobility focussed companies.

Figure 9: Count of companies operating in stationery and mobility applications.

Figure 9 - Text version

The distribution of firms operating in the Canadian battery ecosystem by application:

- Stationary applications: 37 companies

- Mobility applications: 25 companies

The mobility applications subsegment is composed of transport electric vehicle companies, such as electric buses or trains, light duty vehicles such as e-bikes, medium & heavy-duty vehicles for construction and logistics operations, recreational vehicles for snow and marine transport, and passenger electric vehicles.

This EV passenger segment stands out as having almost no medium-sized companies or smaller, indicating the difficulty of growing to scale in this segment. It should be noted that this segment only considers battery-integrated EV manufacturing without considering either EV parts such as electric motors or tires. Given the dominance of large OEMs in this sector, it is unlikely that newcomers will easily compete to reach high TRL production without significant supports. However, the presence of these downstream players does provide opportunities for the midstream of the supply chain to partner with adopters of their technologies.

2.1.6. Reuse and Recycling

Finally, reuse and recycling of end-of-life batteries is currently the smallest segment of the supply chain. Firms recycling lithium-ion batteries in Canada are currently at capacity from supply of manufacturing scrap, despite the low volumes of end-of-life batteries, and this segment is set to grow significantly as EV and stationary storage systems are deployed and retired. Furthermore, end-of-life vehicle batteries supplement a growing battery pack reuse market, using second life batteries retaining at least 50% of their original capacity in battery energy storage systems.

The companies in this segment focusing on battery processing and materials recovery are small and medium sized homegrown companies. They show potential for future growth to support the anticipated battery recycling needs in Canada. However, their growth should be timed with EV adoption and retirement growth to ensure continued profitability. Larger companies exist in the end-of-life battery collection, however, given the size of this segment there is an insufficient supply for large capacity battery recycling at this time.

Call2Recycle’s 2022 primer on “Electric Vehicle Battery Management at End-of-Vehicle Life” projected four commercial battery material recovery companies operating in Canada by 2025, of those four, two are currently operating at that scale.Reference [15] While today, no large volumes of end-of-life batteries exist, greater supply in coming years will provide battery recycling companies at economies of scale. The Transition Accelerator’s Roadmap for Canada’s Battery Value ChainReference [16] outlines a minimum required recycling capacity of 27 GWh of batteries by 2035 to maintain its share of the North American market. This presents an opportunity to collocate recycling facility with existing battery production hubs while production facilities optimize their processes, and for recycling firms to feed production facilities once recycling volumes reach steady state.

2.1.7. Ecosystem Conclusions

The Canadian battery ecosystem is evolving from a resource-rich, innovation-driven network to one with the necessary operations to support a vision for domestic production. Significant domestic supplies of battery inputs exist in Canada, such as lithium, nickel, manganese, cobalt and graphite and plans are in motion to support the downstream sector with an emerging capacity to support mineral processing and battery component development. Canada is well-positioned to build a resilient, vertically integrated battery value chain; however, challenges remain. The critical middle segments remain vulnerable due to limited and delayed growth, affecting the establishment of a complete value chain. Securing industrial partnerships, targeting investments, and securing the ingenuity and presence of the Canadian battery industry can reinforce the middle segments, and make Canada’s battery value chain compete at a global stage.

2.2. Battery Innovation Infrastructure

The battery ecosystem is also made up of innovation infrastructure including physical and technological infrastructure, skilled and collaborative resources, and facilities that accelerate the development of new ideas by encouraging innovative thinking and risk taking. While these resources and activities exist in industry, they also exist as stand-alone battery innovation research centers in academia and as their own organizations.

Canada’s innovation infrastructure has been supported for many decades by research expertise in academia and laboratories across the country, and this continues today. Many research institutions and laboratories have expertise and capabilities to support battery innovation amongst other priorities. Today, there are multiple institutions dedicated to battery development specifically as their core business.

Battery innovation centers, generally focusing on lower TRL innovations, contribute vital capacity to generate Highly Qualified Personnel (HQP) and new technologies. These new technologies may eventually reach commercial viability and drive Canada’s economic competitiveness. These innovation centres provide an opportunity for existing for-profit firms to test their technologies and cross-collaborate in their field of work, enable access to equipment that could otherwise be out of reach, and train HQP to continue this work.

The following academic centres are worth noting as a testament to the growing investments in academic research in batteries technologies.

- CEGEP network – Training programs aimed at Battery and Electric Vehicle sectors

- Concordia University – Volt-Age Electrification Research Program

- Dalhousie University – Canadian Battery Innovation Centre

- McGill University – McGill Centre for Innovation in Storage and Conversion of Energy

- McMaster University – Centre for Mechatronics and Hybrid Technologies

- University of British Columbia – Battery Innovation Research Excellence Cluster

- University of Calgary – Western Canada Battery Consortium

- University of Toronto – Electrification Hub

- University of Waterloo – Ontario Battery and Electrochemistry Research Centre

These are in addition to public research facilities such as the National Research Council pilot-scale battery manufacturing line facility and their battery performance and safety evaluation research facility, and Hydro-Québec Research Institute (IREQ) Centre of Excellence in Transportation Electrification and Energy Storage. Battery innovation centers round out the Canadian battery ecosystem by anchoring battery clusters on a geographical basis, as seen in Figure 10.

Figure 10: Emerging Canadian Battery Innovation Clusters

Figure 10 - Text version

The map of Canada highlights four Emerging Canadian Battery Innovation Clusters located in British Columbia, Southern Ontario, Quebec, and Nova Scotia:

Western Canada Battery Cluster:

- University of BC Okanagan’s Battery Innovation Cluster

- University of Calgary’s Western Canada Battery Consortium

- E-One Moli

- NanoOne

Southern Ontario Automotive Cluster:

- University of Waterloo’s Ontario Battery and Electrochemistry Research Center

- University of Toronto’s Electrification Hub

- McMaster University – Center for Mechatronics and Hybrid Technologies

- Volkswagen – PowerCo

- Stellantis/LGES

- Commercial testing facilities: Flex-Ion, TÜV SÜD and Siemens

Quebec Battery Cluster:

- Hydro Quebec’s Center for Excellence

- NRC Boucherville Battery Prototyping Center

- McGill University’s Centre for Innovation in Storage and Conversion of Energy

- Concordia University’s Volt-Age Electrification Research Program

- Vallée de la Transition Énergétique : Blue Solutions and Nano One

- EcoPro Canada

Halifax Battery Cluster:

- Dalhousie University’s Canadian Battery Innovation Center

- NOVONIX Battery Technology Solutions

Western Canada Battery Cluster: Western Canada’s battery innovation presence is bolstered by the Battery Innovation Cluster at the University of British Columbia Okanagan, which includes a Battery Innovation Centre, planned to open in 2026, which will feature battery prototyping serving industry and academia, and the Western Canada Battery Consortium at the University of Calgary. These facilities are mainly focused on solid-state battery technologies and advanced manufacturing. E-One Moli has had an R&D facility in Maple Ridge, BC since the 1990’s and chose to expand on their existing lithium-ion R&D and manufacturing facility in 2023, although these plans have been halted as the parent company prioritizes its Taiwanese cell production. Nano One’s Innovation Hub in Burnaby, BC was expanded in 2023 to further their in-house innovation and production of cathode battery materials including lithium iron phosphate (LFP), lithium nickel manganese cobalt oxide (NMC), and lithium nickel manganese oxide (LNMO) cathode chemistries.

Southern Ontario Automotive Cluster: The Southern Ontario cluster is localized around its prominent automotive manufacturing base. The University of Waterloo has recently launched the Ontario Battery and Electrochemistry Research Center, which focuses on next-generation battery chemistries for high energy density. The University of Toronto is home to the Electrification Hub, also focusing on applications of batteries such as mobility needs. McMaster University’s Centre for Mechatronics and Hybrid Technologies focuses on advanced automotive technology, including battery testing, modelling and characterization. This cluster has attracted the most interest of companies looking to establish gigafactories in support of existing OEMs, such as the PowerCo and LGES gigafactories to supply Volkswagen and Stellantis respectively. Additionally, this area is home of commercial battery development and testing facilities such as: Flex-Ion who offers battery development from chemistry development, cell, module, and pack manufacturing; and TÜV SÜD who offers battery cycling and abuse testing as well as post-mortem analysis. At the time of writing, Siemens also announced that they will establish a Global AI Manufacturing Technologies R&D Center for Battery Production, initially located in Oakville, Toronto, and in Kitchener-Waterloo.

Québec Battery Cluster: The Quebec battery cluster is anchored by Hydro Quebec’s long-spanning work in battery innovation at the Center of Excellence in Transportation Electrification and Energy Storage, and further grown by recent investments by the provincial government in battery manufacturing through EcoPro, in Shawinigan, QC. The National Research Council’s pilot-scale battery manufacturing line, located in Boucherville, QC, facilitates prototyping small and large cells, using industry fabrication processes, de-risking new battery technologies. The Vallée de la transition énergétique (VTE) promotes an industrial park in Bécancour, QC, where investments seek to promote their goals for the battery sector. While not directly an R&D centre, this clustering has promoted itself as a test bed for innovative technologies. This cluster includes innovating companies such as Blue Solutions (specializing in solid-state batteries) and Nano One (LFP cathode active material). McGill’s Centre for Innovation in Storage and Conversion of Energy and Concordia University’s Volt-Age Electrification Research Program add to this innovation cluster, in addition to many other academic institutions with electrification expertise more generally.

Halifax Battery Cluster: The Halifax battery cluster is anchored by Dalhousie University, which has recently launched the Canadian Battery Innovation Center, which aims to accelerate scale-up of innovations by enabling construction of next generation battery cells that meet industrial standards and thereby demonstrate feasibility. Many innovations and HQP at leading battery/energy companies have come out of the Jeff Dahn Research Group lab in the last few decades, primarily focusing on material scale-up, grid storage, and sustainable cells. The Novonix Battery Technology Solutions division, with facilities located in the Halifax, NS area, provides state-of-the-art battery testing equipment for laboratory R&D, and offer pilot cell manufacturing and testing.

Future anchoring of these clusters could include more intentional partnerships in the form of “hubs” and infrastructure capable of producing cells in the final product-ready state (i.e. B-samples), such as large format cells produced at minimum industrial production rates.

3. Battery Deployment

The two largest applications driving demand for battery deployment are the transportation and electricity sectors. In transportation, batteries in EVs displace the need for fossil fuel combustion in an internal combustion engine. In the electricity sector, batteries can support a resilient electricity grid by storing electricity generated by renewable energy sources such as solar and wind, and using that energy to meet peak demand and provide fast and accurate grid balancing services, capable of displacing those provided by fossil fuel generators.

Measuring the deployment of batteries for these applications provides indicators toward the health and potential of the battery supply chain. Increasing demand derisks investments in the supply chain that rely on market stability and growth.Reference [17] Conversely, an observed slowdown in these deployments due to softening demand for EVs has created roadblocks for the battery sector, as seen in recent announcements to investments in Canada. Supply chain bottlenecks due to policy uncertainty or trade restrictions can also impact deployment.

3.1. Transportation

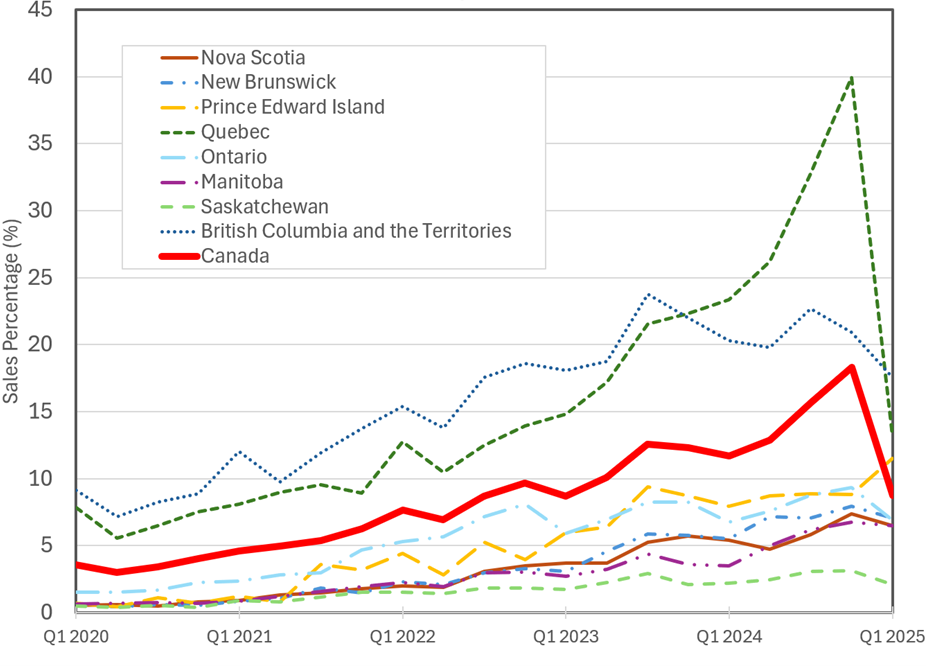

In 2023, the transportation sector was the second largest source of GHG emissions, accounting for 23% of total national emissions.Reference [18] To reach net-zero emissions in Canada by 2050, the transportation sector must transition away from internal combustion engine vehicles. To date, this transition has been almost fully driven by on-road light-duty battery electric vehicles (BEVs).Reference [19] To track this, EV sales as a percentage of total new passenger vehicle registrations is reported on a quarterly basis (see Figure 11).Reference [20] By assuming a vehicle lifetime of 15 years, 100% of new vehicles would need to be EVs by 2035 to meet the net-zero target by 2050.

Figure 11: National and provincial passenger EV registration statistics in Canada from 2020 to 2024. (Source: Statistics Canada)

Figure 11 - Text version

The line chart shows electric vehicle registrations by sales across Canadian from Q1 2020 to Q1 2025:

- Canada (red line): Sales increase steadily from ~3% in Q1 2020 to ~18% in Q4 2024, then drop slightly to under 10% in Q1 2025.

- Quebec (green dashed line): Shows the fastest growth, from ~8% in Q1 2020 to nearly 40% in Q4 2024, then falls sharply to under 15% in Q1 2025.

- British Columbia and Territories (blue dotted line): Second highest growth, rising from ~9% in Q1 2020 to its maximum ~24% in Q3 2023, before dropping below 20% by Q1 2025.

- Other provinces (Nova Scotia, New Brunswick, Ontario, Manitoba, and Saskatchewan): Show modest growth since Q1 2020, remaining below ~10% throughout the period. Prince Edward Island is the only province exceeding 10% by Q1 2025.

The data above, sourced from Statistics Canada, shows quarterly new EV registrations by province.Footnote a EV sales in Canada have been led by strong showings from Quebec and British Columbia who have exceeded the national average consistently. The decline in registrations in 2025 are largely driven by Quebec pausing its EV purchase subsidies from February 1 – March 31, 2025.Reference [21] This decline saw EV sales decline from over 18% to just under 9% of sales nationally, and demonstrates that shifts away from internal combustion engine vehicles are still highly dependent upon customer incentives.

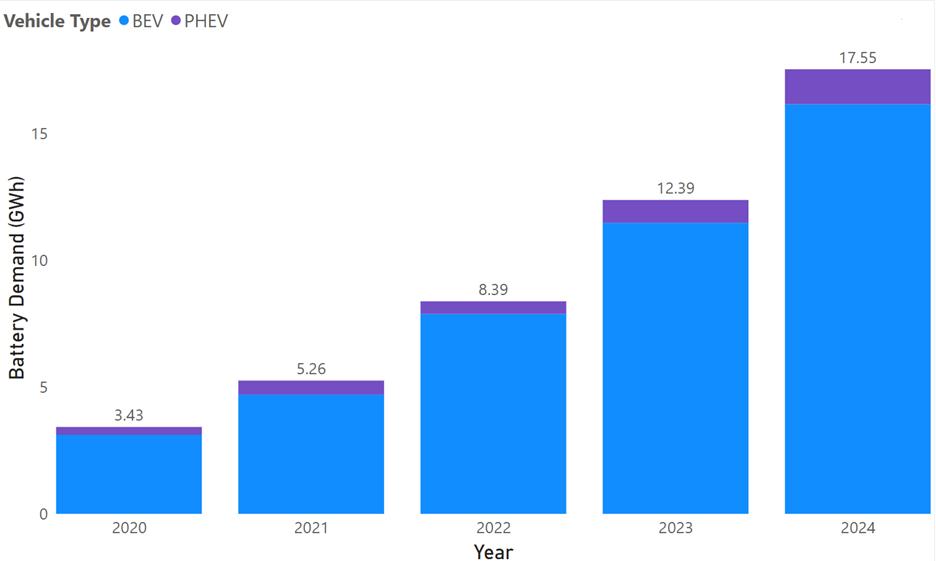

Based on available BEV and plug-in hybrid electric vehicle (PHEV) sales statistics, around 720,000 EVs were sold in Canada in the years 2020-2024.Reference [20] Assuming an average BEV battery pack size of 80 kWh (conservative estimate based on full capacity), and an average PHEV battery pack size of 20 kWh, the total battery demand owing to domestic passenger vehicle demand for these years is shown in Figure 12.

Figure 12: Annual Canadian battery demand for passenger battery electric and plug-in hybrid electric vehicles.

Figure 12 - Text version

The bar chart shows annual Canadian battery demand for passenger vehicles (GWh) from 2020 to 2024, split by vehicle type: BEV (blue) and PHEV (purple) segments. Demand from BEVs dominates over PHEVs.

- 2020: 3.43 GWh

- 2021: 5.26 GWh

- 2022: 8.39 GWh

- 2023: 12.39 GWh

- 2024: 17.55 GWh

These values resemble those projected under BloombergNEF’s EV outlook for the Net-Zero Scenario (Figure 13), with some margin of difference accounting for differences in assumptions in battery size.

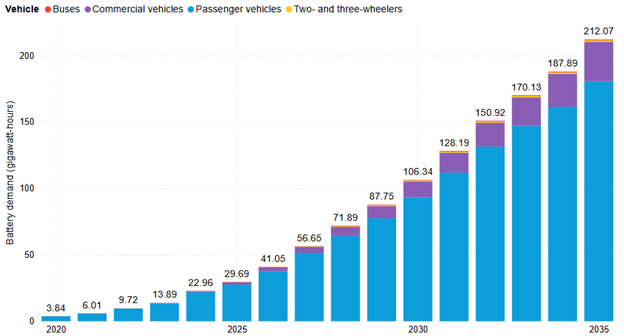

Figure 13: Annual Canadian battery demand in GWh for all vehicle types, assuming net-zero scenario by 2050. (Source: BloombergNEF)

Figure 13 - Text version

The bar chart shows Canadian battery demand by vehicle type under a net-zero scenario by 2050, with buses (red), commercial vehicles (purple), passenger vehicles (light blue), and two and three wheelers (yellow).

- 2020–2025: Battery demand rises from 3.84 GWh to 29.69 GWh, with passenger vehicles representing the greatest demand.

- 2025–2030: Battery demand grows to 106.34 GWh for all vehicle types. Passenger vehicles remain dominant (over 90 GWh), commercial vehicles reach ~10 GWh, while demand from other vehicle types remain low.

- By 2035: Battery demand reaches 212.07 GWh for all vehicle types, with passenger vehicles accounting for over 180 GWh, commercial vehicles ~30 GWh, and other vehicle types remaining minor contributors.

3.2. Electricity

Alongside its ZEV sale mandates, the Government of Canada has also set a target of achieving a net-zero electricity grid by 2035. While batteries are not a source of electricity generation, they are a directly enabling technology for non-emitting sources of electricity, projected at over 83 GW in 2035.Reference [16] To support this model, Energy Storage Canada, in their 2022 report titled Energy Storage: A Key Net Zero Pathway in Canada,Reference [22] outlined the need for 8-12 GW of energy storage capacity for the grid by 2035 and the Canadian Climate Institute, more ambitiously, laid out a target of 12 GW of energy storage capacity by 2030.Reference [23]

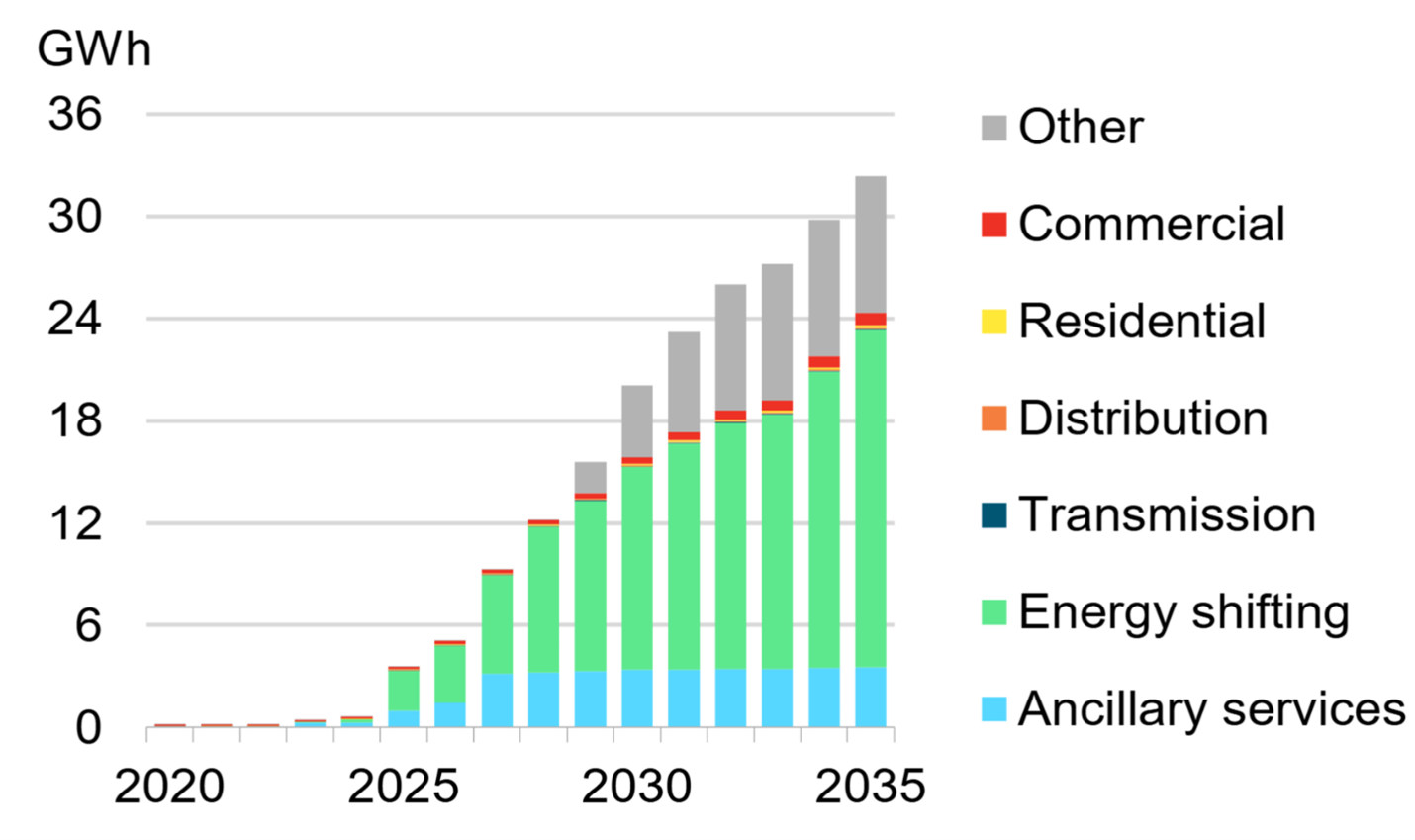

Figure 14 shows projected cumulative battery storage capacity in Canada up to 2035, which is not tied to any net-zero targets. Capacity additions are slated to increase significantly by the end of 2025, reaching approximately 4 GWh. This is primarily driven by energy shifting services such as energy arbitrage. By 2035, BloombergNEF projects a cumulative energy storage capacity of approximately 32.5 GWh. This corresponds to an annual capacity addition of approximately 3 GWh per year.

Figure 14: Projected cumulative stationary storage capacity in Canada assuming no major policy changes. (Source: BloombergNEF)

Figure 14 - Text version

The bar diagram presents cumulative battery energy storage capacity in Canada (2020–2035) under a scenario with no major policy changes, broken down by application: commercial (red), residential (yellow), distribution (orange), transmission (dark blue), energy shifting (green), ancillary services (light blue), and other (grey).

- 2020–2025: Storage capacity reaches ~4 GWh, with energy shifting and ancillary services leading adoption.

- 2025–2030: Storage capacity reaches ~20 GWh. Energy shifting and ancillary services are still leading adoption and account for 15 GWh, while other applications contribute ~5 GWh.

- By 2035: Storage capacity exceeds 32 GWh. Energy shifting reaches over 18 GWh, ancillary services remain at 3 GWh adopted by 2027. Other applications reach 10 GWh.

- Overall, commercial, residential, transmission, and distribution applications show relatively small adoption compared to other applications.

BloombergNEF predicts that in 2025, approximately 91% of the global stationary storage demand will be met by LFP-based lithium-ion batteries, while 6% is met by NMC-based lithium-ion chemistry. The role of NMC is expected to further decrease to negligible levels due to limitations in cost and lifetime while LFP maintains dominance with 81% of the total demand, and sodium-ion batteries are expected to grow to 10%.

3.3. Total Demand

In the last few years, new passenger vehicle sales in Canada have hovered around 1.8 million per year. Assuming an average battery size of 80 kWh per vehicle, Canada could require around 144 GWh of annual battery production in 2035 to meet its domestic needs, if 100% of vehicles were battery or hybrid EVs.

The International Energy Agency’s Global EV Outlook 2024 estimates a total annual demand of approximately 10.2 TWh of batteries for mobility and stationary storage applications in 2035 to be on track for net-zero by 2050.Reference [19] Of this, 6.9 TWh are set to be from passenger vehicles, 0.8 TWh from stationary storage, and another 2.5 TWh from other mobility applications including two/three-wheelers, busses, and trucks. To determine the expected demand from non-passenger EVs in Canada, a similar ratio of passenger to non-passenger vehicle battery demand is assumed to hold true for both global and Canadian demand, which yields an annual battery demand of approximately 52 GWh. Overall, this means Canada would require approximately 196 GWh of annual battery production in 2035 to meet the domestic demand for transportation-related applications.

Assuming the higher forecasted demand of 12 GW of energy storage by 2035 to be on track for net-zero, and assuming an average of 4 hours of storage for these deployments, 48 GWh of storage would be required. Based on current technology, assuming an average system lifetime of 10 years, then an annual battery production of 4.8 GWh per year would be needed to meet domestic demand while maintaining 12 GW of grid storage. In the current policy scenario, an annual production of 3 GWh of stationary storage batteries would be needed.

Combining this with the previous requirement of 196 GWh for total vehicle demand, Canada could require 200 GWh of annual battery production in 2035 to meet its domestic needs across these two segments.

4. Battery Technology Benchmarking and Targets

The SABI outlines five frameworks, two of which are used to define the most impactful performance metrics for batteries. Footnote b The Battery Performance Framework highlights five general performance metrics that describe the technical merit of any battery: energy density, power density, cost, safety, and lifetime. The Battery Sustainability Framework describes additional needs to meet the energy trilemma and sustainability goals.

From these, this report highlights the following six performance metrics as the most impactful for relativizing battery innovation and its potential for meeting the goals of the SABI.

- Energy density: The energy that can be stored in a cell (measured in watt-hours, Wh).

- Power density: The flow of energy that can be input or output during charging and discharging, respectively, normalized by mass (expressed in W/kg) or volume (expressed in W/L).

- Lifetime: The ability of a battery to charge of discharge for many cycles over a long period of time with limited degradation of performance.

- Safety: The requirements established to prevent harm or damage from battery malfunction during use, storage, handling, and disposal.

- Cost: The manufacturing cost of a battery typically expressed as $/kWh or $/kg.

- Sustainability: The waste byproducts of battery manufacturing, the most prominent being greenhouse gas emissions, expressed in kgCO2eq/kWh and water.

An expanded explanation of these metrics is included in Appendix B and can be used to better understand how each metric is derived. Other important metrics such as extreme temperature performance, charging speed, and range are primarily dependent on the metrics above and on the application utilizing the battery, so are not treated distinctly here. This report offers an intermediate understanding of these six performance metrics to better appreciate their impact on other market driven requirements.

The following sections present benchmarking data for leading technologies, for each performance metric, and provide targets for future performance. The battery technology benchmarking was conducted by aggregating state-of-the-art performance data of current battery technologies. This includes publicly available data on battery materials, cells, and systems of commercially available and deployed batteries, as well as information on next-generation battery technologies reported by industry and in peer-reviewed literature. Target battery requirements for different applications and from various battery technology roadmaps were collected and compared to provide context for the use-cases of different battery technologies and designs, and to set expectations for future state-of-the-art performance targets. For consistency, the benchmarks are offered at the cell level, as battery performance is largely driven from design and optimizations at the cell level and offers most opportunity for innovation.

Publicly accessible performance data of commercially available battery cells for multiple chemistries, capacities, form factors, and applications are aggregated to provide a benchmark of modern battery capabilities.Reference [24] These reference cells and their applications are shown in Table 1. The technology in commercially available cells tested today likely originates from RD&D activities conducted in years prior; the data presented in this section reflects the state-of-the-art in battery technology from approximately the early to late 2010s.

| Cell Manufacturer | Product Name | Target Applications |

|---|---|---|

| A123 Systems | 26700 NCA GL | motorsports, Formula 1Reference [25] |

| BYD | Blade C102F | electric vehiclesReference [26] (2022 long-range BYD Dolphin) |

| BYD | C45F-302Ah | electric power systems, solar energy storage systems, electric vehicles, electric motorcycles, e-bikes, micro-mobility applicationsReference [27] |

| CATL | Tesla Model 3 | electric vehiclesReference [24] (2023 Tesla Model 3) |

| Farasis | P79B3 | electric vehiclesReference [28] |

| HiNa Battery | NACR26700 MP3.0 (A) | e-bikes, portable and residential energy storage systemsReference [29] |

| LG Energy Solution | INR21700-M58T | consumer electronics, e-scooters, e-bikes, power toolsReference [30] |

| LG Chem | E66A | electric vehiclesReference [31] (Audi e-tron GT quattro, 2019 Porsche Taycan) |

| LG Chem | E61V | electric vehiclesReference [24] (2019 Audi e-tron) |

| Molicel | INR21700-P45B | electric vehicles, electric vertical take-off and landing aircrafts (eVTOL), micro-mobility, home appliances and other applicationsReference [32] |

| Panasonic | Tesla Model Y 21700 | electric vehiclesReference [24] (2020 Tesla Model Y) |

| Primearth EV Energy | Hybrid Toyota Camry | hybrid electric vehicleReference [24],Reference [33] (2019 Hybrid Toyota Camry) |

| Samsung | CS1200R | electric vehiclesReference [20] (2019 BMWi3) |

| Samsung | BMW 530e | plug-in hybrid electric vehiclesReference [20] (2019 BMW 530e) |

| Tesla | Tesla Model Y 4680 | electric vehiclesReference [34] (2022 Tesla Model Y) |

While it may not be possible to independently maximize each battery performance metric, it is only necessary to ensure that the battery performance envelope exceeds its application requirements. Therefore, the benchmarks and targets presented below are offered to decision-makers to understand the relative value of innovation ventures, although trade-offs are inherent to purpose-driven design and proper discretion should be used when selecting performance targets. See Appendix B for more discussion on trade-offs and composite metrics.

4.1. Cell Energy Density

Cell energy density benchmarks of commercially available cells from Table 1 are presented here along three views.

- Volumetric and gravimetric energy densities by cell format (Figure 15)

- Volumetric and gravimetric energy densities by cell chemistry (Figure 16)

- Gravimetric energy densities and capacity by cell format (Figure 17)

Targets for energy density are selected on the basis of cell performance and affordability.

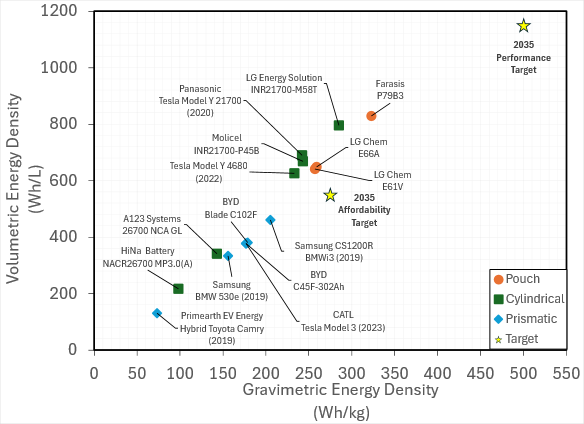

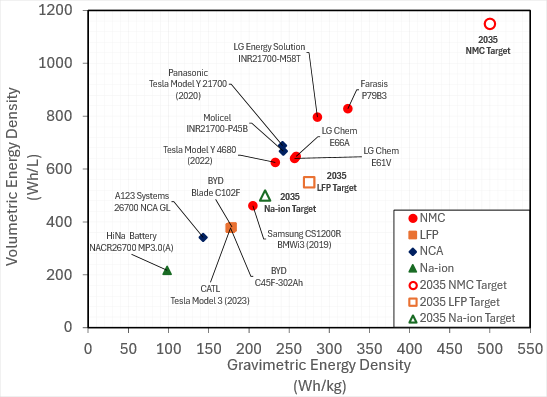

2035 Performance Target: High performance is generally achieved through use of NMC cathodes, and innovations on the anode are expected to push energy densities further. Figure 15 and Figure 16 show a 2035 gravimetric energy density target of 500 Wh/kg and a volumetric energy density target of 1150 Wh/L.

Affordability Target: Affordable batteries must balance low cell manufacturing costs and energy densities suited to their end application. However, high performance cells may require more expensive cell manufacturing techniques and input materials to achieve their high performance. LFP is a likely candidate for meeting both affordability and acceptable performance, with a 2035 gravimetric energy density target of 270 Wh/kg and a volumetric energy density target of 550 Wh/L.

Na-Ion Target: Finally, this section would not be complete without acknowledging the potential of sodium-ion batteries as a competitive alternative to lithium-ion batteries for stationary and low-range mobility storage applications. For this battery type, a long-term target is outlined in Figure 32 for a gravimetric energy density of 220 Wh/kg and a volumetric energy density of 500 Wh/L.

Figure 15: Volumetric (measured in Wh/L) and gravimetric (measured in Wh/kg) energy densities for selected commercially available cells labeled by cell format (pouch, cylindrical, or prismatic). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).Reference [24]

Figure 15 - Text version

The scatter plot compares gravimetric and volumetric energy densities for three commercially available cell formats — pouch, cylindrical, and prismatic —as well as two 2035 targets:

- Pouch cells (orange circles): Gravimetric energy density of ~250 to ~325 Wh/kg and volumetric energy density of ~620 to ~810 Wh/L.

- Cylindrical cells (green squares): Gravimetric energy density of ~100 to ~275 Wh/kg and volumetric energy density of ~200 to ~800 Wh/L.

- Prismatic cells (light blue diamonds): Gravimetric energy density of ~75 to ~200 Wh/kg and volumetric energy density of ~100 to ~450 Wh/L.

- 2035 targets (yellow stars):

- Affordability Target: 270 Wh/kg gravimetric and 550 Wh/L volumetric.

- Performance Target: 500 Wh/kg gravimetric and 1150 Wh/L volumetric.

Figure 16: Volumetric (measured in Wh/L) and gravimetric (measured in Wh/kg) energy densities for selected commercially available cells labeled by cell chemistry (NMC, LFP, NCA, Na-ion). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).Reference [24]

Figure 16 - Text version

The scatter plot compares gravimetric and volumetric energy densities across four commercially available cell chemistries, with marker shapes identifying each chemistry: NMC (circles), LFP (squares), NCA (diamonds), and sodium-ion (triangles).

- NMC (red circles): Current gravimetric energy densities range from ~200 to ~325 Wh/kg, with volumetric energy densities from ~450 to ~850 Wh/L. A 2035 target (open red circle) indicates 500 Wh/kg and 1150 Wh/L.

- LFP (orange squares): Current gravimetric energy density of ~175 Wh/kg and volumetric energy density ~350 Wh/L. The 2035 target (open orange square) indicates 270 Wh/kg and 550 Wh/L.

- NCA (blue diamonds): Current gravimetric energy densities range from ~150 to ~240 Wh/kg and volumetric energy densities from ~350 to ~700 Wh/L.

- Na-ion (green triangles): Current gravimetric energy density of ~100 Wh/kg and volumetric energy density ~200 Wh/L. A 2035 target (open green triangle) indicates ~225 Wh/kg and ~300 Wh/L.

- Values toward the upper right corner represent higher energy density. Among the chemistries shown, NMC achieve the highest gravimetric and volumetric energy densities.

Figure 17: Gravimetric energy densities (measured in Wh/kg) and nominal cell capacities (measured in Ah) for selected commercially available cells labeled by cell format (pouch, cylindrical, or prismatic). Energy densities are measured by discharging from 100% SOC at C/10 rate at 25°C until reaching the lower voltage limit (either 2V or 2.5V).Reference [24]

Figure 17 - Text version

The scatter plot compares cell capacity in logarithmic scale against linear gravimetric energy density for commercially available pouch, cylindrical, and prismatic cell formats:

- Pouch cells (orange circles): Capacities between 60-80 Ah and gravimetric energy density between 250 and 330 Wh/kg.

- Cylindrical cells (green squares): Capacities between 3-20 Ah and gravimetric energy density between 100 and 290 Wh/kg.

- Prismatic cells (light blue diamonds): Capacities between 4-300 Ah and gravimetric energy density between 70 and 210 Wh/kg.

Takeaways

- As seen in Figure 15, the volumetric and gravimetric energy densities of commercial battery cells are highly correlated.Footnote c

- The anode and cathode chemistry play a significant role in determining the cell energy density (see Appendix C for supporting calculations). For instance, the prismatic BYD and CATL cells with LFP and graphite chemistry in Figure 15 and Figure 16 have nearly identical energy densities (177-179 Wh/kg and 377-381 Wh/L). However, NMC and nickel, cobalt, aluminum oxide (NCA) chemistries mostly have higher energy densities with more variation compared to LFP. The variation in NMC cells’ energy density is in part due to the variation in cathode and anode composition: NMC cathode compositions with higher nickel content and graphite anode compositions with silicon incorporation typically have higher energy densities. Other commercial pairings are outlined below.

The Farasis P79B3 NMC pouch cell is comprised of an NMC cathode with greater than 90% Ni composition and a graphite anode with some silicon incorporation, and it has the highest energy density of the selected cells (323 Wh/kg and 829 Wh/L).Reference [28],Reference [35]

The LG Chem E66A NMC pouch cell is comprised of an NMC cathode with 70% Ni composition (LiNi0.7Mn0.2Co0.1O2) and a graphite anode, and it has an intermediate energy density (259 Wh/kg and 648 Wh/L).Reference [31],Footnote [36]

The Samsung CS1200R NMC prismatic cell is comprised of an NMC cathode with 60% Ni composition (LiNi0.6Mn0.2Co0.2O2) and a graphite anode, and it has a lower energy density (205 Wh/kg and 461 Wh/L).Reference [37],Reference [38]

- As shown in Figure 16 sodium-ion batteries such as the HiNa Battery NACR26700 MP3.0(A) have lower energy density compared to conventional lithium-ion chemistry. This 3Ah cylindrical cell is comprised of a sodium, copper, manganese, and iron oxide cathode paired with an anthracite-derived soft carbon anode with energy densities of 98 Wh/kg and 217 Wh/L.Reference [39]

- The energy density of battery cells can span a wide range, as shown in Figure 15 and are optimized for the target application’s requirements, as shown in Figure 17. However, cell capacity alone is insufficient to determine a battery’s application, as both small and large capacity cells may be used for the same application. For example, one of the 2020 versions of the Tesla Model Y uses 4.6 Ah cylindrical cells from Panasonic with NCA cathode and graphite anode, and one of the 2022 versions of the same vehicle uses 22 Ah cylindrical cells with NMC811 (LiNi0.8Mn0.1Co0.1O2) cathode chemistry and graphite anode.Reference [40],Reference [41]

- Figure 17 shows how there is a growing trend toward increasing cell capacity and a shifting preference for large-format cells (especially prismatic cells) in mobility and stationary storage applications. This is because they can increase the cell volumetric energy density due to improved volume efficiency of the active material share and lower the cost due to reduction of manufacturing steps that scale with number of cells.Reference [27],Reference [42], Reference [43],Reference [44]

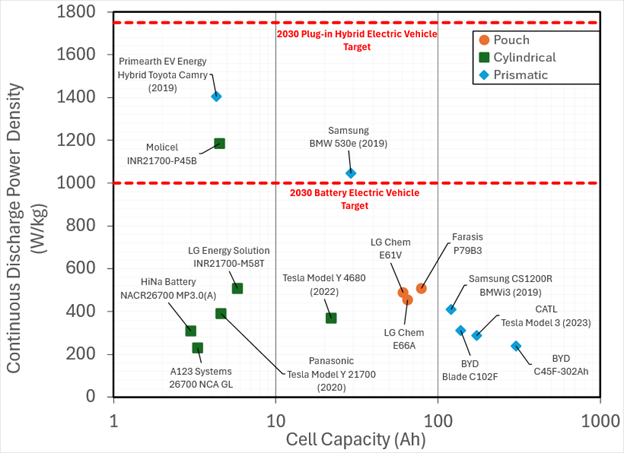

4.2. Cell Power Density

The continuous discharging power capability of the cells in Table 1, are presented in Figure 18. The peak power capability, or the maximum power that can be supplied for 5 minutes starting from 100% SOC is included for reference in Figure 19.

Importantly, battery cells used in hybrid electric vehicles (HEVs), PHEVs, and BEVs exhibit variation in power capability, as shown in Table 2. This table highlights how three prismatic cells from Primearth EV Energy and Samsung shown in Figure 15, Figure 17, and Figure 18 serve vehicles of similar size but with different levels of electrification, namely the 2019 Toyota Camry HEV, the 2019 BMW 530e PHEV, and the 2019 BMWi3 BEV.

Targets for continuous discharge power density are shown in Figure 18 for BEVs and PHEVs.

BEV Target: BEVs require less power density, balancing instead high power and energy densities to achieve the desired range. The longer-term target for BEV batteries is 1000 W/kg.

PHEV Target: PHEVs require higher power density compared to BEVs, utilizing smaller cells. The longer-term target for PHEV batteries is 1750 W/kg.

Figure 18: Continuous discharge power densities (measured in W/kg) and nominal cell capacities (measured in Ah) for selected commercially available cells labelled by cell format (pouch, cylindrical, or prismatic). Continuous discharge power densities are determined from discharging the cell from 100% SOC at 25°C until reaching 10% SOC and either reaching the lower voltage limit (either 2 or 2.5V) or reaching a maximum surface temperature of 68°C.Reference [24]

Figure 18 - Text version