This page contains annual reports providing a snapshot of potential major energy and natural resources projects across Canada within the next 10 years. To find the latest information on projects being advanced through the Government of Canada’s Major Projects Office, including those outside the energy and natural resources sectors, visit: Major Projects Office

ISSN 2817-5646

Cat. No. M2-24E-PDF

© His Majesty the King in Right of Canada, as represented by the Minister of Energy and Natural Resources, 2025

For information regarding reproduction rights, contact Natural Resources Canada at copyright-droitdauteur@nrcan-rncan.gc.ca.

Table of Contents

- Executive Summary

- Major Project Trends By Sector

- Energy Sector

- Mining Sector

- Forest Sector

- Clean Technologies

- Methodology

- Appendix

Executive Summary

The Major Projects Inventory (MPI) provides an annual snapshot of key natural resource projects in Canada that are either currently under construction or are planned within the next ten years (2024 to 2034). The inventory includes major projects that increase, extend or improve natural resource production, as well as information on their value, timing and geographic location.

As of September 2024, there are 504 major projectsFootnote 1 under construction or planned over the next ten years in Canada in the energy, forest and mining sectors, which have a combined potential capital value of $632.6B. This is an increase from 2023 in both the overall project count (from 493 projects) and capital value (+10.9% from $570.5B)Footnote 2.

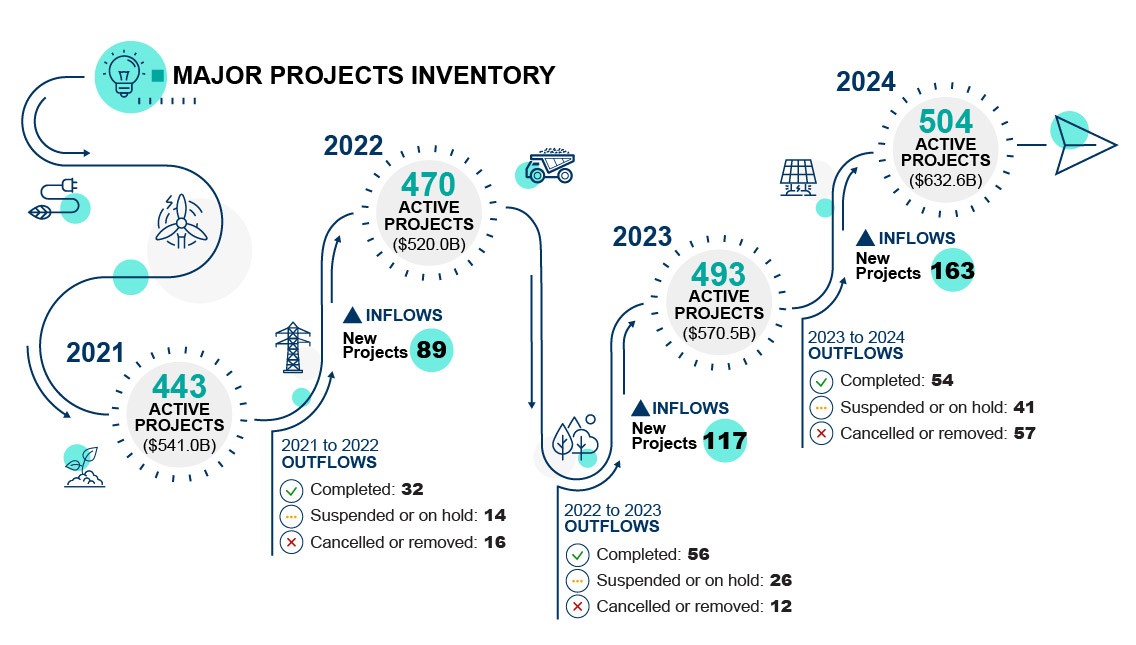

Figure 1: Inflow and Outflow of Projects and Value in the MPI, 2021 to 2024

Text description

Image depicting changes to the Major Projects Inventory between 2021 and 2024.

In 2021, the total number of active projects was 443 ($541B).

Between 2021 and 2022: 89 new projects were added; 32 projects were completed and therefore removed from the inventory; and 30 projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed.

In 2022, the total number of active projects was 470 ($520B).

Between 2022 and 2023: 117 new projects were added; 56 projects were completed and removed; and 38 projects became inactive and were removed. In 2023, the total number of active projects was 493 ($570.5B).

Between 2023 and 2024: 163 new projects were added; 54 projects were completed and removed; and 98 projects became inactive and were removed. In 2024, the total number of active projects was 504 ($632.6B).

Between 2023 and 2024, there were more projects added to the inventory than projects removed, leading to an increase in the overall project count.

- 163 projects were added to the inventoryFootnote 3, representing an increase of $176.9B in potential capital investment.

- 54 projects were removed from the inventory because they were completed and began production, representing $76.0B of actual investment.

- 49 projects were removed from the inventory because they were put on hold, suspended, or cancelled, representing $28.7B in potential investment.

- 49 projects were removed from the inventory following a verification review with Provinces and Territories and subject matter experts, representing $22.1B of investment (e.g., project not sufficiently developed, duplicate projects).

Energy

Canada is viewed as a world leader in hydroelectricity, nuclear power, and hydrogen and is well positioned to benefit from rising domestic and global demand. Potential projects in the energy sector include oil, petrochemicals and non-emitting electricity generation, transmission, distribution, storage, and grid modernization in the transition to “net-zero”. Projects in both the hydrocarbon and non-emitting energy sectors continue to advance decarbonization efforts. Carbon capture, utilization and storage (CCUS) offer the potential to offset emissions. Currently, the energy sector directly or indirectly supports nearly 663,000 jobs and accounts for 10.1% of the Canadian economyFootnote 4.

There are 340 energy projects in the 2024 inventory with a combined value of $510.0B.

- There are 3 fewer energy projects than in 2023, but the total capital value of active energy projects has increased by $37.7B (+8.0%).

- Growth in potential investment is mainly due to nuclear (+100.8%) and wind (+115.8%) projects, whose total value has more than doubled since the last report to $78.6B.

- 3 out of 5 energy projects (205 projects) are classified as using clean technologyFootnote 5, with a total potential investment of $192.1B.

Mining

Canada holds vast mineral reserves, and global demand continues to drive investments in areas such as critical minerals for electric vehicles (EVs) and green technologies, including battery production. The mining sector directly or indirectly provides about 711,000 jobs and represents 5.9% of the Canadian economyFootnote 6. In the 2024 inventory, there are 138 mining projects with a combined value of $117.1B.

- This is an increase of 9 mining projects and $23.5B (+25.1%) in total capital value since 2023.

- About half (67) of mining projects would process or extract some form of critical minerals, worth $72.4B in potential investment.

- Of these critical minerals mining projects, 36 projects valued at $41.7B would extract or process copper, nickel or lithium, three key components of EV batteries.

Forests

The forest sector is an important contributor to Canada’s economy, serving as a key source of prosperity for people and communities across the country. The sector directly or indirectly supports almost 367,000 jobs and accounts for 1.8% of the Canadian economyFootnote 7. The Canadian forest sector has traditionally manufactured products such as lumber, panels, wood pulp, newsprint and other printing and writing papers. The sector is also driving new economic activity through value-added products, and maintaining a focus on innovation within the bioeconomy, which includes various products derived from wood.

The 2024 inventory includes 26 forest projects with a combined value of $5.5B.

- This is an increase of 5 forest projects and $0.9B (+18.6%) in total capital value since 2023.

- 10 forest projects are classified as using clean technology, for a total of $2.0B in potential investment.

Clean Technology

Clean power and low carbon fuels are essential for Canada to meet its climate goals. The clean technology market presents opportunities to assist with transition to low carbon economies, both domestically and abroad. Clean technology products support more than 205,000 jobs and represents 1.4% of the Canadian economyFootnote 8. Clean technology projects in the 2024 inventory are found in the energy and forest sectors, and are primarily comprised of renewable electricity or non-emitting energy projects, including carbon capture and storage.

Of all 504 projects in the inventory, about 43% (215 projects) are classified as using clean technology, for a total of $194.2B in potential investment.

- There are 18 fewer clean technology projects than in 2023, but the total capital value of active clean technology projects has increased by $36.7B (+23.3%).

Major Project Trends by Sector

Energy Sector

There are 340 energy projects in the 2024 inventory with a combined capital value of $510.0B, down from 343 projects in 2023, but representing an increase in capital value of $37.7B from 2023 ($472.3B).

Energy projects span many sub-sectors, including those in the oil and gas industry (e.g., oil sands, offshore, natural gas, LNG, export terminals, storage facilities, and pipelines) and in electricity generation and transmission (e.g., clean technologies, nuclear, and power lines).

British Columbia (42.9%) and Alberta (28.5%) account for almost three quarters of the total value of major energy-related projects. Ontario and Quebec follow, with 13.6% and 7.5% respectively.

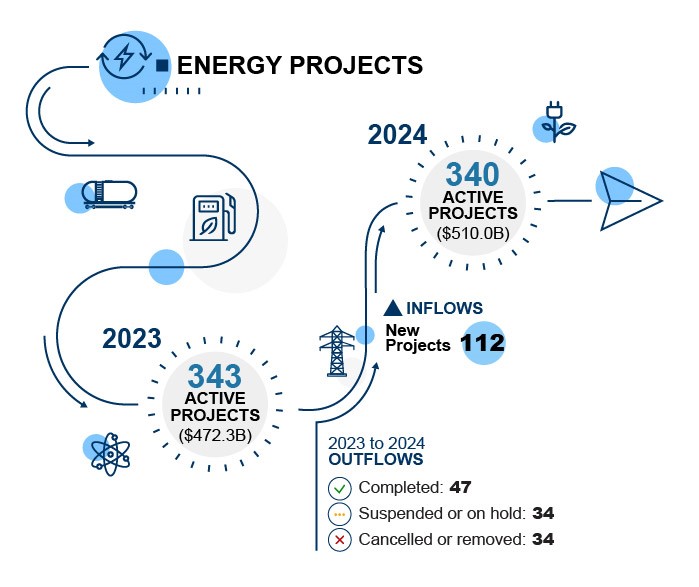

Figure 2: Inflow and Outflow of Energy Projects, 2023 to 2024

Text description

Image depicting changes to the inventory of energy projects between 2023 and 2024.

In 2023, the total number of active projects was 343 ($472.3B).

Between 2023 and 2024:

- 112 new projects were added;

- 47 projects were completed and therefore removed from the inventory; and

- 68 projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed.

In 2024, the total number of active projects was 340 ($510.0B).

Trends

In Canada, a series of regulations, policies, deployment programs, collaborative cross-jurisdictional initiatives, and provincial and territorial initiatives influence investment decisions. Recent examples include:

- Coal phase out by 2030

- Natural gas performance standards

- Revenue-neutral carbon tax

- Net zero 2050 legislation

- Upcoming Clean Electricity Regulations

- Efforts related to EV deployment

- Transition towards a “net-zero” electricity system to begin in 2035

These are complemented by regional strategies, interties, provincial regulatory environments, market structures and business models, policies such as net-metering arrangements, and fiscal measures like tax credits and equipment rebates. Together, these measures, which are designed to facilitate investment and sustainable development, could prove daunting for some potential investors.

Additionally, the transition to “net-zero” will require major investments in decarbonising current operations, along with enhancing non-emitting electricity generation, transmission, distribution, storage, and grid modernization. These investments will largely serve to meet demands from increasing electrification in other sectors.

An important current growing area of investment for Canada is new “net-zero” petrochemical facilities, including Dow Chemical’s proposed $11.5B “net-zero” ethylene and derivatives complex. There is also growing interest in ammonia production to export hydrogen to international markets.

World-leading low-emitting liquefied natural gas (LNG) projects are also advancing in Canada, in support of global energy security and transition from higher emitting fuels. For example, LNG Canada Phase 1 ($47.9B) is expected to begin exporting in 2025 and the Woodfibre LNG ($6.9B) and Cedar LNG ($4.6B) projects are anticipated to be best-in-class greenhouse gas emissions performance facilities, with operational dates expected in 2028. In parallel, Canada continues to advance decarbonisation of upstream natural gas production to reduce emissions along the full value chain.

Canada is the 4th largest oil producer and has the 4th highest proved oil reserves in the worldFootnote 9. Growth in Canadian crude oil production is being driven by the Trans Mountain pipeline expansion project (TMX) where 590K barrels per day of new capacity has been added. New oil sands projects will need to come online to fill the pipeline. For example, the Mildred Lake ($3.3B) and the Blackrod ($2.9B) oil sands projects are expected to boost Canada's oil sands production.

The TMX expansion pipeline is designed to diversify Canada's crude oil market to Southeast Asian countries (e.g., China, South Korea, Japan) and India. In addition, exports to the US west coast market are growing through an increase in tanker traffic from the port of Vancouver.

Further, Canada’s abundant supply of low-cost and lower emitting petrochemical feedstock (e.g., propane, natural gas) results in lower operational costs and petrochemical products life-cycle emissions. This is Canada’s key competitive advantage to other petrochemical producing jurisdictions worldwide.

Canada’s greatest competition for the attraction of energy investments is the US, which offers a larger selection of financial incentives to attract projects. To level the playing field, Canada announced a suite of investment tax credits. The impact of these tax measures may be affected by a shorter construction season and limited availability of specialized contractors needed to support the construction of petrochemical facilities. This may result in higher initial capital costs and longer investment return period for investments in Canada as compared to the US.

| 2021 | 2022 | 2023 | 2024 | |

|---|---|---|---|---|

| Total Energy Projects | 305 ($450B) |

320 ($427B) |

343 ($472.3B) |

340 ($510.0B) |

| Oil and Gas-related | 106 ($339B) |

96 ($294B) |

87 ($318.6B) |

67 ($296.2B) |

| Electricity Generation and Transmission | 176 ($102B) |

179 ($106B) |

182 ($97.4B) |

188 ($118.9B) |

| OtherFootnote * | 23 ($8.9B) |

45 ($26.6B) |

74 ($56.2B) |

85 ($94.9B) |

In terms of potential investment, the inflow of 112 projects in 2024 valued at $136.9B was greater than the outflow of 115 projects valued at $107.4B. The most significant incoming projects in terms of potential value included Phase 1 of LNG Canada’s export facility in Kitimat, British Columbia ($47.9B) and Nuclear Waste Management Organization’s (NWMO) Adaptive Phased Management Deep Geological Repository in Ontario ($26.0B).

The largest outgoing items included the Trans Mountain Pipeline Expansion in British Columbia and Alberta ($34.0B) and the TransCanada Coastal GasLink Pipeline Project in Dawson Creek, British Columbia ($14.5B), both of which are completed and in production.

Major projects have faced increases in construction costs, including labour, materials, and equipment. The three largest upward revisions to potential investment included:

- Woodfibre LNG project in Squamish, British Columbia (revised from $1.6B to $6.9B),

- Dow Chemical’s Net-Zero Polyethylene Facility in Fort Saskatchewan, Alberta (revised from $10.0B to $11.5B),

- AltaLink’s Central East Area Transmission project in various parts of Alberta (revised from $82M to $332M).

Mining Sector

There are 138 mining-related projects (e.g., mine constructions, redevelopments, expansions, and processing facilities) in the 2024 inventory, representing $117.1B in potential investment. Metal mines (e.g., gold, copper, nickel, zinc) account for about three quarters of the value of major mining-related projects. Non-metal mines (e.g., potash, diamonds) and coal mines account for most of the remainder.

Projects in British Columbia accounted for the largest share of the combined value of mining projects across the country at nearly one third (30.3%), followed by Quebec (20.2%), Ontario (17.3%), and Saskatchewan (17.1%). The remainder is distributed across all provinces and territories, except for Prince Edward Island.

| 2021 | 2022 | 2023 | 2024 | |

|---|---|---|---|---|

| Total Mining Projects | 119 ($89B) |

124 ($88B) |

129 ($93.6B) |

138 ($117.1B) |

| Metals | 80 ($54.9B) |

91 ($65.6B) |

99 ($73.6B) |

98 ($82.8B) |

| Non-Metals | 15 ($17.9B) |

12 ($13.8B) |

13 ($11.7B) |

21 ($24.2B) |

| Coal | 16 ($12.8B) |

15 ($6.2B) |

12 ($6.5B) |

14 ($8.4B) |

| Other (processing, smelters, etc.) | 8 ($3.3B) |

6 ($2.6B) |

5 ($1.8B) |

5 ($1.7B) |

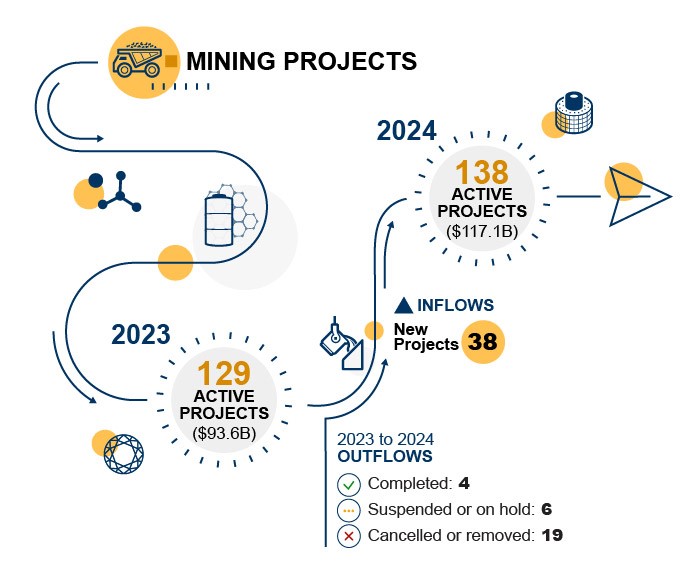

Figure 3: Inflow and Outflow of Mining Projects, 2023 to 2024

Text description

Image depicting changes to the inventory of mining projects between 2023 and 2024.

In 2023, the total number of active projects was 129 ($93.6B).

Between 2023 and 2024: 38 new projects were added;

- 4 projects were completed and therefore removed from the inventory; and

- 25 projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed.

In 2024, the total number of active projects was 138 ($117.1B).

Trends

Canada’s mining sector is strategically positioned to strengthen its global standing by leveraging vast mineral reserves and a robust project pipeline across key metals and minerals.

Growth in the sector is driven by rising demand for critical minerals, especially those essential for EVs and green technologies, as well as by a solid gold production bolstered by record high prices.

While challenges exist, the sector's potential remains substantial, driven by continued investments that are paving the way for the development and expansion of mining projects across the country.

Investment is pivotal for Canada's mining sector as it relies on a steady stream of exploration projects to replace aging mines and sustain mineral output. The Canadian Critical Minerals Strategy, launched in 2022 with nearly $4B in funding, aims to enhance the supply of responsibly sourced critical minerals, and bolster domestic and global value chains for the green and digital economy. This strategy supports and enhance:

- Economic growth

- Climate action

- Reconciliation with indigenous communities

- Global security

- Partnerships

Key elements of the strategy include tax credits for critical mineral development, such as the Critical Mineral Exploration Tax Credit and Clean Technology Investment Tax Credit, which are expected to attract further investment into the sector.

Canada has many assets supporting its mining sector competitive advantage:

- Diverse and extensive mineral resources (e.g., cobalt, copper, gold, iron ore, nickel, potash, silver, zinc, and promising lithium projects) offer significant growth opportunities

- Political and economic stability provides a reliable business environment throughout the lifespan of mining assets

- The availability of capital, skilled labour, and robust infrastructure supports efficient and cost-effective mining operations

- The presence of multinational firms and leading junior firms in exploration and development further enhances Canada’s competitivity

While short-term risks (e.g., geopolitical conflicts, market slowdowns, and fluctuations in commodity prices) pose challenges, the long-term outlook for Canada’s mining sector remains promising. The rising demand for critical minerals, driven by the clean energy transition, along with Canada's efforts to be a leader in the global lithium-ion battery supply chain, underscores its investment appeal. Continued focus on expanding production capabilities and attracting global investment will be key to maintaining Canada’s competitive edge and seizing opportunities in the global mining market.

An inflow of 38 projects valued at $37.2B offset the outflow of 29 projects worth $17.1B, leading to an increase of 9 projects which, combined with upward revisions to the value of existing projects, brought the overall capital value to $117.1B. The highest valued projects include the Kerr-Sulphurets-Mitchell (KSM) project in British Columbia ($8.4B) and Stage 1 of the Jansen Potash project in Saskatchewan ($7.5B).

In terms of new mining projects, the highest valued are Stage 2 of the Jansen Potash project ($6.4B) and Newmont & Teck Resources’ Galore Creek copper and gold mine in British Columbia ($5.2B). As for outgoing items, the largest is the Baldy Ridge Extension Project in British Columbia ($1.6B), which is completed and in production.

Forest Sector

In the 2024 inventory, there are 26 major forest projects across Canada, representing $5.5B in potential investment. Since last year’s update, the number of forest projects increased by 5 and the combined capital value of all active forest projects increased by $0.9B.

Nine projects in Quebec account for more than 40% of the combined value of active forest projects in Canada. The remainder of the value is spread across New Brunswick (21.9%), Nova Scotia (11.2%), Alberta (11.2%), Saskatchewan (7.3%), British Columbia (6.1%), and Northwest Territories (0.4%).

| 2021 | 2022 | 2023 | 2024 | |

|---|---|---|---|---|

| Total Forest Projects | 19 ($2.5B) |

26 ($4.1B) |

21 ($4.6B) |

26 ($5.5B) |

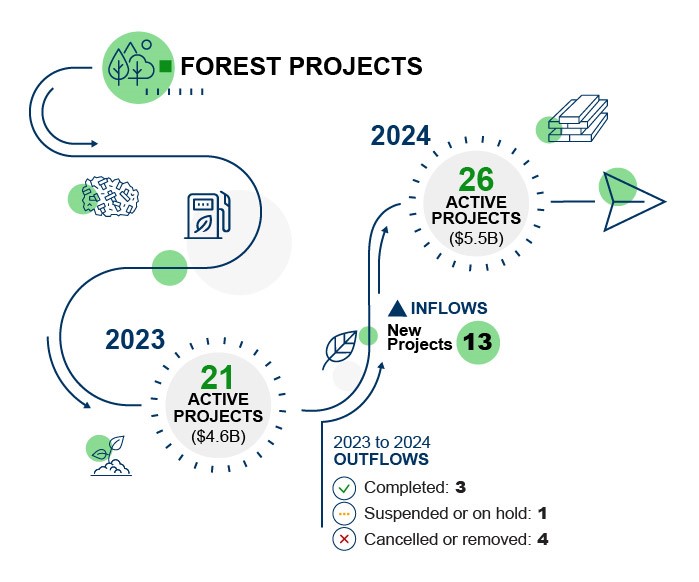

Figure 4: Inflow and Outflow of Forest Projects, 2023 to 2024

Text description

Image depicting changes to the inventory of forest projects between 2023 and 2024.

In 2023, the total number of active projects was 21 ($4.6B).

Between 2023 and 2024:

- 13 new projects were added;

- 3 projects were completed and therefore removed from the inventory; and

- 5 projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed.

In 2024, the total number of active projects was 26 ($5.5B).

Trends

Investment decisions in Canada’s forest sector are heavily impacted by the current and forecasted state of wood supply, and evolving regulations and policies. As Canada continues to pursue a “net-zero” future, prioritize the protection of old-growth forests and species at risk, and handle natural disturbances of increasing frequency, investors are weighing these trends alongside regulatory requirements to access timber.

Investors are also attentive to the fluctuating prices of forest products. Prices for lumber and other solid wood products have remained low in 2023 and over the first half of 2024, after falling in mid-2022 as the US and Canadian economies slowed in response to high interest rates. The housing sector in both countries slowed from the elevated levels reached in 2021, especially in the single-detached units' category. Pulp prices also lowered in late 2023, but steadily increased into 2024 due to global supply constraints including production disruptions and pulp mill closures.

Additional factors influencing investment decisions include:

- Persistent problems with transportation

- High production costs

- Decreased product demand

- Long-term fibre shortages that challenge both lumber and pulp producers

Lumber producers faced additional difficulties with US softwood lumber duties alongside low lumber prices, which has led to production curtailments and closures over the past year.

The availability of skilled workers needed to ensure growth is also a growing concern. In Canada, the forest sector is grappling with shortages of skilled labour, particularly in rural areas where forest activities are more concentrated, and the current labour force is aging: half of the forest sector labour force is expected to retire within 20 years, compared to about 40% for all industries.

Looking ahead, the outlook for Canada’s forest sector will largely depend on macroeconomic conditions, including interest rate movements. Wildfires are also an ongoing concern, causing negative impacts on wood supply, particularly in Quebec and Western Canada. However, government programs focused on expanding housing supply are expected to encourage construction activity and long-term demand for solid wood products, providing support for the industry.

For the pulp and paper sub-sector, the demand for packaging products is expected to grow as e-commerce sales continue to increase. This can support pulp and paper producers as they continue to respond to structural declines in demand for products like newsprint.

The sector is also driving new economic activity through value-added products, and maintaining a focus on innovation within the bioeconomy, which includes various products derived from wood. There have been large investments in mass timber and biochar production. Two new mass timber facilities were announced over the past year with $249M of planned investment. Carbonity, a partnership between Quebec’s Airex, Groupe Rémabec and France-based SUEZ, plans to invest $80M in a new biochar plant. When operational, it will be Canada’s largest biochar plant at 100K tonnes per year in production capacity.

Some of the largest projects in the sector include Enerkem’s biofuel facility under construction in Varennes, Quebec ($1.2B), J.D. Irving’s Saint John Pulp Mill upgrades in New Brunswick ($1.1B), and Mondi Group’s Hinton Pulp Mill expansion in Alberta ($0.6B).

In the 2024 inventory, 13 new forest projects were added, totalling $2.8B in potential capital investment. The largest project was the new J.D. Irving’s Saint John Pulp Mill upgrades in New Brunswick ($1.1B). 8 projects were removed from the inventory this year, of which 3 had been completed and gone into production.

Clean Technologies

In the 2024 MPI, there are 215 energy and forest projects that are classified as clean technology projects, representing $194.2B in potential investment.

- One in four clean technology projects are hydro projects, accounting for 15.6% of the potential capital value of clean technology projects (58 projects valued at $30.4B).

- The remaining clean technology projects are primarily bioenergy projects (41 projects valued at $12.6B), solar projects (36 projects valued at $8.8B), wind projects (33 projects valued at $26.8B), and 25 projects classified in the inventory as “other” worth $23.8B (e.g., hydrogen projects).

- There are also 3 nuclear projects – all in Ontario – that account for more than a quarter of the potential investment in clean technology projects ($51.8B).

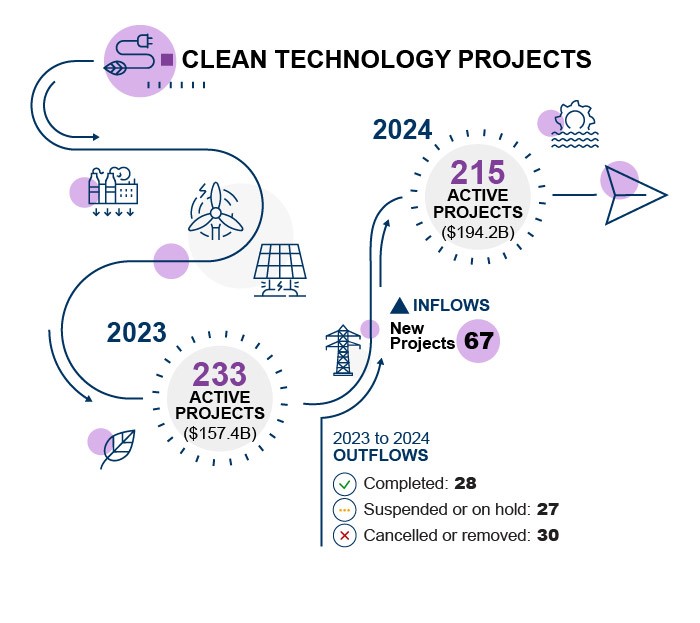

Figure 5: Inflow and Outflow of Clean Technology Projects, 2023 to 2024

Text description

Image depicting changes to the inventory of clean technology projects between 2023 and 2024.

In 2023, the total number of active projects was 233 ($157.4B).

Between 2023 and 2024:

- 67 new projects were added;

- 28 projects were completed and therefore removed from the inventory; and

- 57 projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed.

In 2024, the total number of active projects was 215 ($194.2B).

While project counts for clean technology projects decreased between 2023 and 2024 by 18, the potential capital costs increased by 22.1% ($36.7B).

A total of 67 projects valued at $67.1B in potential investment were added: 18 hydro, 16 wind, 14 solar, 7 bioenergy, 2 energy storage, 1 nuclear, and 9 “other.” In 2024, 85 clean technology projects were removed from inventory, of which 28 projects valued at $9.5B were completed: 11 wind, 6 solar, 6 bioenergy, 4 hydro, and 1 “other.”

Trends

Clean power and low-carbon fuels are crucial for Canada to meet climate goals. Canada is a world leader in hydroelectricity, nuclear power, and hydrogen and most electricity generation in Canada comes from non-greenhouse gas emitting sources. Wind and solar photovoltaic energy are the fastest growing sources of electricity in Canada, while biofuels and EVs also play an important role in reducing the climate impact of transportation in the country.

The growth of the global clean technology market presents opportunities for Canada, while challenges arise from the global competition to attract investments, notably the US Inflation Reduction Act and the EU Green Deal. Canada is responding through measures such as Investment Tax Credits and continues to advance opportunities for collaboration in clean technology and innovation, thus seizing the generational opportunities afforded by the ongoing transition to low-carbon economies both here and abroad.

Clean technology projects included in the MPI are largely renewable electricity projects (e.g., hydro, wind, solar, biomass, tidal, geothermal) and non-emitting energy projects, such as nuclear, biofuels, and carbon capture and storage. These projects are subsets of the energy and forest sector totals.

Larger projects include the Pathways Alliance Carbon Capture Storage Hub Phase 1 project in Alberta ($16.5B), Peace River Site C Hydro project in British Columbia ($16.0B), 2 nuclear refurbishment projects in Ontario ($13.0B and $12.8B), and the Dow Chemical’s Net-Zero Polyethylene Facility in Alberta ($11.5B).

| 2021 | 2022 | 2023 | 2024 | |

|---|---|---|---|---|

| Total Clean Technology | 178 ($104B) |

197 ($118B) |

233 ($157.4B) |

215 ($194.2B) |

| Hydro | 58 ($39.2B) | 63 ($44.8B) | 78 ($37.4B) | 58 ($30.4B) |

| Bioenergy | 31 ($8B) | 35 ($9.4B) | 47 ($14.3B) | 41 ($12.6B) |

| Solar | 22 ($2.2B) | 30 ($3B) | 31 ($6.2B) | 36 ($8.8B) |

| Wind | 41 ($14.6B) | 35 ($13.4B) | 32 ($12.4B) | 33 ($26.8B) |

| Carbon Capture and Storage | 2 ($11.3B) | 6 ($15.5B) | 9 ($38.3B) | 8 ($38.3B) |

| Tidal | 6 ($0.3B) | 7 ($0.4B) | 7 ($0.4B) | 4 ($0.2B) |

| Geothermal | 5 ($0.4B) | 4 ($0.4B) | 4 ($0.4B) | 4 ($0.4B) |

| Nuclear | 4 ($27.4B) | 3 ($26.1B) | 2 ($25.8B) | 3 ($51.8B) |

| Energy Storage | 0 | 0 | 0 | 2 ($1.1B) |

| Multiple | 1 ($0.03B) | 1 ($0.03B) | 1 ($0.03B) | 1 ($0.03B) |

| Other1 | 8 ($0.5B) | 13 ($5.3B) | 22 ($22.1B) | 25 ($23.8B) |

1 “Other” includes initiatives such as hydrogen projects.

Methodology

The MPI captures information on major natural resource projects in Canada that are either currently under construction or planned in the next ten years. The inventory includes projects that increase, extend, or improve natural resource production (e.g., new extraction and infrastructure projects, major processing facilities, and large expansion projects). Spending on exploration and general-purpose infrastructure projects (e.g., multi-purpose highways) is excluded.

To be included in the inventory, projects must meet minimum capital thresholds:

- $50M for projects in energy and mining

- $20M for electricity and forest sector projects

- $10M for clean energy and clean technology projects

Projects with capital estimates below the thresholds, while recognized as important contributions to overall investment, are excluded due to limited data availability.

A variety of data sources are used to update the inventory, including databases maintained by Natural Resources Canada and other federal, provincial, and territorial government departments, company releases, and publicly accessible websites. The inventory is based solely on information that is in the public domain.

The inventory includes information on the value, timing, and geographic location of projects. Potential capital costs are presented in current dollars. These are estimates of the project’s total cost as reported by the project proponent and are not intended to represent the project’s actual or yearly spending figures. These capital valuations are validated annually by provincial and territorial counterparts in nominal terms as per project finance reporting.

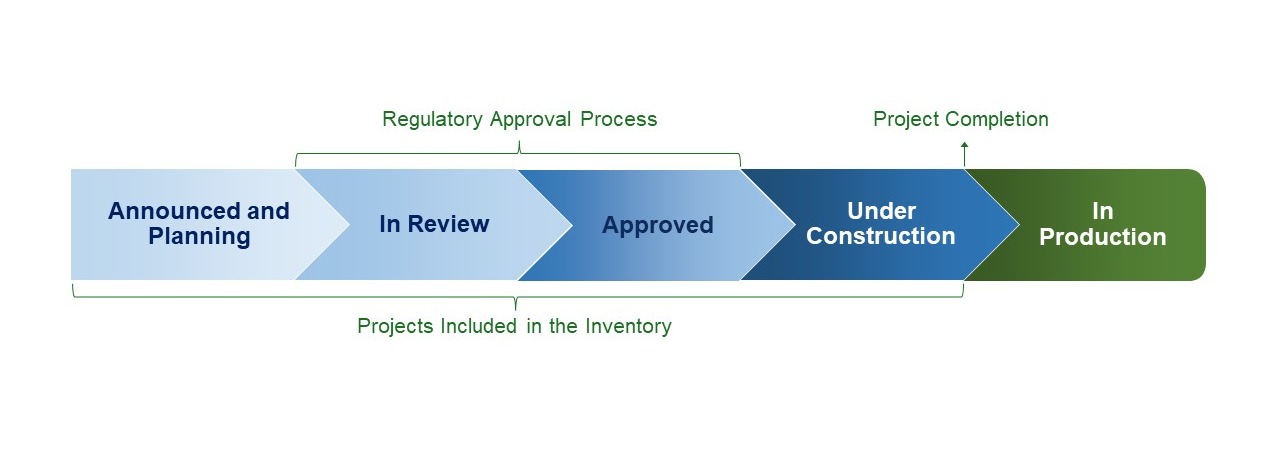

Projects included in the inventory are categorized according to their stage of development. A project typically progresses through the following stages:

- Announced and Planning: planned projects that have been publicly announced but where regulatory approvals have not been submitted

- In Review: planned projects that have submitted applications for regulatory approvals but are still under review

- Approved: planned projects that have received all major regulatory approvals, i.e., the approvals required to start construction but for which construction has not yet begun

- Under Construction: projects for which construction is underway

- Post-Review Planning: an additional stage to account for projects which have been rejected and returned to a planning phase in order to submit revised documents for further review

Figure 6: Project Stages Included in the 2024 MPI

Full text

Figure 6 shows a progress bar that follows project stages from announcement and planning to production. There are 5 key stages:

- Announced and Planning

- In Review

- Approved

- Under Construction

- In Production

The regulatory approval process takes place during the review and approval stages 2 and 3. The project is completed once the construction stage 4 is completed. Projects included in the major projects inventory fall under stage 1 to 4, before project completion.

Projects are classified as having been added, completed, put on hold, suspended, cancelled, or removed since the previous annual update by the following definitions:

- Added projects: new projects that have been announced since the previous update or older projects that have come within the scope for inclusion based on newly available data

- Completed projects: projects that have moved past the construction phase and into the production phase, or have otherwise been completed

- On hold projects: projects which have been temporarily interrupted and are expected to resume progression within a short period of time, typically 2 to 6 months

- Suspended projects: projects (previously planned or under construction) that have been delayed for a long period or officially suspended by the proponents

- Cancelled projects: projects (previously planned or under construction) that have been officially cancelled by the proponents

- Removed projects: projects that are no longer within the inventory’s scope due to newly available information (e.g., because they no longer meet the minimum capital thresholds)

Updates to the 2024 inventory were made between June and September 2024, and reflect public information newly available since the 2023 inventory update in May 2023.

Appendix

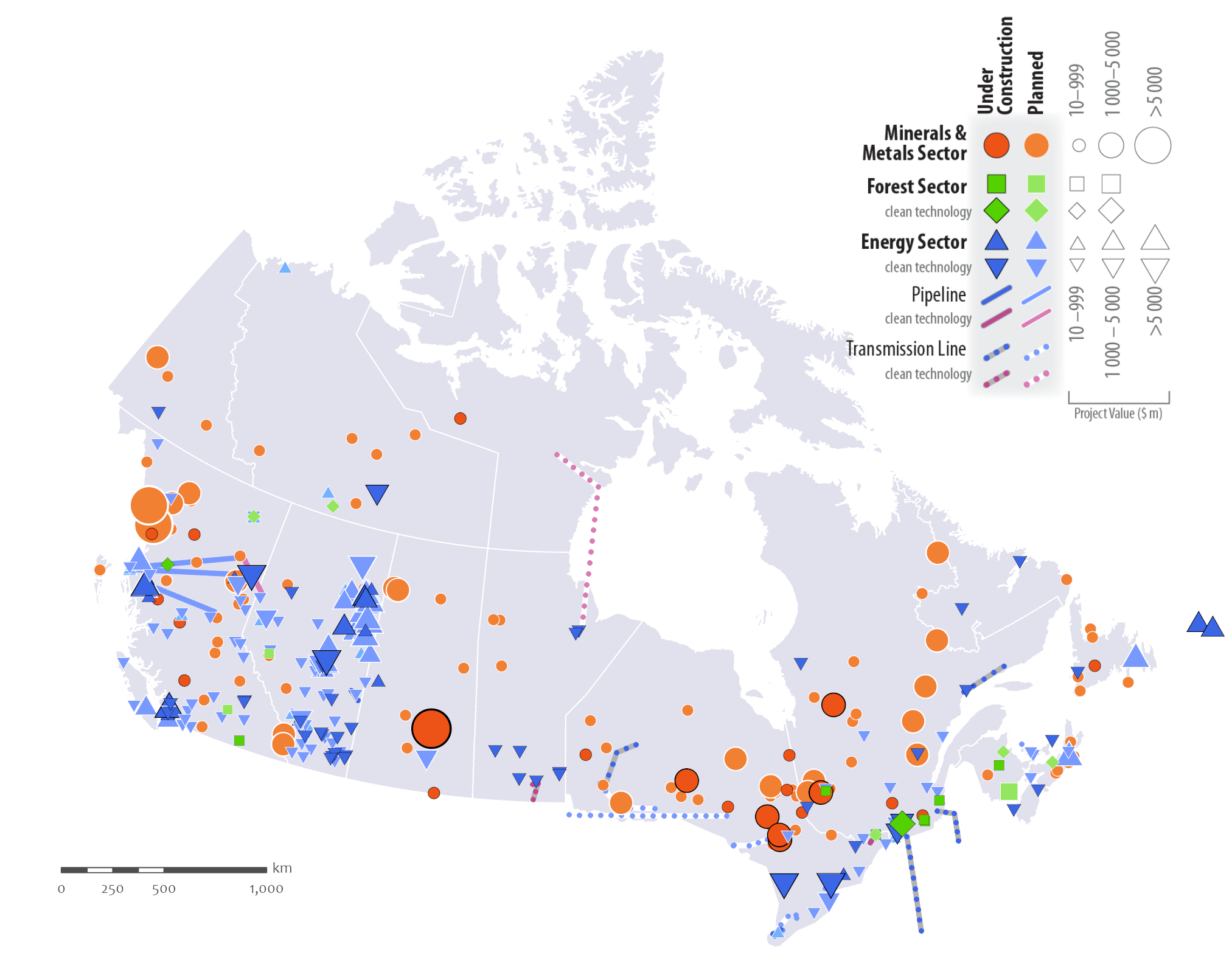

National Profile

The capital threshold value of $50 million is used for energy and mining sector projects. Electricity and forest sector projects are valued at $20 million or greater. A capital threshold of $10 million is set for clean energy and clean technology projects, which fall within the energy and forest sectors.

Potential major natural resource projects in all sectors are spread across the country. There is a high concentration of energy projects in Alberta and British Columbia reflecting the presence of oil and gas. The bulk of minerals and metals projects are in Ontario and Quebec. There is at least one energy project and one mining project in each province and territory. Forest projects are largely found in British Columbia, Quebec, and New Brunswick. Looking across sectors, the projects with the highest cost tend to be in the energy sector. A more detailed description by province or territory can be found in the Provincial and Territorial Profiles.

Disclaimer: This map is for illustrative purposes and has neither been prepared for, nor would be suitable for, legal, engineering, or surveying purposes.

Canada Centre for Mapping and Earth Observation, Natural Resources Canada, 2024.

- As of September 2024, there are 504 projects currently under construction or planned over the next ten years, representing $632.6B in potential capital investment.

- Energy projects accounted for more than 80% of the total value of major projects in the inventory, mining projects accounted for 18.5%, and forest projects for less than 1%.

Table A1: Sectoral Changes from 2023 to 2024

| Energy | Mining | Forest | Total | |

|---|---|---|---|---|

| 2023 Inventory totals | 343 ($472.3B) |

129 ($93.6B) |

21 ($4.6B) |

493 ($570.5B) |

| Potential capital revisions [Revised total] | + $8.2B [$480.5B] |

+ $3.4B [$97.0B] |

+ $0.4B [$5.0B] |

+ $12.1B [$582.6B] |

| Of which: Clean technology | 224 ($154.4B) |

N/A | 9 ($3.1B) |

233 ($157.4B) |

| Potential capital revisions [Revised total] | - $2.6B [$151.8B] |

N/A | + $83M [$3.2B] |

- $2.5B [$154.9B] |

| Add: | ||||

| New projects | 112 ($136.9B) |

38 ($37.2B) |

13 ($2.8B) |

163 ($176.9B) |

| Of which: Clean technology | 62 ($66.4B) | N/A | 5 ($0.7B) | 67 ($67.1B) |

| Subtract: | ||||

| Completed projects | 47 ($72.4B) | 4 ($3.3B) | 3 ($0.3B) | 54 ($76.0B) |

| Of which: Clean technology | 27 ($9.5B) | N/A | 1 ($40M) | 28 ($9.5B) |

| On hold, suspended; cancelled, or removed | 68 ($35.0B) | 25 ($13.8B) | 5 ($2.0B) | 98 ($50.8B) |

| Of which: Clean technology | 54 ($16.6B) | N/A | 3 ($1.8B) | 57 ($18.3B) |

| 2024 Inventory totals | 340 ($510.0B) |

138 ($117.1B) |

26 ($5.5B) |

504 ($632.6B) |

| Of which: Clean technology | 205 ($192.1B) |

N/A | 10 ($2.0B) |

215 ($194.2B) |

Note: Table A1 summarizes the annual changes in the inventory from 2023 to 2024. The second row highlights revisions to potential investment since the previous update to account for more recent project financials. Next, new projects are added to the existing tally and completed projects are subtracted. This is followed by subtracting inactive projects to arrive at 2024 totals. Clean technology projects are shown at each step, where applicable.

Table A2: Inventory Summary by Detailed Project Status, 2024

| Energy | Mining | Forest | Total | |

|---|---|---|---|---|

| 2024 Inventory Total | 340 ($510.0B) | 138 ($117.1B) | 26 ($5.5B) | 504 ($632.6B) |

| Announced and Planning | 142 ($239.8B) | 31 ($23.1B) | 12 ($1.5B) | 185 ($264.4B) |

| In Review | 54 ($57.1B) | 46 ($29.5B) | 5 ($1.8B) | 105 ($88.4B) |

| Post-Review Planning | 0 | 0 | 0 | 0 |

| Approved | 35 ($54.1B) | 35 ($33.6B) | 0 | 70 ($87.7B) |

| Under Construction | 109 ($159.0B) | 26 ($30.9B) | 9 ($2.2B) | 144 ($192.1B) |

Table A3: Inventory Summary by Province and Territory, 2024

| Energy | Mining | Forest | Total | |

|---|---|---|---|---|

| 2024 Inventory Total | 340 ($510.0B) |

138 ($117.1B) |

26 ($5.5B) |

504 ($632.6B) |

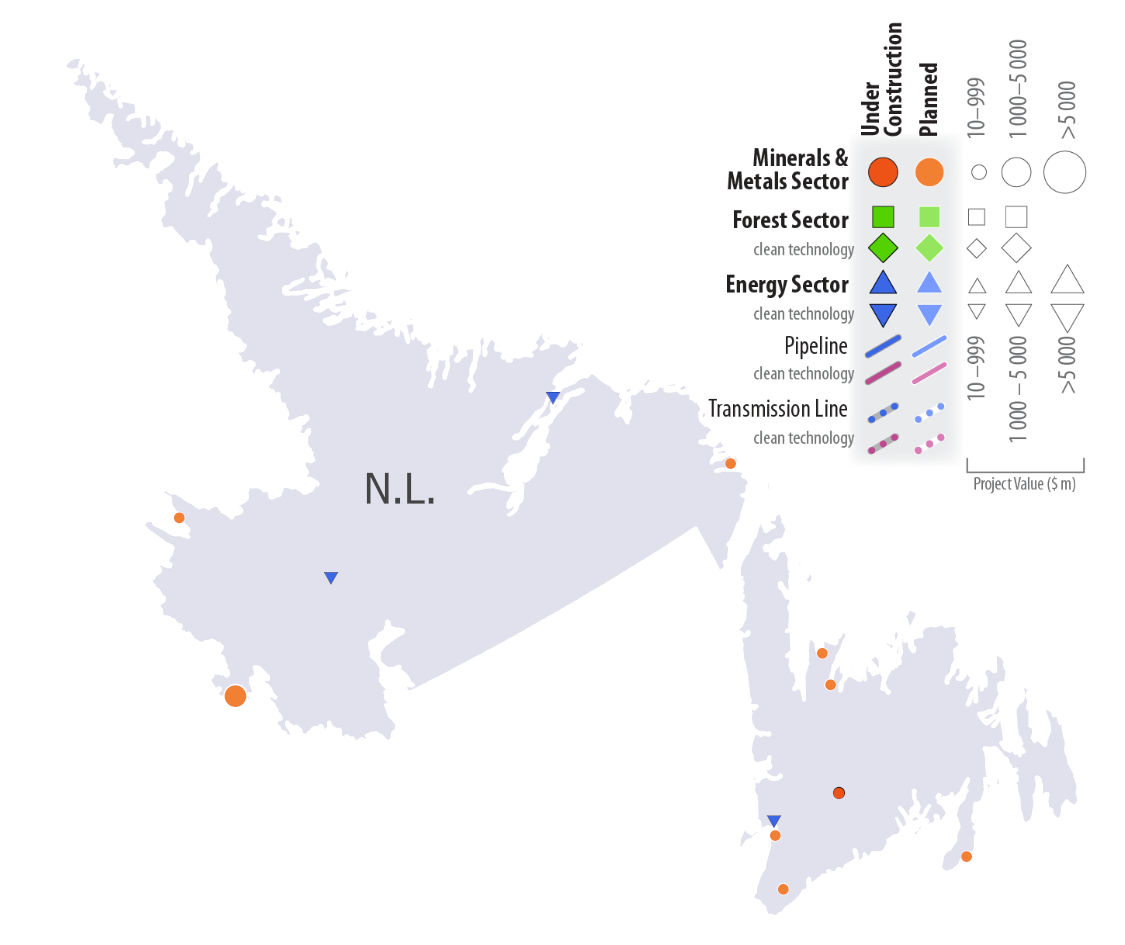

| Newfoundland and Labrador | 7 ($16.5B) | 9 ($6.1B) | 0 | 16 ($22.6B) |

| Prince Edward Island | 4 ($0.2B) | 0 | 0 | 4 ($0.2B) |

| Nova Scotia | 8 ($8.7B) | 5 ($0.8B) | 3 ($0.6B) | 16 ($10.1B) |

| New Brunswick | 2 ($0.3B) | 1 ($0.6B) | 3 ($1.2B) | 6 ($2.0B) |

| Quebec | 59 ($38.2B) | 31 ($23.6B) | 9 ($2.3B) | 99 ($64.1B) |

| Ontario | 32 ($69.4B) | 26 ($20.3B) | 0 | 58 ($89.7B) |

| Manitoba | 15 ($1.1B) | 4 ($0.6B) | 0 | 19 ($1.7B) |

| Saskatchewan | 12 ($6.2B) | 11 ($20.1B) | 1 ($0.4B) | 24 ($26.7B) |

| Alberta | 105 ($145.5B) | 4 ($2.3B) | 2 ($0.6B) | 111 ($148.3B) |

| British Columbia | 88 ($218.8B) | 37 ($35.5B) | 7 ($0.3B) | 132 ($254.6B) |

| Yukon | 1 ($0.04B) | 4 ($4.6B) | 0 | 5 ($4.7B) |

| Northwest Territories | 4 ($1.5B) | 5 ($2.0B) | 1 ($0.02B) | 10 ($3.5B) |

| Nunavut | 0 | 1 ($0.6B) | 0 | 1 ($0.6B) |

| Multi-jurisdictional | 3 ($3.7B) | 0 | 0 | 3 ($3.7B) |

Provincial and Territorial Profiles

Individual Provincial and Territorial profiles include annual highlights and maps showing project locations.

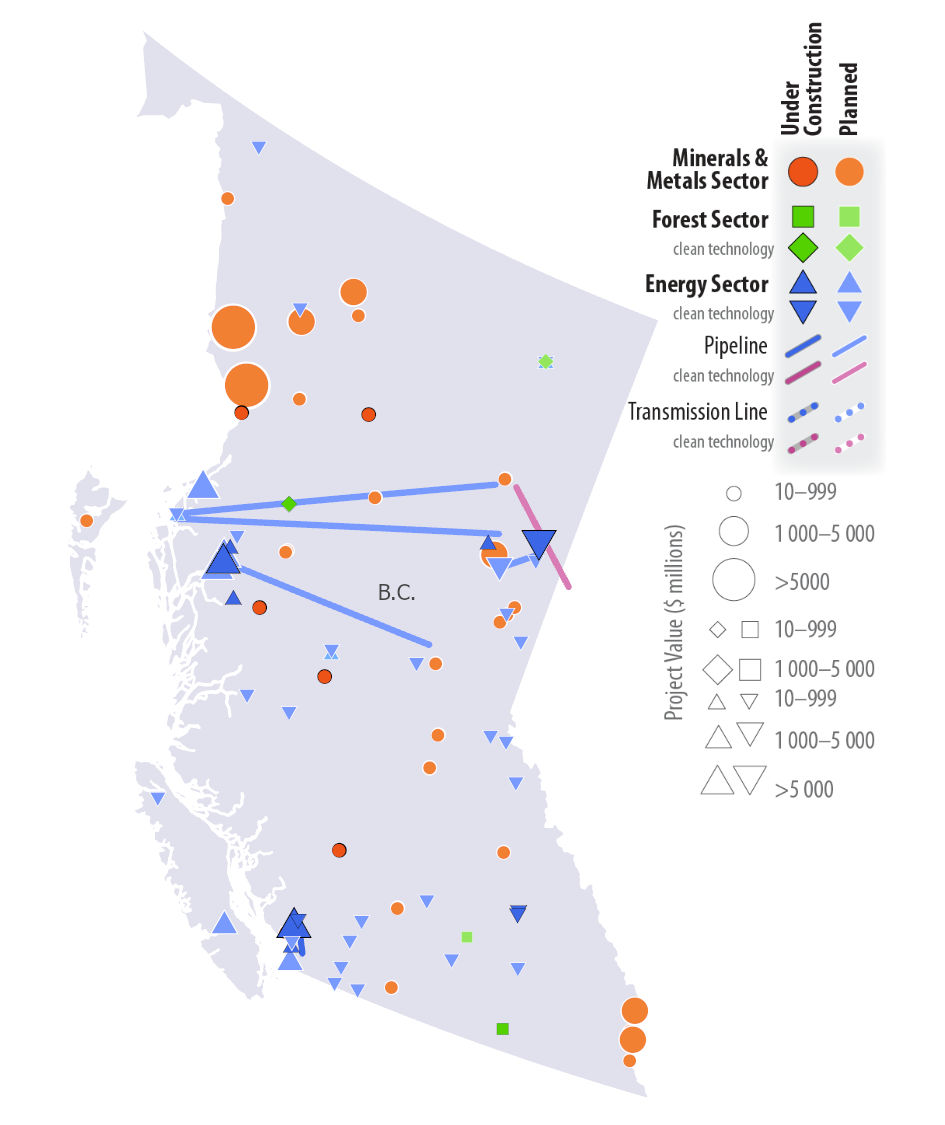

British Columbia

- In 2024, a total of 132 projects are under construction or planned over the next ten years in British Columbia, representing $254.6B and 40.3% of total national-level investment in the inventory.

- Energy projects are valued at $218.8B and account for 85.9% of the value of potential investments in the province.

- The largest projects include LNG Canada Phase 1 ($47.9B) and Phase 2 ($25.0B), Kitimat Clean Oil Refinery ($22.0B), the Peace River Site C Hydroelectric Project ($16.0B), and the Ksi Lisims LNG project in the Nasoga Gulf ($10.0B).

- In 2024, 54 of the 132 projects in British Columbia were clean technology projects valued at $40.5B.

- In 2023, the total number of active projects in British Columbia was 125 ($212.0B). In summary, between the 2023 and 2024 inventory updates:

- 34 new projects (20 energy, 13 mining, 1 forest) were added

- 5 projects were completed (4 energy, 1 mining) and therefore removed from the inventory

- 22 projects (17 energy, 5 mining) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

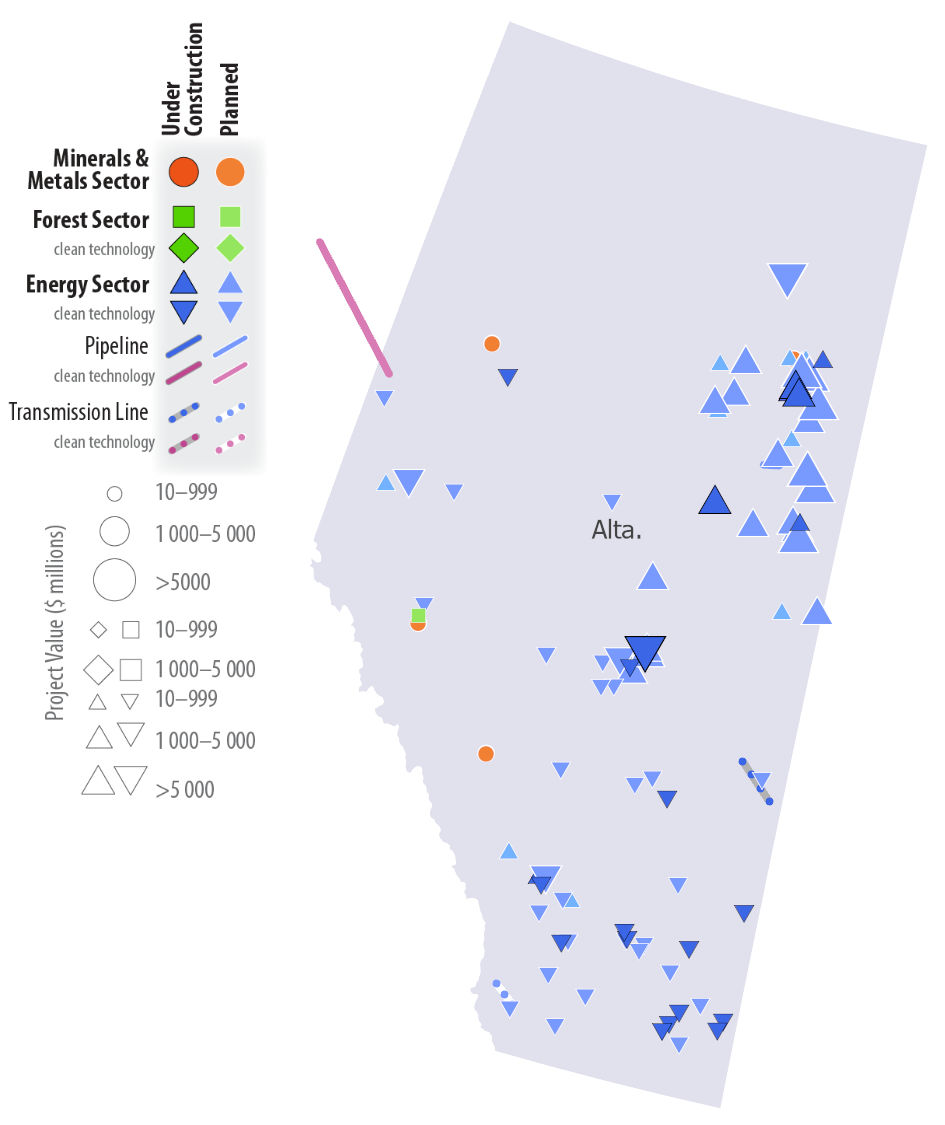

Alberta

- In 2024, a total of 111 projects are under construction or planned over the next ten years in Alberta, representing $148.3B and 23.5% of total national-level investment in the inventory.

- Energy projects are valued at $145.5B and account for 98.0% of the value of potential investments in the province.

- The largest projects include the Pathways Alliance Carbon Capture Storage Hub Phase 1 ($16.5B), Athabasca Oil Sands Project at Jackpine ($12.0B), and Dow Chemical’s Net-Zero Polyethylene Facility ($11.5B).

- In 2024, 56 of the 111 projects in Alberta were clean technology projects valued at $50.3B.

- In 2023, the total number of active projects in Alberta was 118 ($160.3B). In summary, between the 2023 and 2024 inventory updates:

- 29 new projects were added (27 energy, 2 forest)

- 22 energy projects were completed and therefore removed from the inventory

- 14 energy projects became inactive (on hold, suspended, cancelled or removed) and were therefore removed

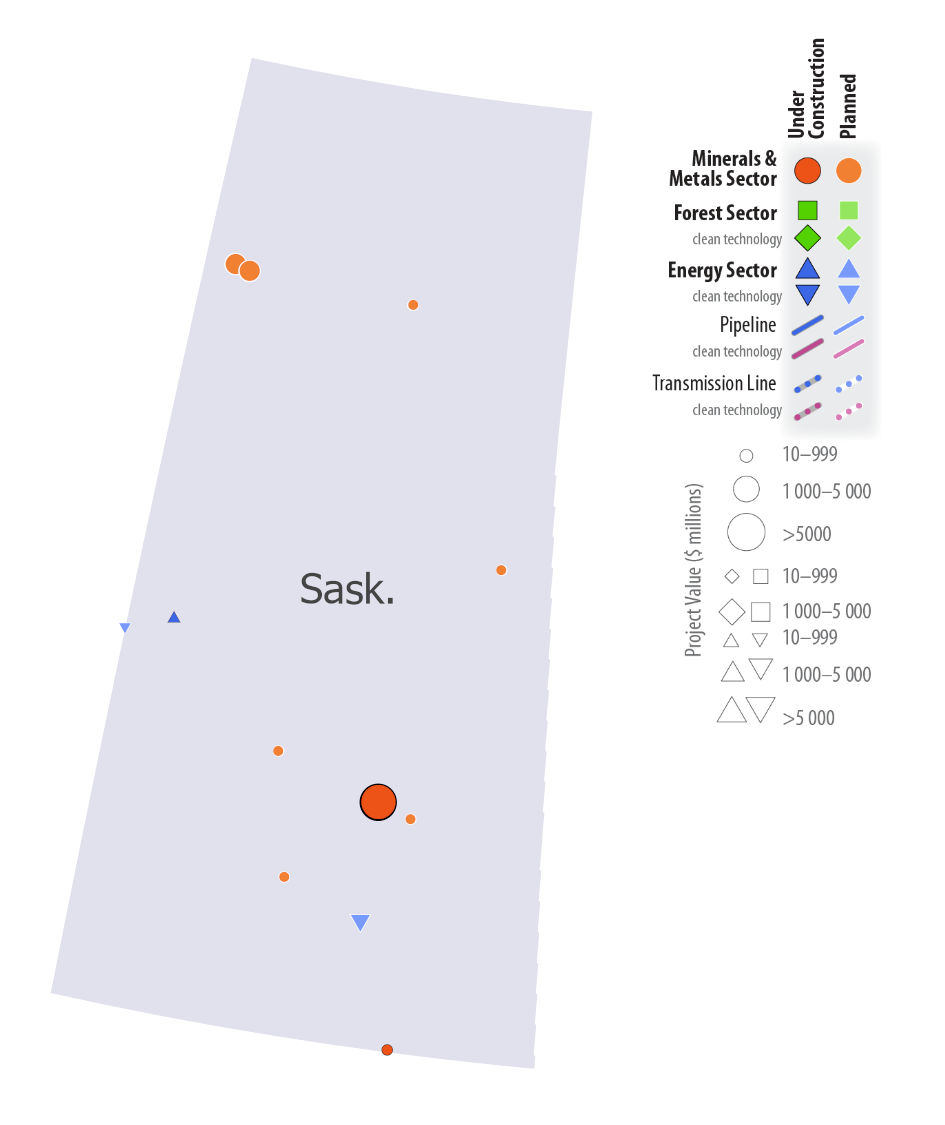

Saskatchewan

- In 2024, a total of 24 projects are under construction or planned over the next ten years in Saskatchewan, representing $26.7B and 4.2% of potential investment in the inventory.

- Mining projects are valued at $20.1B and account for 75.2% of the value of potential investments in the province.

- The largest projects include the Jansen Potash Project Stage 1 ($7.5B) and Stage 2 ($6.4B), FCL Renewable Diesel Plant ($2.0B), NexGen Energy Rook I uranium project ($1.3B), and Aspen Power Station ($1.3B).

- In 2024, 6 of the 24 projects in Saskatchewan were clean technology projects valued at $3.5B.

- In 2023, the total number of active projects in Saskatchewan was 24 ($20.0B). In summary, between the 2023 and 2024 inventory updates:

- 7 new projects (3 energy, 4 mining) were added

- 4 projects (3 energy, 1 forest) were completed and therefore removed from the inventory

- 3 projects (1 energy, 1 mining, 1 forest) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

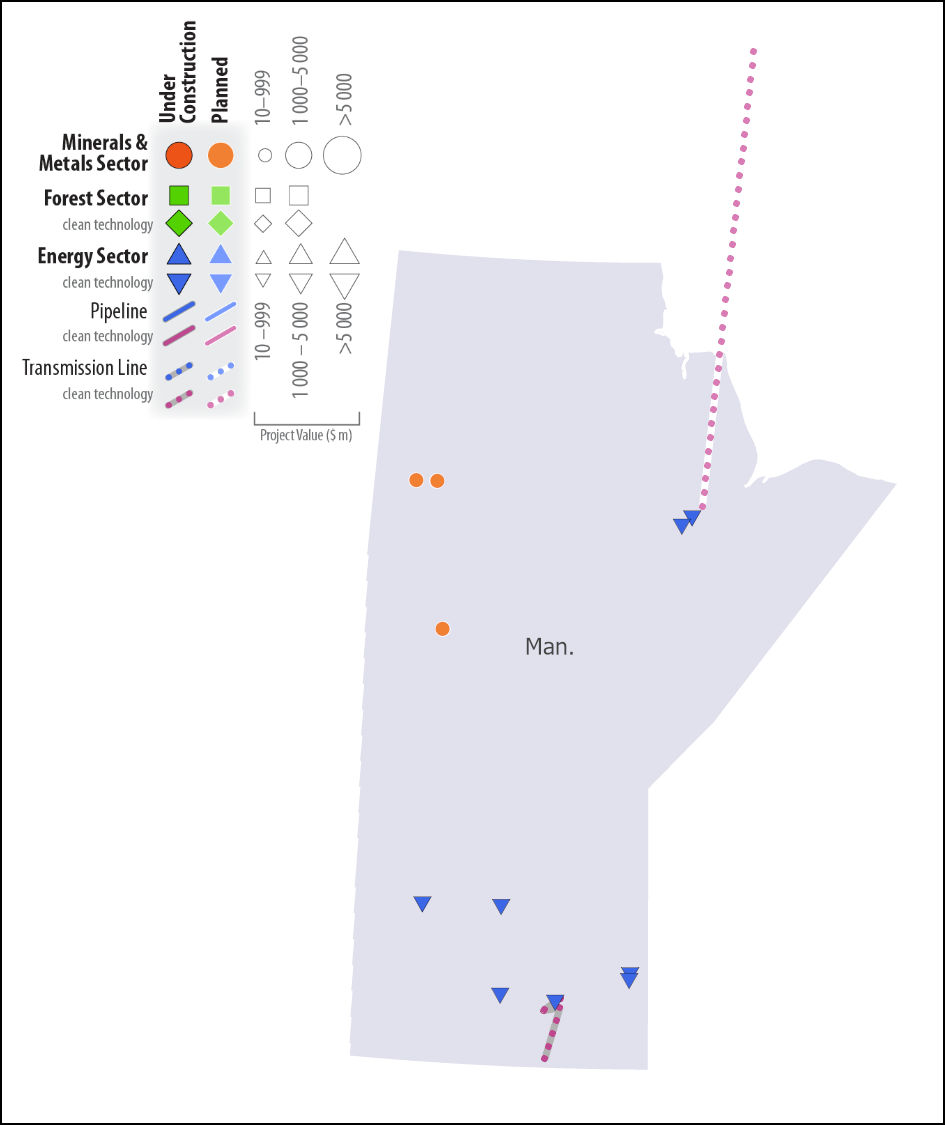

Manitoba

- In 2024, a total of 19 projects are under construction or planned over the next ten years in Manitoba, representing $1.7B of investment.

- Energy projects are valued at $1.1B and account for 62.4% of the value of potential investments in the province. The remainder consists of mining projects.

- The largest projects include Lynn Lake Mine ($0.3B) and Pointe du Bois Renewable Energy Project ($0.4B).

- In 2024, 15 of the 19 projects in Manitoba were clean technology projects valued at $1.1B.

- In 2023, the total number of active projects in Manitoba was 30 ($2.1B). In summary, between the 2023 and 2024 inventory updates:

- 5 new projects (4 energy, 1 mining) were added

- 2 energy projects were completed and therefore removed from the inventory

- 14 energy projects became inactive (on hold, suspended, cancelled or removed)

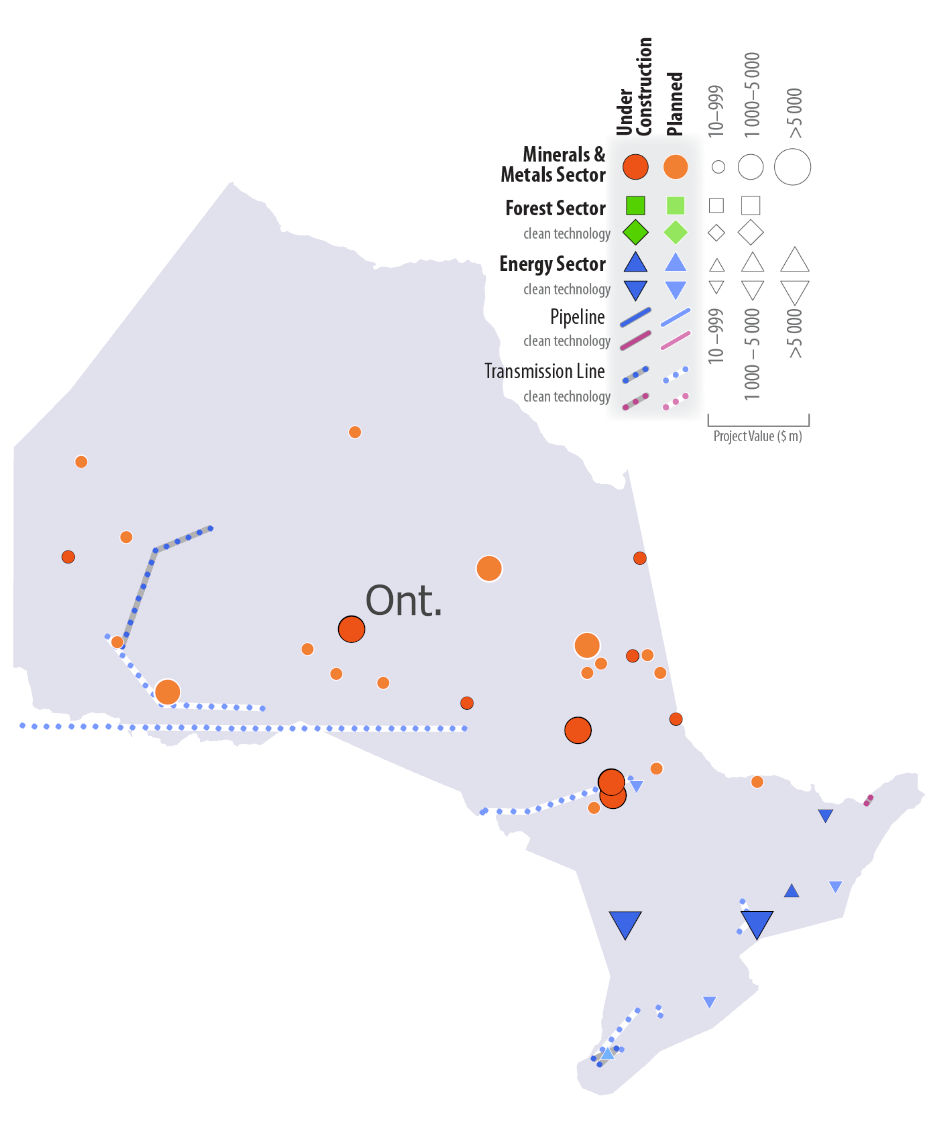

Ontario

- In 2024, a total of 58 projects are under construction or planned over the next ten years in Ontario, representing $89.7B and 14.2% of total investment in the inventory.

- Energy projects are valued at $69.4B and account for 77.4% of the value of potential investments in the province.

- Transmission project development in Ontario is undergoing a significant expansion and will continue to grow in the near future. As such, 8 new lines currently in progress or in the pipeline were added to the inventory, accounting for a total of approximately $4B in investment.

- The largest projects include the NWMO’s Adaptive Phased Management Deep Geological Repository ($26.0B), Bruce Nuclear Refurbishment ($13.0B), Darlington Nuclear Refurbishment ($12.8B), and the Meaford Pumped Storage Project ($4.3B).

- In 2024, 14 of the 58 projects in Ontario were clean technology projects valued at $60.7B.

- In 2023, the total number of active projects in Ontario was 52 ($52.2B). In summary, between the 2023 and 2024 inventory updates:

- 21 new projects (16 energy, 5 mining) were added

- 6 projects (3 energy, 3 mining) were completed and therefore removed from the inventory

- 9 projects (1 energy, 6 mining, 2 forest) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

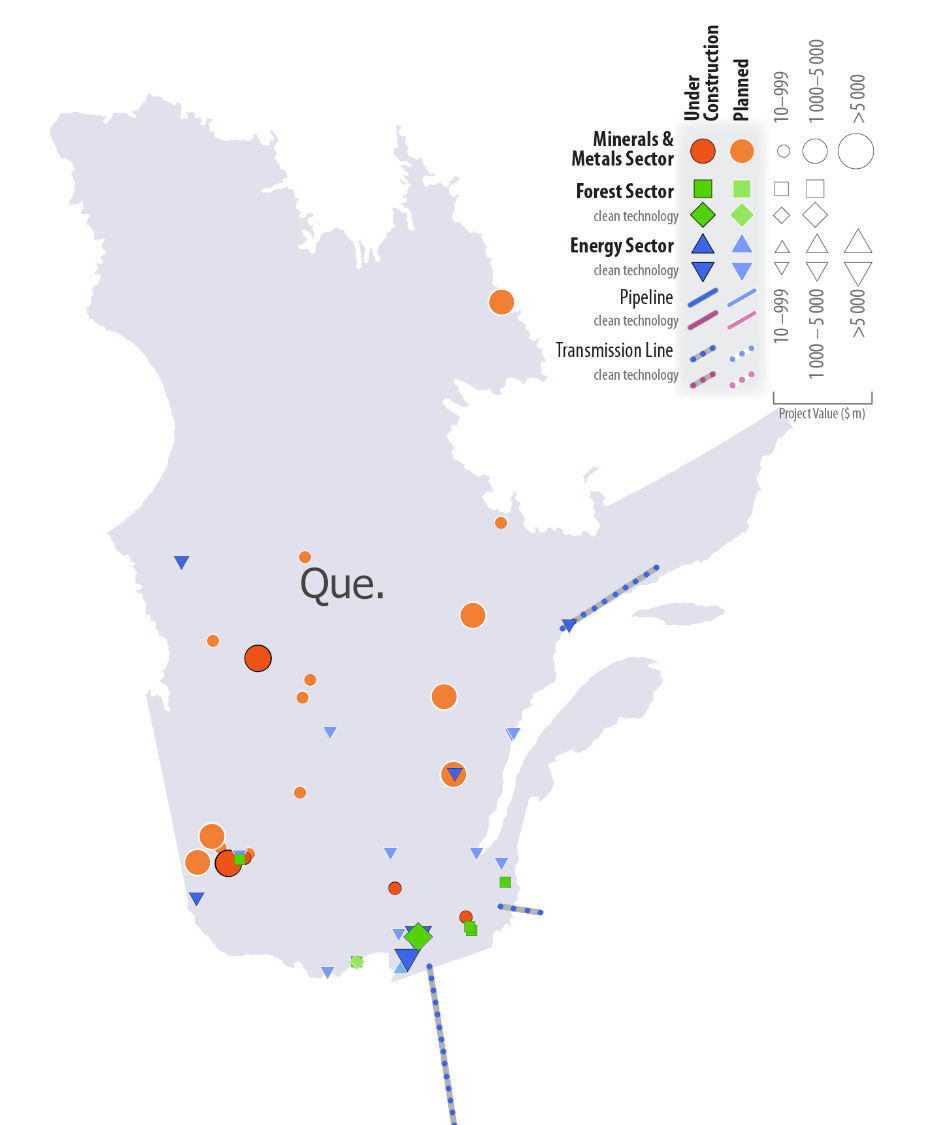

Quebec

- In 2024, a total of 99 projects are under construction or planned over the next ten years in Quebec, representing $64.1B and 10.1% of total investment in the inventory.

- Energy projects are valued at $38.2B and mining projects are valued at $23.6B, respectively accounting for 59.6% and 36.8% of the value of potential investments in the province.

- The largest projects include the Chamouchouane zone wind farm ($9.0B), TES Canada Green Hydrogen plant ($4.0B), Champlain Hudson Power Express Transmission Line ($2.2B), the Whabouchi Lithium Project ($2.1B), and the Odyssey mine extension project ($1.7B).

- In 2024, 45 of the 99 projects in Quebec were clean technology projects valued at $32.8B. Both the count and value of clean technology projects were up from 2023 (28 projects valued at $17.6B).

- In 2023, the total number of active projects in Quebec was 65 ($44.4B). In summary, between the 2023 and 2024 inventory updates:

- 52 new projects (35 energy, 11 mining, 6 forest) were added

- 7 projects (5 energy, 2 forest) were completed and therefore removed from the inventory

- 11 projects (10 mining, 1 forest) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

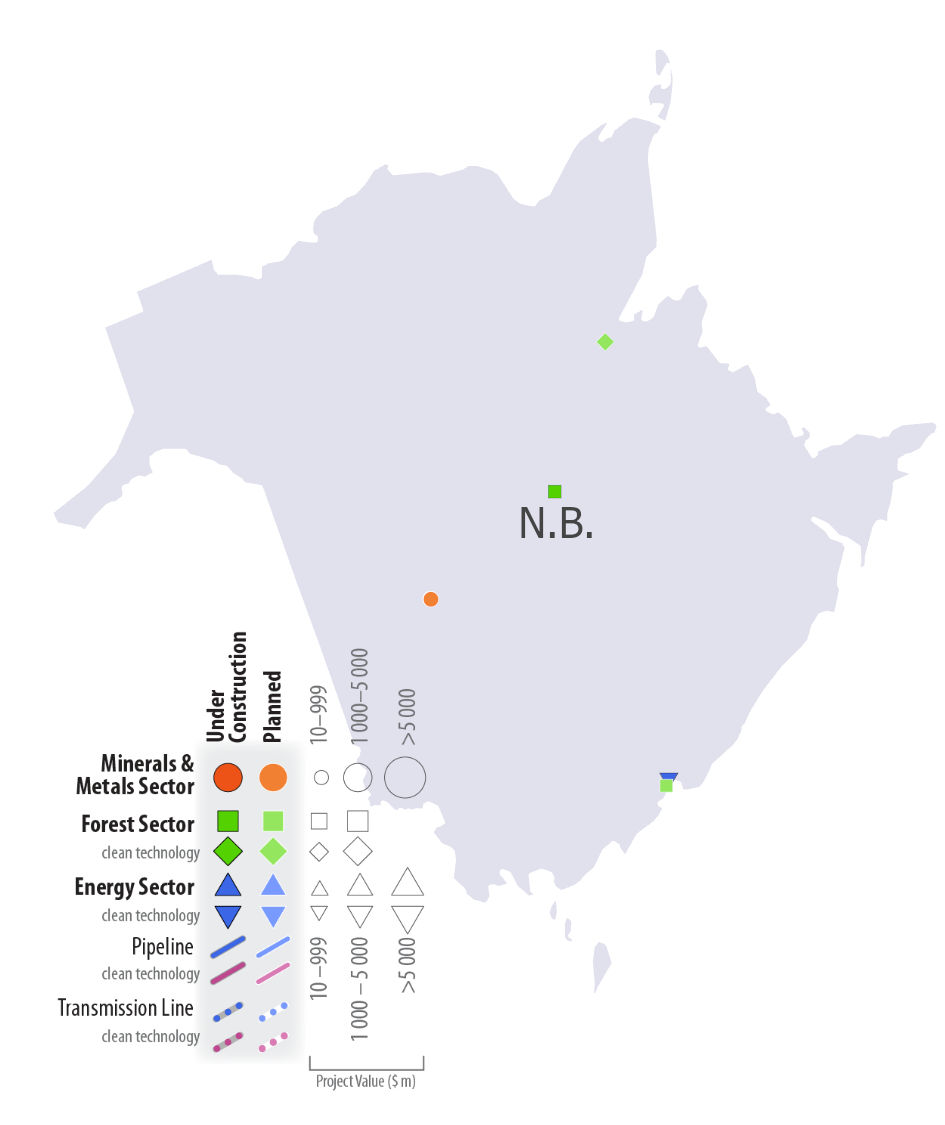

New Brunswick

- In 2024, a total of 6 projects are under construction or planned over the next ten years in New Brunswick, representing $2.0B and 0.3% of total investment in the inventory.

- Forest projects are valued at $1.2B and account for 59.1% of the value of potential investments in the province.

- The largest projects include the Saint John Pulp Mill Upgrades ($1.1B), Sisson Project ($0.6B), and a Smart Grids Investments Phase Project ($0.2B).

- In 2024, 3 of the 6 projects in New Brunswick were clean technology projects valued at $0.3B.

- In 2023, the total number of active New Brunswick projects was 7 ($4.3B). In summary, between the 2023 and 2024 inventory updates:

- 1 new forest project was added

- 1 energy project was completed and therefore removed from the inventory

- 1 energy project became inactive (on hold, suspended, cancelled or removed) and was therefore removed

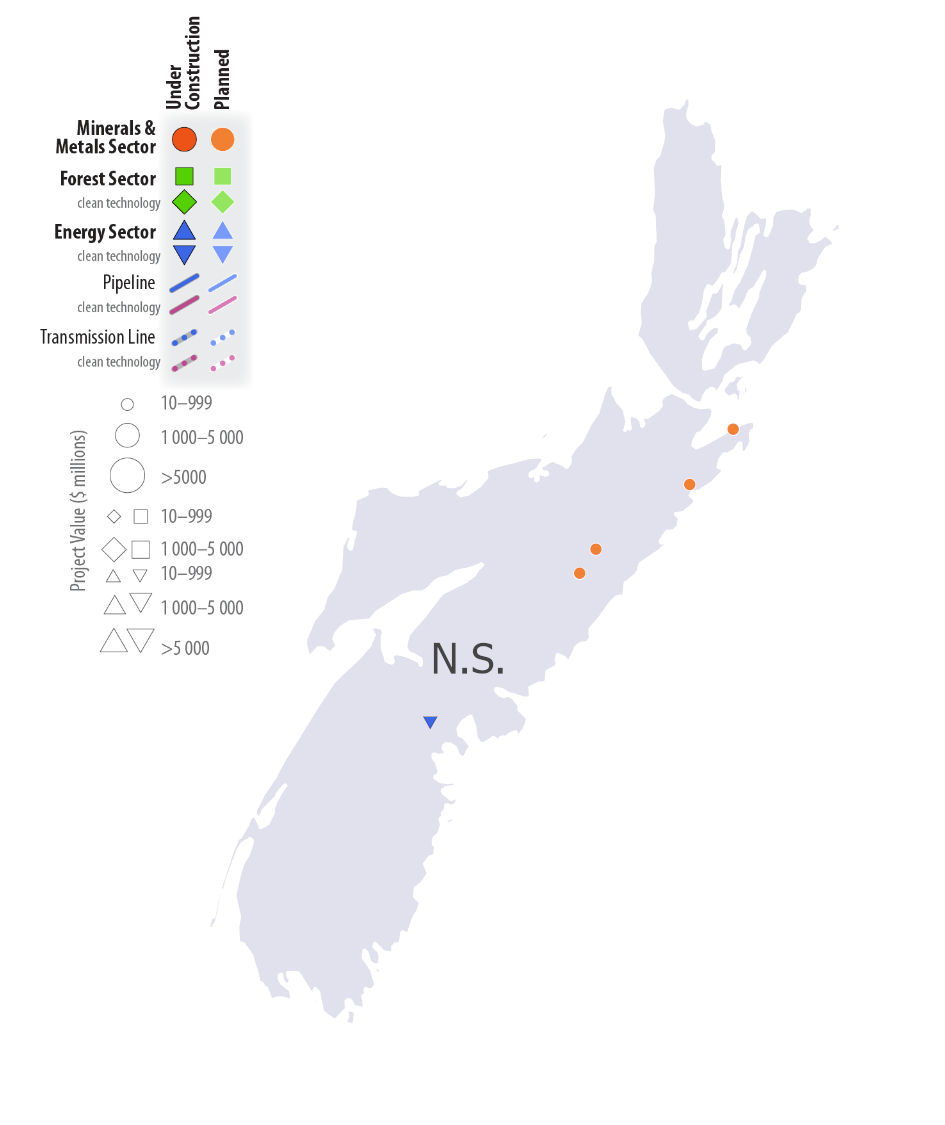

Nova Scotia

- In 2024, a total of 16 projects are under construction or planned over the next ten years in Nova Scotia, representing $10.1B and 1.6% of total investment in the inventory.

- Energy projects are valued at $8.7B and account for 86.4% of the value of potential investments in the province.

- The largest projects include Bear Head Energy ($8.0B), Nova Scotia Power Battery Storage ($0.4B), the Goldboro Gold Mine ($0.3B), and the Mass Timber Manufacturing Plant ($0.2B).

- In 2024, 9 of the 16 projects in Nova Scotia were clean technology projects valued at $1.1B.

- In 2023, the total number of active projects in Nova Scotia was 15 ($9.3B). In summary, between the 2023 and 2024 inventory updates:

- 5 new projects (1 energy, 1 mining, 3 forest) were added

- 4 projects (3 energy, 1 mining) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

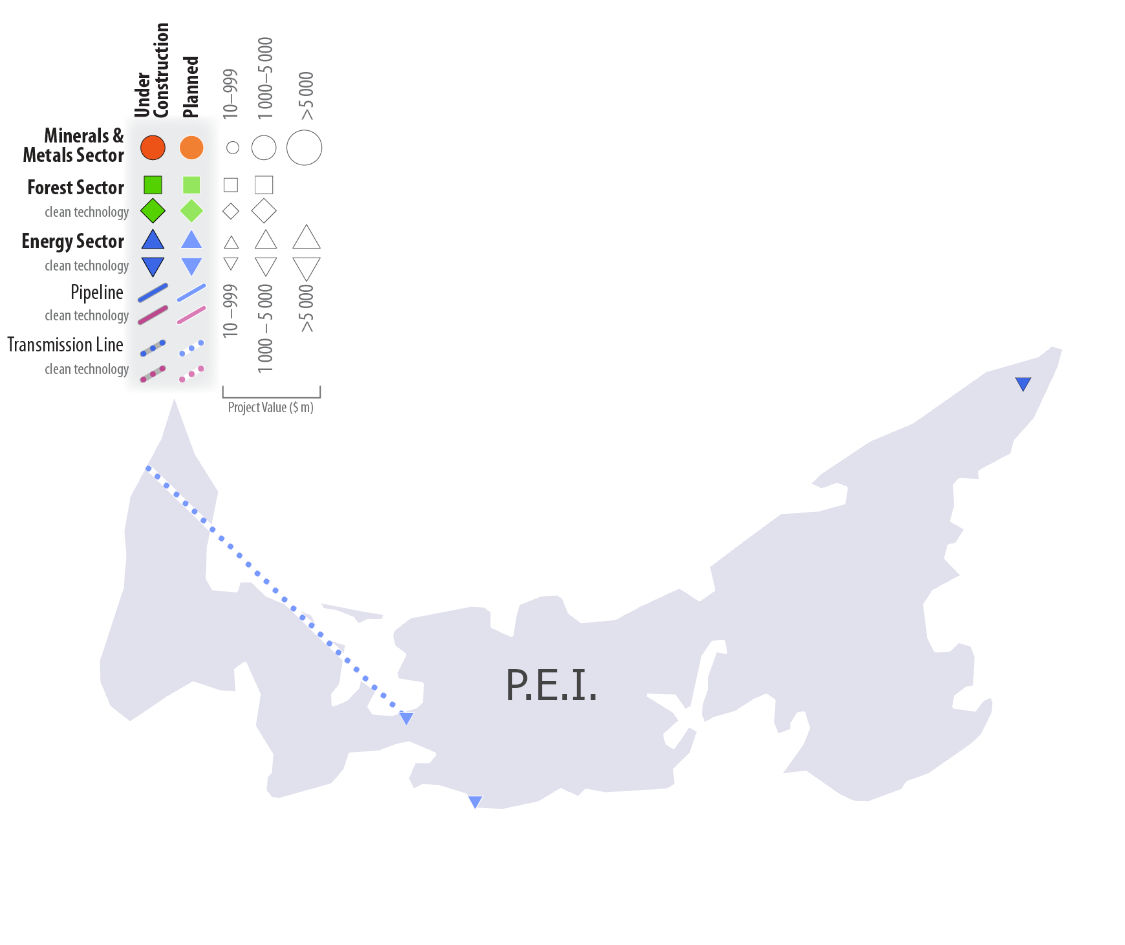

Prince Edward Island

- In 2024, a total of 4 projects are under construction or planned over the next ten years in Prince Edward Island, representing $0.2B and 0.04% of total investment in the inventory.

- Energy projects accounted for the full value of potential investments in the province.

- Projects include the Skinners Pond Transmission Line ($0.09B), PEI Energy Corporation Wind Farm #5 ($0.06B), and the Western PEI Transmission Upgrade ($0.04B).

- In 2024, 3 of the 4 projects in Prince Edward Island were clean technology projects valued at $0.2B.

- In 2023, the total number of active projects in Prince Edward Island was 7 ($0.5B). In summary, between the 2023 and 2024 inventory updates:

- 2 energy projects were completed and therefore removed from the inventory

- 1 energy project became inactive (on hold, suspended, cancelled or removed) and was therefore removed

Newfoundland and Labrador

- In 2024, a total of 16 projects are under construction or planned over the next ten years in Newfoundland and Labrador, representing $22.7B and 3.6% of total investment in the inventory.

- Energy projects are valued at $16.5B and account for 73.1% of the value of potential investments in the province.

- The largest projects include Grassy Point LNG ($10.0B), Kamistiatusset iron ore mine ($3.9B), and the West White Rose oil expansion project ($3.8B).

- In 2024, 4 of the 16 projects in Newfoundland and Labrador were clean technology projects valued at $0.4B.

- In 2023, the total number of active projects in Newfoundland and Labrador was 28 ($24.7B). In summary, between the 2023 and 2024 inventory updates:

- 8 new projects (5 energy, 3 mining) were added

- 2 energy projects were completed and therefore removed from the inventory

- 18 projects (16 energy, 1 forest, 1 mining) became inactive (on hold, suspended, cancelled or removed) and were therefore removed

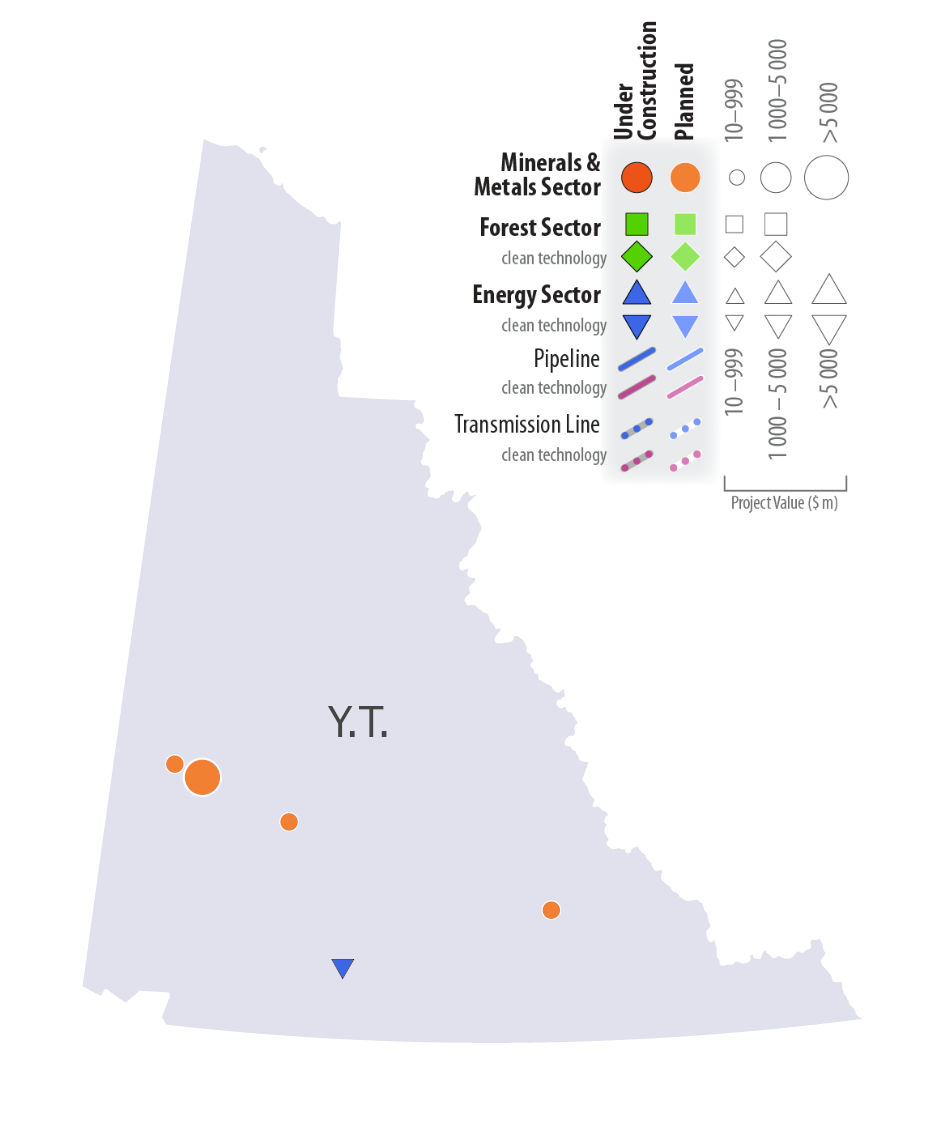

Yukon

- In 2024, a total of 5 projects are under construction or planned over the next ten years in Yukon, representing $4.7B and 0.7% of total investment in the inventory.

- Mining projects are valued at $4.6B and account for 99.3% of the value of potential investments in the territory.

- The largest projects include the Casino Mine ($3.6B), Kudz Ze Kayah Mine ($0.5B), and the Coffee Gold Mine ($0.3B).

- In 2024, 1 of the 5 projects in Yukon were clean technology projects valued at $0.04B.

- In 2023, the total number of active projects in Yukon was 7 ($4.4B). In summary, between the 2023 and 2024 inventory updates:

- No new projects were added

- 1 energy project was completed and therefore removed from the inventory

- 1 mining project became inactive (on hold, suspended, cancelled or removed) and was therefore removed

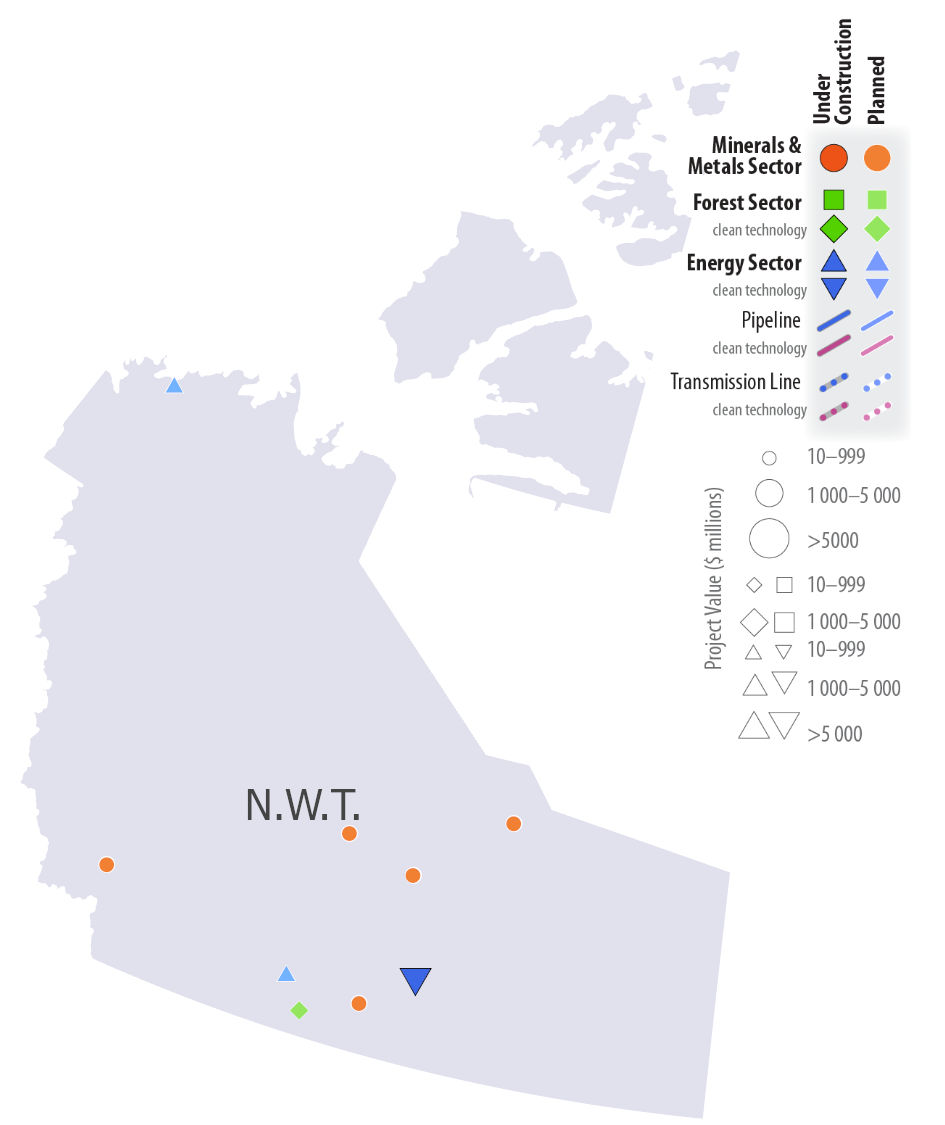

Northwest Territories

- In 2024, a total of 10 projects are under construction or planned over the next ten years in the Northwest Territories, representing $3.5B and 0.6% of total investment in the inventory.

- Energy projects are valued at $1.5B and mining projects at $2.0B, accounting respectively for 41.5% and 57.9% of the value of potential investments in the territory.

- The largest projects include the Taltson Hydroelectric Expansion Project ($1.2B), the Pine Point Mine ($0.7B), and the NICO Cobalt-Gold-Bismuth Mine ($0.6B).

- In 2024, 3 of the 10 projects in the Northwest Territories were clean technology projects valued at $1.3B.

- In 2023, the total number of active projects in Northwest Territories was 11 ($3.3B). In summary, between the 2023 and 2024 inventory updates:

- No new project was added

- 1 energy project was completed and therefore removed from the inventory

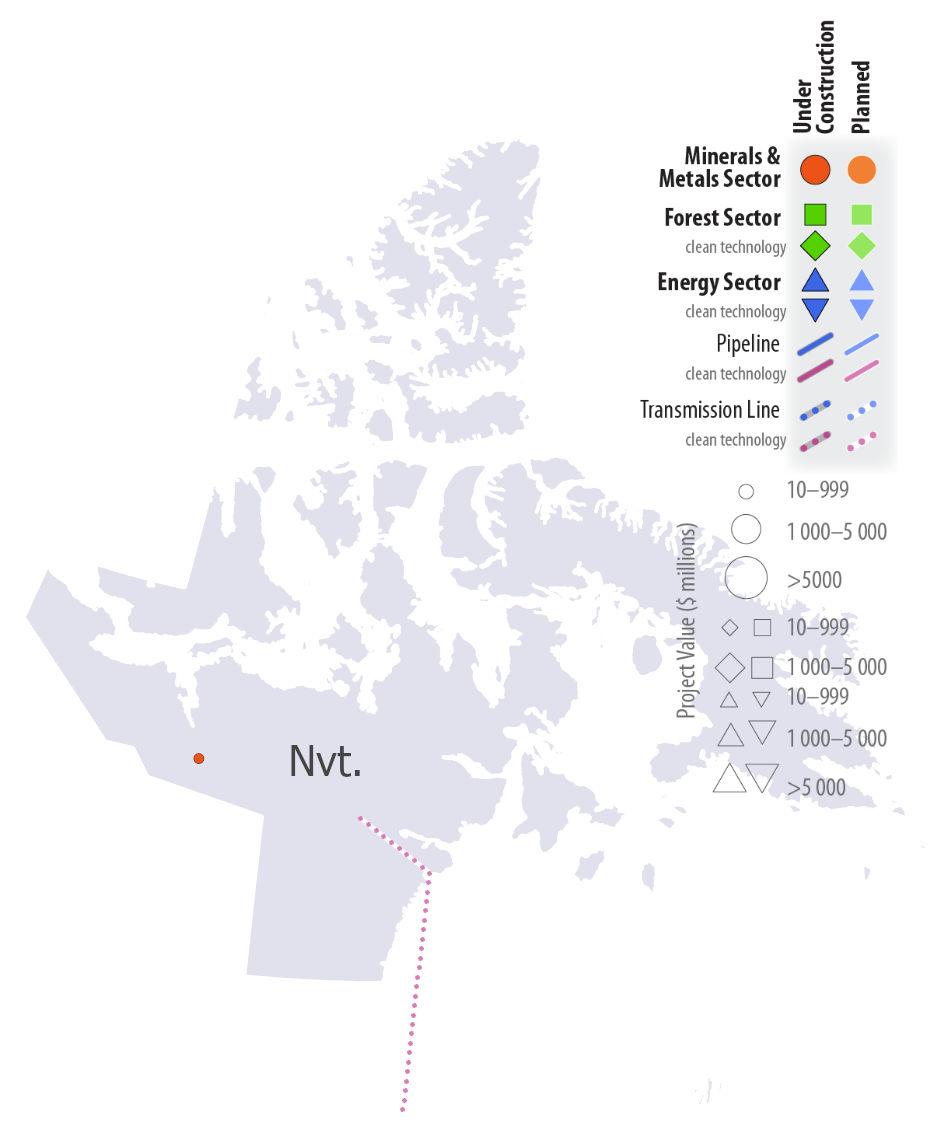

Nunavut

- In 2024, a total of 1 project, the Back River Gold Project, is under construction in Nunavut, representing $0.6B in investment in the mining sector.

- In 2023, the total number of active projects in Nunavut was also 1 ($0.6B). In summary, between the 2023 and 2024 inventory updates:

- No projects were added, completed or otherwise removed from the inventory