PRELIMINARY REPORT TO THE MINISTER OF NATURAL RESOURCES AND THE MINISTER OF INDUSTRY

FEBRUARY 28, 2014

A joint report by the

National Energy Board and Competition Bureau

TABLE OF CONTENTS

- 1. Executive Summary

- 2. Introduction

- 3. The Canadian Propane Industry

- 4. High Prices and Potentially Anticompetitive Behaviour

- 5. Current Situation

- 6. Causes of Recent Propane Shortages and Price Increases

- 7. Next Steps

1. Executive Summary

1.1 On February 4, 2014, the Ministers of Natural Resources and Industry requested that the National Energy Board and Competition Bureau work together to review propane market issues. This preliminary report responds to that request by providing an overview of the Canadian propane industry, current propane supplies, and initial perspectives on the factors that may have contributed to price increases and supply challenges this winter. This analysis remains preliminary and will continue over the next two months.

1.2 In Canada, propane is produced, transported, and distributed across a wide-reaching supply chain. Upstream producers manufacture propane through natural gas processing and as a by-product of crude oil refining. Propane is then either stored in underground salt caverns or transported by pipeline, rail, or truck across Canada by midstream firms. Finally, downstream distributors move propane to consumers, who purchase it for business and personal use. Propane supplies are also imported from and exported to the U.S.

1.3 This winter, propane inventories have been lower than average and demand has been unexpectedly high in the Canadian and U.S. propane industries. Supply tightened and prices increased rapidly. A wide range of data sources and industry stakeholders identifies various contributing factors:

- a colder-than-normal winter across the eastern parts of Canada and the U.S. that has resulted in greatly increased demand for home heating fuels and also caused challenges with certain transportation infrastructure;

- an exceptionally large and wet corn harvest in the U.S. Midwest, resulting in greater-than-normal demand for propane to dry the corn prior to storage;

- lower-than-normal propane inventories stored in advance of this year’s peak demand season, resulting in less propane being available for distribution; and

- rapidly growing U.S. exports of propane to overseas markets, which have decreased the availability of propane in Canada and the U.S.

1.4 Given current production, storage, transportation, and export trends, tight supply and high prices are expected to continue for the remainder of the high-demand winter season. Consumers of propane, including households that cannot easily switch to other fuels, will continue to be significantly impacted.

1.5 The National Energy Board and Competition Bureau will continue to work together on developing a better understanding of the dynamics of the Canadian propane industry, including market structure and marketplace behaviour. As requested by the Ministers, a more detailed final report on the overall propane market situation will be published publicly before April 30, 2014.

2. Introduction

2.1 The National Energy Board (NEB) and Competition Bureau (Bureau) have been asked to work together to review propane market issues, including price increases, scarcity, and the volume of propane exports to the U.S. More specifically, in a letter dated February 4, 2014,Footnote 1 the Ministers of Natural Resources and Industry requested that the NEB and the Bureau examine:

- the propane supply and demand situation in Canada, including production, inventories, exports/imports and end-use;

- the propane distribution network;

- wholesale and retail propane pricing;

- composition of the wholesale and retail market;

- the factors that have contributed to the recent shortages and price spikes;

- whether there have been any anti-competitive activities that may have exacerbated the impact on consumers; and

- any potential factors that could exacerbate the current market challenges or contribute to future propane shortages and related price increases.

2.2 This preliminary report analyzes the above issues, with emphasis on the availability of current supplies and initial perspectives on the factors that may have led to recent propane shortages and price increases in Canada. As requested by the Ministers, a more detailed final report on the overall propane market situation will be published publicly before April 30, 2014.

2.3 As Canada’s energy regulator, the NEB has significant understanding of, and experience with, the Canadian propane industry.Footnote 2 The Bureau has substantial expertise in assessing the performance of various industries and examining the role that competitive forces play in market outcomes.Footnote 3 The two organizations are well equipped to undertake this review and have worked together closely on this preliminary report.

2.4 This report has also benefitted from the participation of a range of stakeholders from all parts of the propane supply chain. Fifty-two interviews have been conducted to date, including ten firms performing upstream and/or midstream activities, twenty-seven firms performing downstream activities, and fifteen industry associations, consumer groups, and other stakeholders. In addition, the report examined proprietary and publicly available information from across Canada and the U.S. to better understand propane market dynamics, the current supply situation, and the causes of recent shortages and price increases.

3. The Canadian Propane Industry

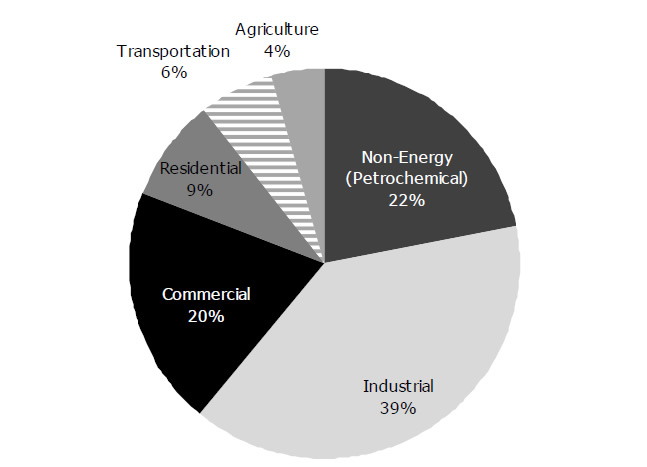

3.1 Propane is a natural gas liquidFootnote 4 that is relied on by Canadians for a variety of purposes, from home heating and cooking, to agricultural crop drying and fueling vehicles. In 2012, approximately 10.2 million cubic metres of propane were consumed in Canada.Footnote 5 Table 3.1 reports the most popular end uses of propane in Canada. Figure 3.1 shows the percentage of propane that was consumed by each sector during 2012.

| Sector | End Uses |

|---|---|

| Residential | Home heating, water heating, cooking |

| Commercial | Space heating, water heating, cooking |

| Industrial | Forklifts, heating for refining |

| Transportation | Automotive |

| Agriculture | Crop drying, barn and stable heating |

| Non-Energy | Plastics manufacturing |

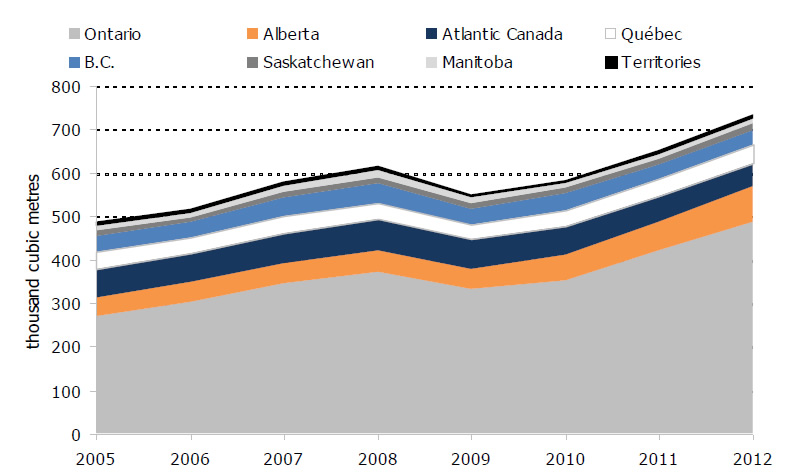

3.2 Propane is a common source of heating fuel for residences and businesses that are not served by natural gas pipelines. Statistics Canada estimates that approximately one per cent of households heat with propane, with the highest rate in Ontario at two per cent.Footnote 6 Figure 3.2 shows the geographic distribution of residential demand for propane, which is concentrated in Ontario.

Figure 3.1: Canadian Propane Demand by Sector, 2012

The source of this information is Statistics Canada, CANSIM 128-0012.

Text Version

Figure 3.1: Canadian Propane Demand by Sector, 2012

In 2012, propane in Canada was consumed in the following proportions:

Industrial uses - 39%,

Non-Energy (Petrochemical) uses - 22%,

Commercial uses - 20%,

Residential uses - 9%,

Transportation uses - 6%, and

Agricultural uses - 4%.

The source of this information is Statistics Canada, CANSIM 128-0012.

Figure 3.2: Residential Propane Demand by Canadian Province or Region, 2005-2012

The source of this information is Statistics Canada, CANSIM 128-0012.

Text Version

Figure 3.2: Residential Propane Demand by Canadian Province or Region, 2005-2012

In Ontario, residential propane usage has increased from approximately 270 thousand cubic metres per year in 2005 to approximately 486 thousand cubic metres per year in 2012. In Alberta, residential propane usage has increased from approximately 43 thousand cubic metres per year in 2005 to approximately 84 thousand cubic metres per year in 2012. In Atlantic Canada, residential propane usage has decreased from approximately 63 thousand cubic metres per year in 2005 to approximately 51 thousand cubic metres per year in 2012. In Québec, residential propane usage has fluctuated between 32 and 43 thousand cubic metres per year from 2005 to 2012. In British Columbia, residential propane usage has fluctuated between 32 and 47 thousand cubic metres per year from 2005 to 2012. In Saskatchewan, residential propane usage has increased from approximately 12.5 thousand cubic metres per year in 2005 to approximately 17.5 thousand cubic metres per year in 2012. In Manitoba, residential propane usage has fluctuated between 9 and 15 thousand cubic metres per year from 2005 to 2012. In the Territories, residential propane usage has fluctuated between 6 and 11 thousand cubic metres per year from 2005 to 2012.

The source of this information is Statistics Canada, CANSIM 128-0012.

3.3 Propane is produced through two means. Approximately 85 to 90 per cent of Canadian propane is produced as a result of natural gas processing, and the remaining 10 to 15 per cent is produced as a by-product of crude oil refining and upgrading. In 2012, approximately 11.1 million cubic metres of propane were produced in Canada.Footnote 7

3.4 Propane for resale is universally processed to an industry standard called “HD-5.”Footnote 8 Once propane has been processed to this standard, there is no meaningful chemical difference between the propane sold by one firm and another.

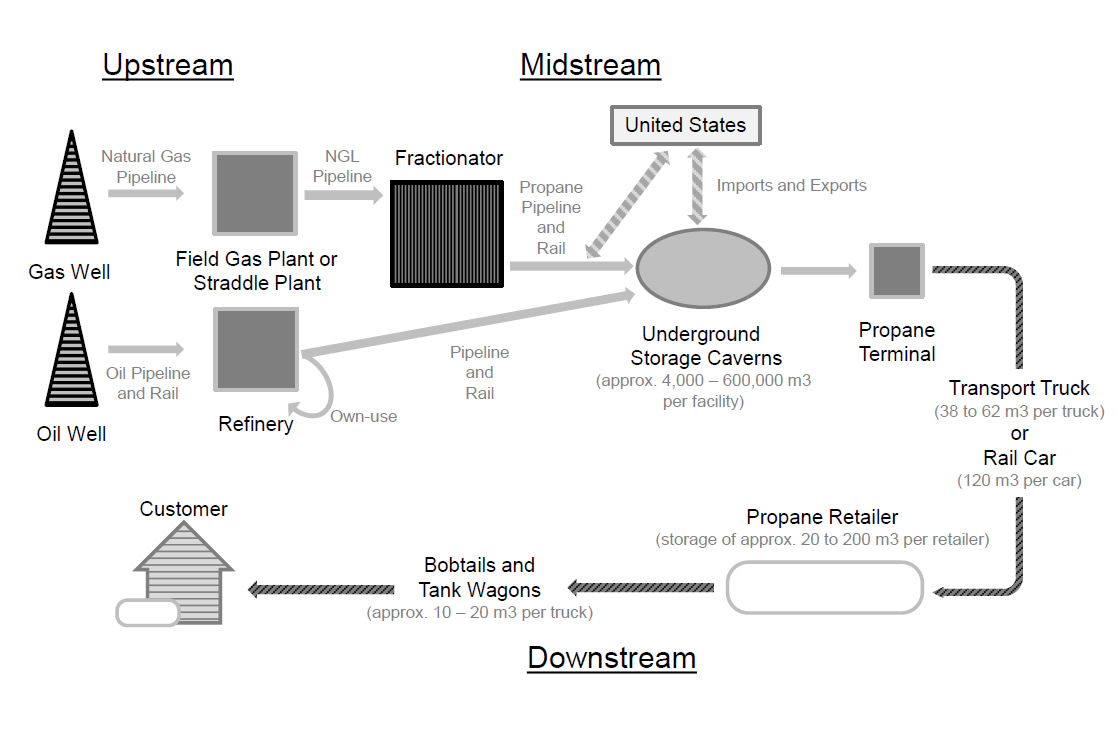

The Canadian Propane Supply Chain

3.5 Participants in the Canadian propane industry operate in a supply chain (see Figure 3.3) that can be separated into three categories:

- Upstream producers separate propane from natural gas through fractionationFootnote 9 and produce it as a by-product of crude oil refining;

- Midstream firms store large quantities of bulk propane in salt cavernsFootnote 10 and/or transport propane long distances via pipeline, rail, or truck from the areas where it is produced to where it is consumed; and

- Downstream distributors deliver propane to end users.

3.6 Initial observations indicate that each level in the supply chain is generally served by a separate group of firms, with no single entity responsible for every function of the supply chain. Although some firms may be present at more than one level, this appears to be the exception and not the norm.

Figure 3.3: Illustration of Canadian Propane Industry Supply Chain

Text Version

Figure 3.3: Illustration of Canadian Propane Industry Supply Chain

Propane is produced from natural gas and as a by-product of oil refining. Propane is extracted from natural gas wells as a stream of natural gas liquids. These natural gas liquids are transported by pipeline to a field gas plant or straddle plant, where they are then transported by a Natural Gas Liquids pipeline to a Fractionator. Once propane has been separated from a stream of natural gas liquids by the fractionator, it is transported by a propane pipeline or a rail line, either to underground storage caverns in Canada, or to the U.S. for export. Propane is extracted from oil wells are a constituent of unrefined oil. This unrefined oil is transported by oil pipelines and rail to a refinery, where the propane is separated from other petroleum products. Once it has been separated, propane is either used for that refinery’s own use, or is transported by pipeline or rail line to underground storage caverns in Canada. Propane can also be imported from the U.S. via propane pipeline and rail lines for storage in underground storage caverns. Underground storage caverns in Canada have capacities ranging from 4,000 to 600,000 cubic metres. Propane is extracted from these underground storage caverns via propane terminals, and shipped by transport truck or rail car to propane retailers. Transport trucks for propane have a capacity of between 38 and 62 cubic metres, and rail cars have a capacity of 120 cubic metres. At a propane retailer’s location, propane can be stored in large storage tanks with a capacity of between 20 and 200 cubic metres per retailer. Retailers then use bobtails and tank wagons, which have a capacity of between 10 and 20 cubic metres, to deliver propane to end customers. The activities involving extraction and processing of propane are typically referred to as “upstream” activities, whereas storage and transportation are considered “midstream”, and end delivery is “downstream”.

Upstream Production of Propane

3.7 Canadian propane production is centred in western Canada. As described above, approximately 85 to 90 per cent of Canadian propane is produced from natural gas processing. Of that amount, approximately 88 per cent is produced in Alberta due to the large amount of natural gas development there. British Columbia is the second largest gas plant producer of propane and is responsible for seven per cent of the Canadian total. Small volumes are also produced from gas plants in Saskatchewan and from offshore gas fields in Nova Scotia.Footnote 11 The 10 to 15 per cent of Canadian propane production that comes as a byproduct of crude oil refining and upgrading is distributed more evenly across Canada.

3.8 There are a number of upstream propane producers in Canada but the majority of Canadian fractionation capacity is owned and operated by a few firms. Other producers of propane include firms that own and operate oil refineries and bitumen upgraders.

3.9 An upstream firm has three options to dispose of propane once it has been produced:

- immediately sell the propane locally to downstream firms or third parties;

- move bulk quantities of propane along midstream transportation assets (i.e., pipeline, rail, or truck) to downstream firms located elsewhere; or

- store the propane for later use or sale.

3.10 Volumes produced by upstream firms are generally sold to large midstream or downstream customers. These sales are typically made according to annually-negotiated contracts that specify target volumes and pricing mechanisms.Footnote 12

3.11 When negotiating purchase contracts, upstream suppliers typically require that midstream and downstream customers buy at least one barrel during the low demand summer months for every three barrels that they require during the high demand winter season.Footnote 13

Midstream Storage and Transportation of Propane

3.12 Propane demand is highly seasonal, with peaks occurring in the fall and winter due to crop drying and heating fuel end use. Propane storage enables firms to amass inventories of propane over the course of the year in order to meet peak-season demand and to mitigate price volatility.

3.13 Bulk quantities of propane are stored in underground salt caverns. Major salt caverns in Canada are located in or around: Fort Saskatchewan, Alberta; Regina, Saskatchewan; and Sarnia, Ontario. Salt caverns are owned by upstream and midstream firms, and storage space in these caverns is generally leased as needed by downstream distributors to store their supplies until they can be picked up for further transport.

3.14 The two most common means for transporting propane across Canada from storage facilities or producers to end-users are pipeline and rail. Transporting long distances via truck is often uneconomical.Footnote 14

3.15 Pipelines offer the most economical long-distance transportation of propane. Two pipelines are currently used to supply eastern Canada. The first is the Enbridge system, which is used to transport a propane-plusFootnote 15 mix to a fractionation facility in southern Ontario. The Enbridge system is currently operating on an “apportioned”Footnote 16 basis. The second pipeline is Kinder Morgan’s Cochin pipeline, which has historically operated below capacity and will be reversed in 2014Footnote 17 to flow condensate east to west into Alberta.Footnote 18

3.16 Propane is also moved west to east across Canada on railways. In order for propane to be moved by rail, rail car filling and unloading infrastructure (commonly called “racks” or “terminals”) are constructed at both the origin and the destination. Facilities located at an originating production plant are generally owned by upstream firms, while facilities at the destination are generally owned by a downstream firm.

3.17 Rail transit of propane can encounter significant disruptions during winter months. Frozen signals can delay progress and cause congestion once the delay is alleviated. Cold weather can also cause train engine issues, and significant snowfalls can cause delays while tracks are cleared. Additionally, it has been reported that one significant rail line experiences air pressure issues when the weather is cold and, as a result, is forced to run shorter trains.Footnote 19 This can result in a shortage of engines, which further reduces the effective capacity of rail.

3.18 During this winter’s peak home heating demand season, propane rail transportation has operated at, or near, full capacity. In this situation, if a shipment is not transported on its scheduled day, it can be cancelled if there is no extra capacity on the following day. When this happens, downstream firms may not obtain their contracted or planned supply.

Downstream Distribution of Propane

3.19 Downstream distributors generally purchase supplies from terminals directly, by sending trains or trucks to those locations, or indirectly, by drawing supplies from another downstream firm’s storage facilities or using third-party shipping.

3.20 Large downstream distributors typically have storage facilities of their own in the form of above-ground “tank farms” containing large propane storage tanks from which delivery trucks (or “tank wagons”) are filled. Smaller firms, particularly those located near a terminal or near a large distributor, may choose to run trucks to the terminal or distributor on a daily basis rather than invest in storage facilities. Downstream firms with a small customer base typically do not own storage assets.

3.21 Downstream distributors that have invested in storage facilities typically have sufficient storage capacity to fulfill one or two days’ worth of peak demand. Downstream distributors have reported that the limited benefitsFootnote 20 of additional storage are outweighed by the financial and regulatory costs associated with storage expansion, especially for downstream distributors with only a small number of customers.Footnote 21

3.22 Purchases by downstream distributors are typically made according to annually-negotiated contracts that specify target volumes and pricing mechanisms. Under these contracts, downstream distributors typically pay a “floating”, variable price upon receipt of their propane supplies (the “rack rate”) and few, if any, are on fixed price contracts. When wholesale prices fluctuate, these changes are reflected in the retail prices paid by end consumers. Most downstream customers pay a retail price at the time of tank filling, with few negotiating fixed price contracts in advance.Footnote 22

3.23 Analysis of the competitiveness of downstream propane markets is ongoing. On one hand, the Superior Propane-ICG Propane merger of the late 1990s monopolized many local propane markets across CanadaFootnote 23 On the other hand, some downstream market participants have indicated that certain local markets are served by multiple distributors. Recent consumer switching from fuel oil to propane for home heating may have contributed to demand increases that induced entry into certain local retail markets.

Household Consumer Demand

3.24 Contractual terms for end-use consumers on floating price contracts vary by retailer, but most allow for immediate customer exit subject to certain costs discussed below. For customers on fixed price contracts, retailers pre-buy equivalent volumes from their suppliers immediately upon entering the contract. Pre-buying in this manner comes at a premium to account for storage costs. This premium is passed on to consumers, which may account in part for limited consumer interest in such contracts.

3.25 Downstream distributors report that they supply propane storage tanks to customers on a rental basis, with a small proportion of customers opting to purchase their own tanks. Once a retailer has placed a rental tank at a customer’s site, no other supplier can fill the tank due to contractual restrictions. If a customer wishes to switch its supplier, downstream distributors often charge fees for tank installation, tank removal, or both. While these fees vary across distributors and depend on the nature of the customer-supplier relationship, they represent a deterrent to customer switching.Footnote 24

3.26 Once a consumer chooses to use propane, significant investments must be made to acquire equipment and appliances that are specifically designed to use propane only.Footnote 25 As a result, these consumers cannot easily switch to other fuels, and it is therefore likely that residential demand for propane is inelastic in the short term.Footnote 26

3.27 Given this inelastic demand, and the significant costs associated with switching from propane to another fuel, consumers have limited options when prices rise.Footnote 27 Households that rely on propane will either consume the same volume of propane and pay substantially more for it, or reduce their consumption in order to partially offset the higher prices. As a result, many Canadians have been significantly impacted by the recent price increases and supply challenges.

The Integrated Canada-U.S. Propane Industry

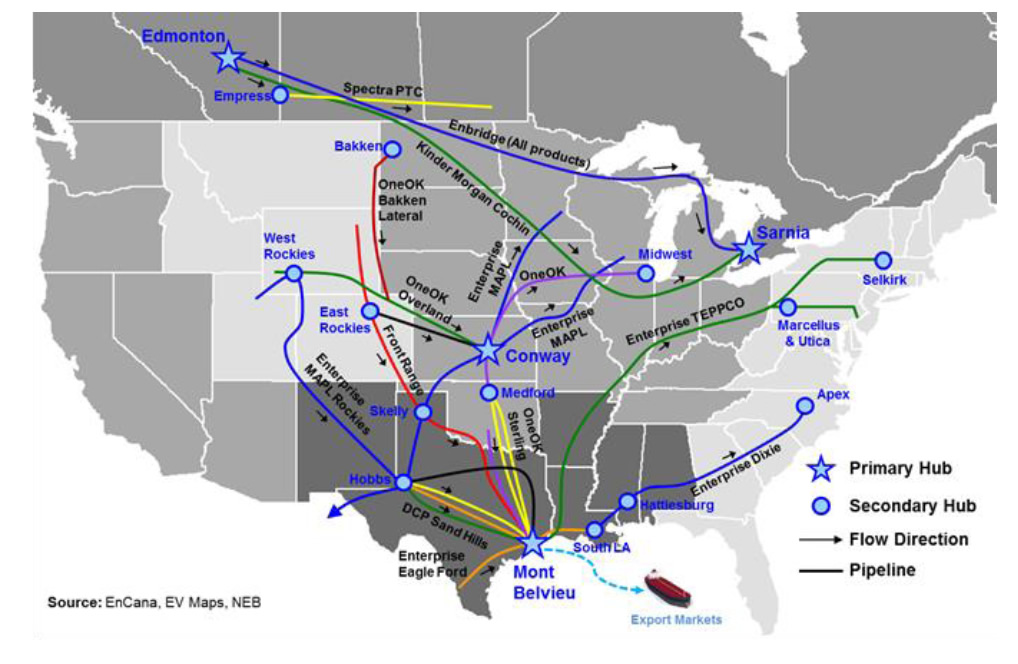

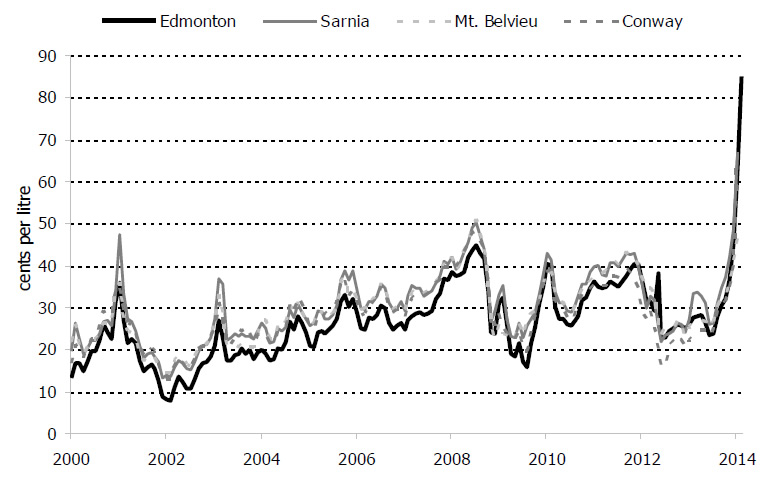

3.28 The Canadian propane sector is highly integrated with its counterpart in the U.S. Canada produces more propane than it consumes and regularly exports to the U.S., its only export market.Footnote 28 Major propane hubs in Canada include Edmonton, Alberta and Sarnia, Ontario. In the U.S., the two largest hubs are Mt. Belvieu, Texas and Conway, Kansas. Figure 3.4 shows these four hubs along with major Canadian and U.S. pipeline infrastructure for natural gas liquids (including propane). Figure 3.5 shows that posted wholesale prices at these four hubs tend to track each other, a further indication of the integrated nature of the Canada-U.S. industries.

Figure 3.4: Major Natural Gas Liquids Pipelines in Canada and the U.S., 2012

The sources of this information are EnCana, EV Maps, and the NEB

Text Version

Figure 3.4: Major Natural Gas Liquids Pipelines in Canada and the U.S., 2012

This is a map of North America showing major natural gas liquids pipelines in Canada and the U.S. as of 2012. Two of these pipelines move propane from Western Canada, where it is produced, to Eastern Canada, where a significant proportion of propane is consumed. The first of these pipelines is the Enbridge pipeline, and the second is the Kinder Morgan Cochin pipeline. Both of these pipelines flow from Edmonton, Alberta to Sarnia, Ontario. There are also a large number of pipelines in the U.S., with primary hubs located in Conway, Kansas and Mont Belvieu, Texas.

The sources of this information are EnCana, EV Maps, and the NEB

Figure 3.5: Monthly Average Posted Propane Prices at Major Canadian and U.S. Hubs, 2000-2014

The sources of this information are Butane-Propane News, and NEB calculations.

Text Version

Figure 3.5: Monthly Average Posted Propane Prices at Major Canadian and U.S. Hubs, 2000-2014

Wholesale propane prices at Edmonton, Alberta; Sarnia, Ontario; Mt. Belvieu, Texas; and Conway, Kansas have generally tracked within 10 cents per litre of each other during the time period of 2000 to 2014. Wholesale prices have generally ranged between 10 and 50 cents per litre from 2000-2013, and prices in late 2013 and early 2014 have risen as high as approximately 85 cents per litre.

The sources of this information are Butane-Propane News, and NEB calculations.

How Canadian Propane Prices are Determined

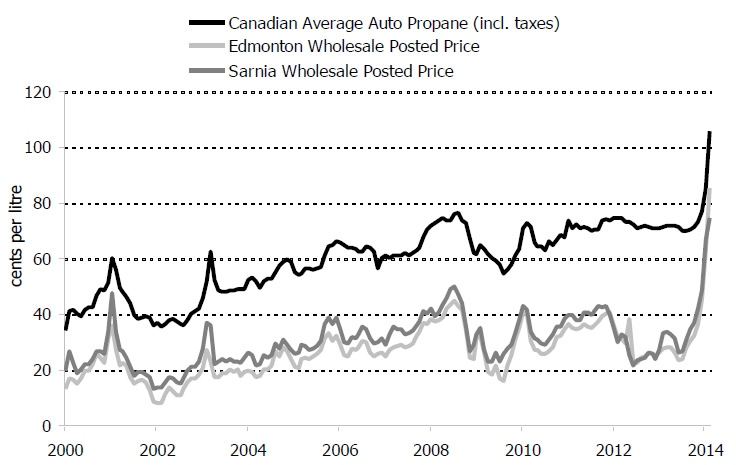

3.29 Retail propane purchases are private transactions involving a downstream distributor and an individual family or business. No centralized data source measures and collects these prices. However, propane prices for automotiveFootnote 29 uses are reported by Natural Resources Canada, and are a potential proxy for home consumption and other propane end usesFootnote 30 Figure 3.6 shows automotive propane retail prices in conjunction with posted Canadian wholesale prices from January 2000 to January 2014, and illustrates their correlation.

3.30 Wholesale contracts are generally negotiated on an annual basis between upstream producers of propane and their midstream and downstream customers using posted prices as references. In these negotiations, buyers and upstream sellers generally do not lock in fixed prices, but negotiate discounts from, or premiums to, posted wholesale prices. Wholesale prices (both actual and posted) are the result of supply and demand in propane markets and, potentially, the behaviour of firms.

Figure 3.6: Canadian Average Retail (Automotive) and Posted Wholesale Propane Prices, 2000-2014

The sources of this information are Kent Marketing Services, Butane-Propane News, and NEB calculations.

Text Version

Figure 3.6: Canadian Average Retail (Automotive) and Posted Wholesale Propane Prices, 2000-2014

Canadian average automotive propane prices have generally exceeded wholesale prices by approximately 20-30 cents per litre from 2000-2014. In late 2013 and early 2014, Canadian average automotive prices increased, from a recent average of approximately 65 cents per litre during 2008 to 2013, to approximately 105 cents per litre in late 2013 and early 2014.

The sources of this information are Kent Marketing Services, Butane-Propane News, and NEB calculations.

3.31 When wholesale prices rise or fall (which increases or decreases producers’ margins), downstream distributors generally pass on this change, at least partially, to end-use consumers. Market participants have indicated that downstream distributors focus on achieving a certain “cents per litre” margin on propane, rather than attempting to earn a particular percentage margin.Footnote 31 Fixed price contracts, in which consumers pay a premium for price certainty, are uncommon for household uses.

4. High Prices and Potentially Anticompetitive Behaviour

4.1 Canadian consumers have experienced high propane prices this winter. In situations where demand is high and supply is tight, this can be an expected short-term result of the market, as prices reflect the scarcity of the good and adjust to allocate the limited supplies of that good to their highest value use in the economy.Footnote 32 In circumstances where high prices occur in an efficient market, economic welfare is maximized by allowing these high prices to persist.Footnote 33 High prices can encourage additional production, or make other sources of supply economical, both of which would ultimately tend to moderate a short term price increase.

4.2 However, high prices can also result from market inefficiencies. In some circumstances, elevated prices may be the result of an exercise of market powerFootnote 34 or an illegal agreement to fix prices in all or part of an industry. In these circumstances, high prices become a symptom of anticompetitive behaviour rather than the outcome of an efficient market. When firms engage in anticompetitive conduct, this typically results in high prices, less selection, lower quality products or services, and a reduction of innovative offerings.

4.3 Some types of anticompetitive conduct can be imposed unilaterally by a single firm, without the need for cooperation between market participants.Footnote 35 This type of behaviour is more common when markets are served by a small number of firms and when barriers to entry and expansion are high. Otherwise, when customers have choice among many competing alternatives, there is a greater potential that customers can switch their purchases to other firms in sufficient numbers to deter anticompetitive behaviour.Footnote 36

4.4 Alternatively, a group of firms can, tacitly or explicitly, coordinate their marketplace actions to effect anticompetitive results. Markets may be more susceptible to this type of behaviour when firms can: (a) mutually recognize the benefits from competing less aggressively with one another; (b) monitor the conduct of other firms and detect deviations from the terms of coordination; and (c) respond to deviations through credible deterrent mechanisms.Footnote 37 When a group of firms engages in coordinated behaviour with anticompetitive outcomes, this conduct can be subject to the civil provisions in the Competition Act.Footnote 38 When firms coordinate their behaviour by engaging in price fixing, bid rigging, or market allocation, this can constitute an indictable offence under the Competition Act, and those found responsible can be subject to imprisonment and fines.Footnote 39

4.5 High prices can also result in times of shortage, typically following disasters or other events that disrupt the normal flow of goods, when sellers use marketplace disruption to artificially increase prices.Footnote 40 This is commonly known as “price gouging”, and is another situation where an inefficient market can result in higher prices. Charging high prices is not, by itself, prohibited in the Competition Act; high prices are a concern under the Competition Act when they are the result of anti-competitive conduct.Footnote 41

4.6 Economics, and in particular the industrial organization branch of economics, provides both a theoretical and empirical framework for analyzing these types of behaviour and the impact they may have on the economy. While economics provides several different models of firm interaction, the basic premise behind industrial organization and competition policy is that more competition results in a more efficient allocation of resources in the economy. When firms engage in the types of behaviour discussed above, market distortion and inefficiency can occur, which can result in higher prices to consumers and harm to the economy.

4.7 The assessment of whether, and to what extent, anticompetitive activities have exacerbated the impact to consumers of recent propane shortages and price spikes is ongoing. This assessment will use the tools available in economics to analyze each level of the Canadian propane industry, and determine if the higher prices consumers are facing may be the result of anticompetitive behaviour. Given the fact that propane is an essential good for some consumers, any such anticompetitive activities would be likely to have substantial negative effects on Canadian consumers.

5. Current Situation

Prices

5.1 Although seasonality and high volatility often characterize propane prices, the price increases this winter are notable for the pace at which they occurred, and for breaking nominal price records. Figure 3.5 and Figure 3.6 illustrate both the size of the price increases this winter and the historic volatility of propane prices more generally.

Production

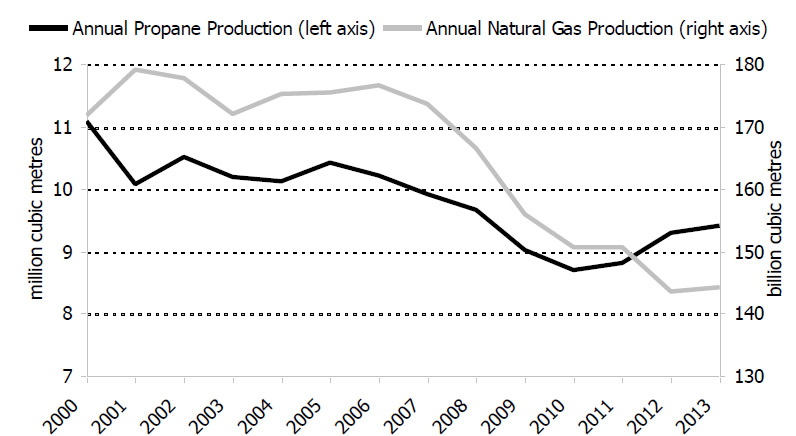

5.2 Canadian gas plant production of propane peaked in 2000, and propane production has been on a steady decline until recent years. Since 2011, higher prices for natural gas liquids relative to the price of natural gas have encouraged the development of more liquids-rich natural gas in western Canada, resulting in a nine per cent increase in gas plant propane production between 2010 and 2013. Figure 5.1 shows annual natural gas and propane production from gas plants, which account for 85 to 90 per cent of total Canadian production. Long-term propane production decreases are correlated with declining natural gas production in Canada.

5.3 Because propane is produced as a by-product of natural gas extraction and crude oil refining, production of propane cannot be expanded without also expanding the production of either natural gas or refined petroleum products – an extensive process that requires significant time and resources, and cannot be achieved in the short term.

Figure 5.1: Canadian Natural Gas Production and Propane Production from Gas Plants, 2000-2013

The sources of this information are Canadian provincial governments and the NEB.

Text Version

Figure 5.1: Canadian Natural Gas Production and Propane Production from Gas Plants, 2000-2013

Annual Canadian natural gas production was roughly constant from 2000-2007, but has been declining since then, from annual levels of approximately 175 billion cubic metres in 2000 to approximately 145 billion cubic metres in 2013. Over this same time period, Canadian propane production fell from approximately 11 million cubic metres to approximately 9.5 million cubic metres; however, in recent years, Canadian propane production has grown from its lowest level of below 9 million cubic metres in 2010.

The sources of this information are Canadian provincial governments and the NEB.

Inventories and Supply

5.4 Table 5.1 displays historical inventory levels and heating season withdrawals in eastern Canada, western Canada, and the U.S. Midwest. The U.S. Midwest is a primary export market for Canadian propane, and is also the U.S. region that relies most heavily on propane for home and space heating needs. Additionally, wholesale prices at U.S. Midwest storage and trading hubs, such as Conway, Kansas, are linked with hubs in Canada, as propane can, at least to some degree, flow to where prices are higher.Footnote 42

5.5 Table 5.1 also illustrates the effect of seasonal temperatures on propane inventories. For example, the 2011-2012 winter was notable for being one of the warmest on record for parts of Canada and the U.S., and the withdrawal of propane in underground inventories in most regions was close to half the size of the withdrawals observed during winters with more “normal” seasonal temperatures, such as the winters of 2010-2011 and 2012-2013.

| Season | Canada West | Canada East | U.S. Midwest (PADD II) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Nov 1 | Mar 1 | Withdrawal | Nov 1 | Mar 1 | Withdrawal | Nov 1 | Mar 1 | Withdrawal | |

| 2008-09 | 793 | 90 | 703 | 516 | 118 | 398 | 3,610 | 2,091 | 1,519 |

| 2009-10 | 956 | 232 | 724 | 548 | 67 | 481 | 4,626 | 1,631 | 2,995 |

| 2010-11 | 1093 | 281 | 812 | 485 | 159 | 329 | 4,246 | 1,512 | 2,734 |

| 2011-12 | 843 | 458 | 385 | 513 | 245 | 268 | 4,036 | 2,588 | 1,448 |

| 2012-13 | 986 | 95 | 891 | 639 | 111 | 528 | 4,332 | 1,831 | 2,501 |

| 2013-14 | 746 | - | - | 524 | - | - | 3,229 | - | - |

| 5-year Average |

934 | 231 | 703 | 540 | 140 | 401 | 4,170 | 1,931 | 2,239 |

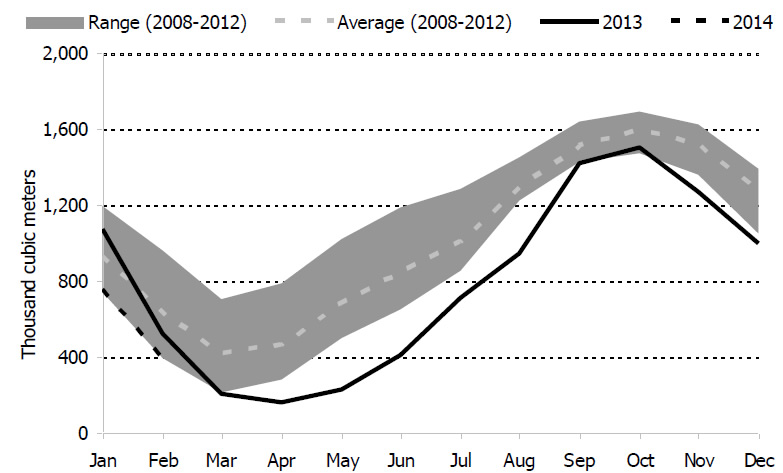

5.6 As displayed in Figure 5.2, Canadian underground propane inventories from the start of the injection season on March 1, 2013 until September were considerably below the five-year range. Unseasonably cold weather in March resulted in inventories declining in Canada at a time when storage usually builds. Furthermore, colder weather continuing into April resulted in storage building at a much slower pace than anticipated. Over the summer, Canadian inventories managed to build at a rate where inventories as of October 1, 2013 were just slightly below the five-year range.

5.7 U.S. Midwest underground propane inventories displayed a similar pattern as shown in Figure 5.3, but despite the large inventory draw observed due to the late end of the heating season, inventories remained within the five-year range through most of 2013. The effect of 2013’s large and wet corn harvest on inventories is noticeable in November when inventories sharply dropped below the five-year range.

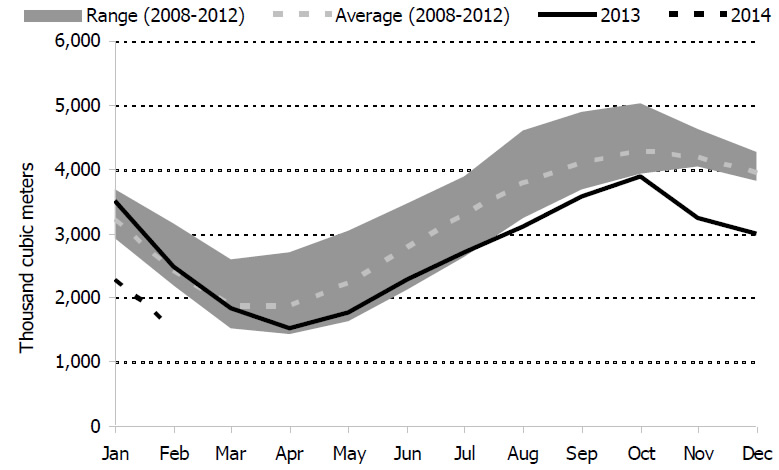

Figure 5.2: Recent Canadian Propane Inventories Compared to Five-Year Range and Average

The source of this information is the NEB.

Text Version

Figure 5.2: Recent Canadian Propane Inventories Compared to Five-Year Range and Average

Canadian propane inventories over the past five years show a season peak in September and October, and a seasonal trough in March and April. From March 2013 to present, Canadian inventories have been at or below the lowest levels experienced in the previous five year period from 2008-2012. From March 2013 to September 2013, Canadian inventories were materially lower than the lowest levels experienced during the previous five year period.

The source of this information is the NEB.

Figure 5.3: U.S. Midwest Propane Inventories in 2013/2014 Compared to Five-Year Range and Average

Text Version

Figure 5.3: U.S. Midwest Propane Inventories in 2013/2014 Compared to Five-Year Range and Average

U.S. Midwest propane inventories over the past five years show a season peak in September and October, and a seasonal trough in March and April. From April 2013 to present, U.S. Midwest inventories have been at or below the lowest levels experienced during the previous five year period from 2008-2012. From October 2013 to February 2014, U.S. inventories have been materially lower than the lowest levels experienced during the previous five year period.

The source of this information is the U.S. Energy Information Administration.

5.8 In early 2014, large storage draws continued in Canada and the U.S. Midwest, primarily due to colder-than-average weather. Recent data suggest that the low inventory situation in the U.S. Midwest is being mitigated by product from the U.S. Gulf Coast flowing northward to U.S. Midwest markets where propane remains in high demand.Footnote 43 However, as of late February 2014, U.S. Midwest inventories still remain low, but are closer to the five-year range.

5.9 Interviews with industry participants indicate that downstream distributors, and ultimately consumers, have had mixed success in acquiring sufficient supplies of propane to meet their needs this winter. Most distributors have been subject to delays of varying lengths in accessing propane supplies, and some have been put on “allotment”, whereby they cannot access the full quantity of propane that they have contracted for. In certain cases, downstream suppliers have been denied supply on a temporary basis, and this has led to shortages of supplies for consumers. These problems seem to have manifested themselves more severely in eastern Ontario and western Quebec than in other areas of Canada.

5.10 Industry interviews also indicated that small-scale propane retailers, particularly those with only one source of supply and no formal supply contract in place, sometimes had to provide less propane than the full amount desired by consumers. Rationing of this nature was reported by smaller suppliers in greater proportion compared to larger, established retailers with diverse supply contracts in place.

Canadian Exports

5.11 Port facilities do not exist in Canada to export propane overseas. Canada does, however, have the ability to export propane to the U.S., and is a net exporter in this context.Footnote 44 The primary U.S. regional markets for Canadian propane are the Midwest and East Coast. In 2013, approximately 85 per cent of Canadian propane exports were to these two regions, with the remaining 15 per cent destined for the Rocky Mountains, West Coast, and Gulf Coast regions. Canadian propane is exported to the U.S. primarily by rail (55 per cent) and pipeline (35 per cent). Trucking is the least cost-efficient method of transporting propane over long distances and accounts for only 10 per cent of Canadian exports.Footnote 45

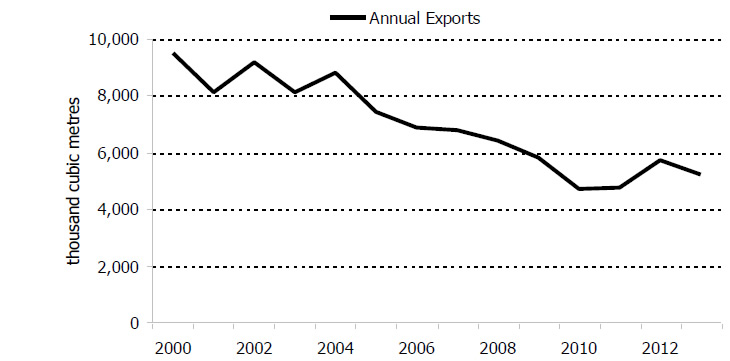

5.12 Figure 5.4 shows the volume of propane exported from Canada to the U.S. from 2000-2013, which has increased recently but has been declining over the long-term. Figure 5.5 compares Canadian exports during 2013 to a five-year range and average. In 2013, Canada exported 5.9 million cubic metres of propane to the U.S., approximately 10 per cent of U.S. consumption. Exports in 2013 were approximately five per cent higher than 2012, which is consistent with average annual growth since 2010, when exports from Canada to the U.S. were at their lowest recent level.

Figure 5.4: Annual Canadian Propane Exports to the U.S., 2000-2013

The source of this information is the NEB.

Text Version

Figure 5.4: Annual Canadian Propane Exports to the U.S., 2000-2013

Annual Canadian propane exports to the U.S. have generally been declining from nearly 10,000 thousand cubic metres in 2000 to less than 6,000 thousand cubic metres in 2013. Annual Canadian propane exports to the U.S. have been roughly constant from 2009-2013, ranging between 5,000 and 6,000 thousand cubic metres per year.

The source of this information is the NEB.

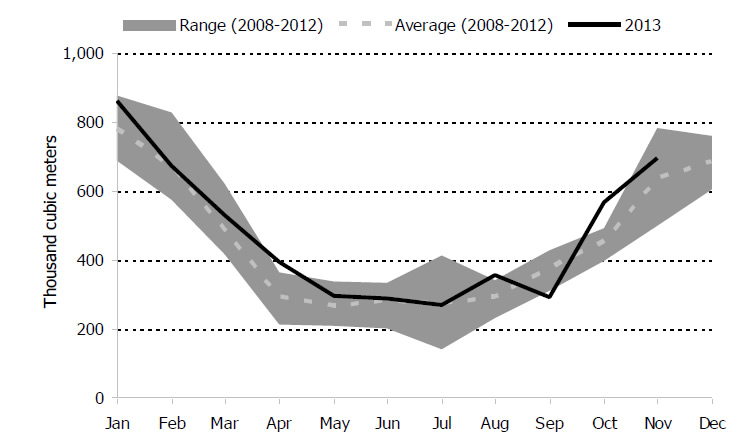

Figure 5.5: Monthly Canadian Propane Exports to the U.S. Compared to 5-Year Range & Average

The source of this information is the NEB.

Text Version

Figure 5.5: Monthly Canadian Propane Exports to the U.S. Compared to 5-Year Range & Average

Monthly Canadian propane exports to the U.S. show a seasonal peak in December and January, and a seasonal trough through the summer months. In 2013, Canadian exports to the U.S. were at or above the five year average for all months other than September, and exports exceeded the highest levels in the previous five year period during April, August, and October 2013.

The source of this information is the NEB.

6. Causes of Recent Propane Shortages and Price Increases

6.1 In general, propane shortages happen because of a mismatch of supply and demand. Propane is produced at a relatively constant rate throughout the year due to its connection to natural gas processing and crude oil refining, and production cannot be quickly expanded or contracted in response to marketplace events. However, since demand is highly seasonal, with large peaks in the fall and winter months, this can lead to situations where demand greatly exceeds supply due to one or both of the following:

- supply shocks, which may temporarily reduce the level of supply at one or more levels of the supply chain and place stress on the ability of the Canadian propane transportation and distribution system to deliver sufficient quantities; and

- demand shocks, which can cause greater-than-anticipated demand in a time period and place stress on distribution capacity.

6.2 As described below, both demand and supply shocks have occurred in the last few months, tightening supply at the same time that demand is very high. Propane inventories in the months preceding the fall and winter demand peaks were also below average, especially in the U.S. The result has been rapidly increasing prices, logistical challenges, and shortages of supply for Canadians who rely on propane.

6.3 In years with less severe demand and/or supply shocks, excess demand can be covered by purchasing supplies from a spot market.Footnote 46 In situations with high sustained demand, however, few market participants have excess propane, and spot markets are unable to fulfill this role at acceptable prices.

Increased Demand given Cold Weather

6.4 The winter of 2013-2014 has been colder than previous winters. Since a significant proportion of annual demand for propane occurs during winter (i.e., for home and space heating), the unusually cold weather has created a demand shock. Retailers indicated in interviews that customer demand for home heating increased by 20 to 25 per cent compared to prior winters.

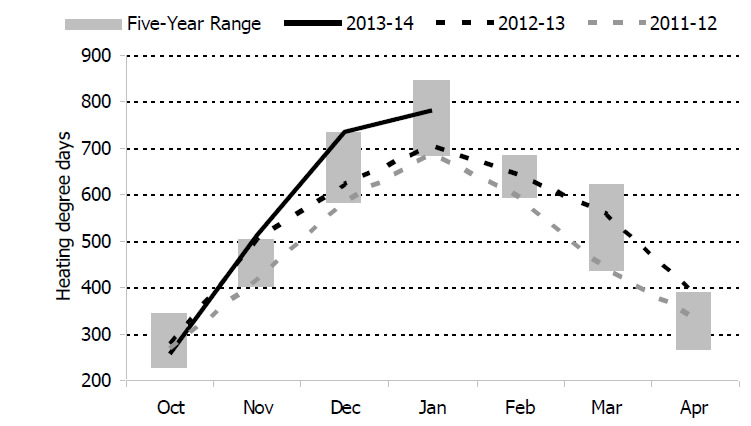

6.5 One way to measure how cold a winter has been in a geographic area is to calculate the number of “heating degree days”Footnote 47 that have been experienced in that area. Figure 6.1 reports the number of heating degree days experienced during the past three winters across Canada, and shows that November and December 2013 were abnormally cold, whereas these same months in 2011 and 2012 were comparatively mild.Footnote 48

Figure 6.1: Canadian Heating Degree Days from October to April, 2011-2014

The sources of this information are the Canadian Gas Association and Environment Canada.

Text Version

Figure 6.1: Canadian Heating Degree Days from October to April, 2011-2014

Monthly heating degree days in Canada during the 2013-2014 winter were at or near five-year highs in October, November, and December 2013. Heating degree days were at or near five-year lows during the 2011-2012 winter, and typically near five year averages or lower during the 2012-2013 winter.

The sources of this information are the Canadian Gas Association and Environment Canada.

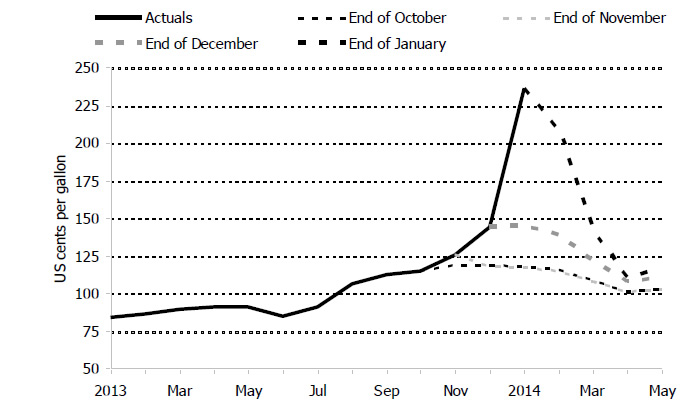

6.6 Firms throughout the Canadian propane supply chain indicated that, when choosing appropriate inventory levels for winter, they make forecasts based on their experience during the past three to five winter seasons. The cold temperatures this winter were unexpected in these forecasts, and this has contributed to propane inventories being drawn down more quickly than anticipated.Footnote 49

6.7 Feedback from industry participants indicated that few industry players accurately predicted either the tight supplies or the price increases currently being experienced. Figure 6.2 presents propane price futures curves at the Conway price hubFootnote 50 at the end of each month from October 2013 to January 2014, and compares these curves to the actual prices experienced during this time period. In each case, the futures markets failed to predict recent price increases.

Figure 6.2: Historical Prices and Futures Curves for Conway, Kansas, April 2013-March 2014

The sources of this information are barchart.com and Conway Propane (OPIS) Futures Prices.

Text Version

Figure 6.2: Historical Prices and Futures Curves for Conway, Kansas, April 2013-March 2014

Futures prices during the month of October 2013 indicated that propane prices were expected to be stable at the Conway, Kansas propane hub during the 2013-2014 winter. In November 2013, December 2013, and January 2014, as actual propane prices rose, futures prices indicated that propane prices were expected to fall back to the price levels experienced during fall 2013.

The sources of this information are barchart.com and Conway Propane (OPIS) Futures Prices.

6.8 As recently as November 30, 2013, weather forecasters were still predicting a mostly mild winter for the major propane-consuming areas of Canada. Figure 6.3 shows that a milder-than-normal winter was predicted for all of southern Ontario, eastern Ontario, western Quebec, Nova Scotia, and eastern Newfoundland and Labrador – all areas where there is significant demand for home heating propane during winter. Figure 6.4 shows an updated forecast, as of December 31, 2013, which predicts a significantly colder winter for most areas of Canada, but still does not foresee a colder-than-normal winter for these high demand areas.

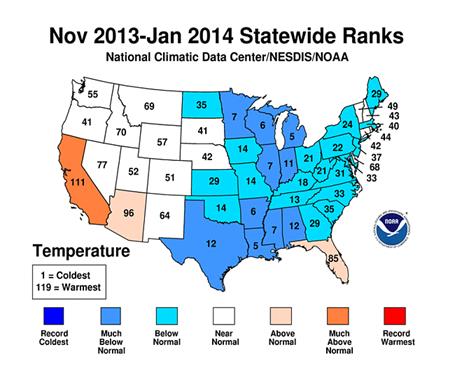

6.9 The eastern half of the U.S. has experienced a similarly cold winter. Figure 6.5 reports that a large number of states experienced weather that was “below normal” or “much below normal”. In a year when Canada experiences cold weather and these states do not, it is possible that supplies could be diverted to Canada. However, the uniform cold felt throughout the eastern portions of Canada and the U.S. this winter indicates that this was not likely possible.

Figure 6.3: Environment Canada’s Seasonal Forecast as of November 30, 2013

The source of this information is Environment Canada.

Text Version

Figure 6.3: Environment Canada’s Seasonal Forecast as of November 30, 2013

As of November 30, 2013, Environment Canada’s seasonal forecast for the December 2013 to February 2014 time period indicated that Southern Ontario, Atlantic Canada, and the northern Territories were all expected to experience above normal temperatures with a probability of 40% or greater. This same forecast predicted below normal temperatures across most of British Columbia, Alberta, and Northern Quebec.

The source of this information is Environment Canada.

Figure 6.4: Environment Canada’s Seasonal Forecast as of December 31, 2013

The source of this information is Environment Canada.

Text Version

Figure 6.4: Environment Canada’s Seasonal Forecast as of December 31, 2013

As of December 31, 2013, Environment Canada’s seasonal forecast for the January to March 2014 time period indicated that Southern Ontario and Atlantic Canada were expected to experience above normal or normal temperatures. This same forecast predicted below normal temperatures across substantially all of the rest of Canada.

The source of this information is Environment Canada.

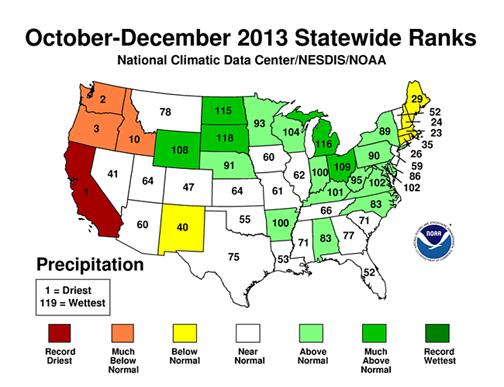

Figure 6.5: U.S. November 2013-January 2014 Temperature Climate Data

The source of this information is National Climatic Data Center/NESDIS/NOAA.

Text Version

Figure 6.5: U.S. November 2013-January 2014 Temperature Climate Data

For the time period of November 2013 to January 2014, every state in the eastern U.S., other than Florida, experienced “below normal” or “much below normal” temperatures.

The source of this information is National Climatic Data Center/NESDIS/NOAA.

6.10 The cold weather experienced across Canada and the U.S. also delayed and/or reduced the volume of propane that has been shipped by train. As mentioned previously, at times of high demand for all propane-related assets, it can be difficult or impossible to make up for such shortcomings in the short run due to congestion issues and tight capacity utilization.

Increased Demand for Crop Drying

6.11 The 2013 corn growing season was longer, and the corn harvest wetter, than average. This had two effects: (1) additional propane was required to dry the very wet corn, and (2) the longer season pushed the seasonal crop drying demand peak closer to the home heating peak demand season, allowing less time for inventoried supply to rebound.Footnote 51 Figure 6.6 shows that much of the U.S. Midwest region, which grows a significant volume of corn, experienced a very wet autumn, with most Midwest states receiving higher than average rainfall. By some reports, this year’s corn crop was 34 per cent larger than 2012,Footnote 52 and agricultural demand for propane may have been as much as five times greater than in 2012.Footnote 53

Figure 6.6: Map of United States Indicating Precipitation during Autumn 2013

The source of this information is National Climatic Data Center/NESDIS/NOAA.

Text Version

Figure 6.6: Map of United States Indicating Precipitation during Autumn 2013

For the time period of October 2013 to December 2014, at least 19 U.S. states experienced “above normal” or “much above normal” amounts of precipitation.

The source of this information is National Climatic Data Center/NESDIS/NOAA.

Supply Chain Congestion and Disruptions

6.12 Congestion experienced at rack sites and other distribution points has contributed, and may continue to contribute, to tight propane supply this winter. This congestion is likely the result of both greater-than-usual demands being placed on propane terminals and other transportation infrastructure, and disruptions related to weather conditions.

6.13 In periods of high demand such as this winter, it may be difficult to make up for even one missed delivery from a terminal to local storage, since terminal access is operating at or near capacity on an ongoing basis. In this respect, even if propane is physically present in the distribution terminal or salt cavern, supplies can only be made available at a maximum daily rate.

6.14 Industry interviews also indicate that two additional factors may have contributed to tight Canadian supply this winter: (1) certain propane production facilities experienced temporary disruptions in December and January, and (2) the Cochin Pipeline, used to transport propane to the U.S. Midwest and eastern Canada, was shut down for maintenance during a portion of November and December.Footnote 54

Decreased Availability due to Increased U.S. Exports

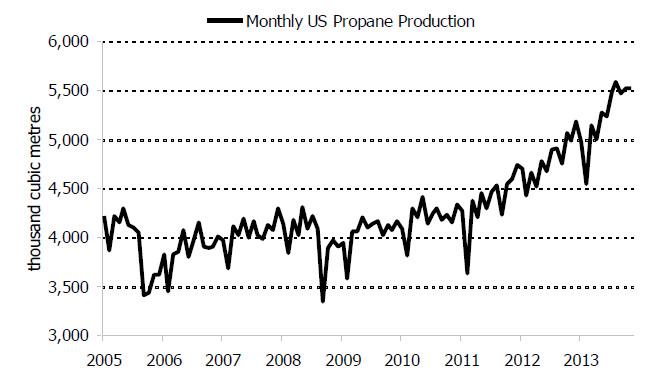

6.15 U.S. propane production has grown in recent years as investments in export infrastructure at major U.S. terminals near Houston, Texas have increased the ability of upstream producers and midstream transporters to participate in overseas markets. Figure 6.7 illustrates the increase in U.S. propane production since 2005.

Figure 6.7: U.S. Propane Production, 2005-2013

The source of this information is the U.S. Energy Information Administration.

Text Version

Figure 6.7: U.S. Propane Production, 2005-2013

U.S. monthly propane production has increased from approximately 4,000 thousand cubic metres in 2005 to approximately 5,500 thousand cubic metres in 2013. From 2005 to 2011, production was roughly constant; however, production has grown from 2011 to 2013.

The source of this information is the U.S. Energy Information Administration.

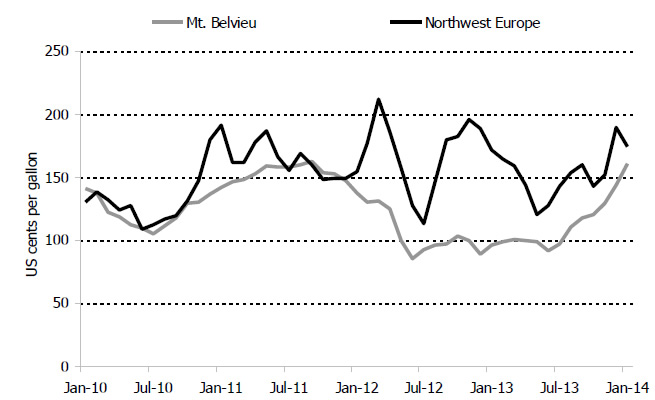

6.16 Figure 6.8 shows that the prices U.S. exporters can obtain overseas have generally compared favourably to domestic prices.

Figure 6.8: Price of Propane in Northwest Europe and the United States Gulf Coast, 2010-2014

The sources for this information are OPIS, Butane-Propane News, and NEB calculations.

Text Version

Figure 6.8 shows that the prices U.S. exporters can obtain overseas have generally compared favourably to domestic prices.

Since late 2011, propane prices in Northwest Europe have exceeded those at a major North American export terminal at Mt. Belvieu, Texas. Prices have been between approximately 10-100 U.S. cents per gallon higher in Europe from January 2011 to January 2014.

The sources for this information are OPIS, Butane-Propane News, and NEB calculations.

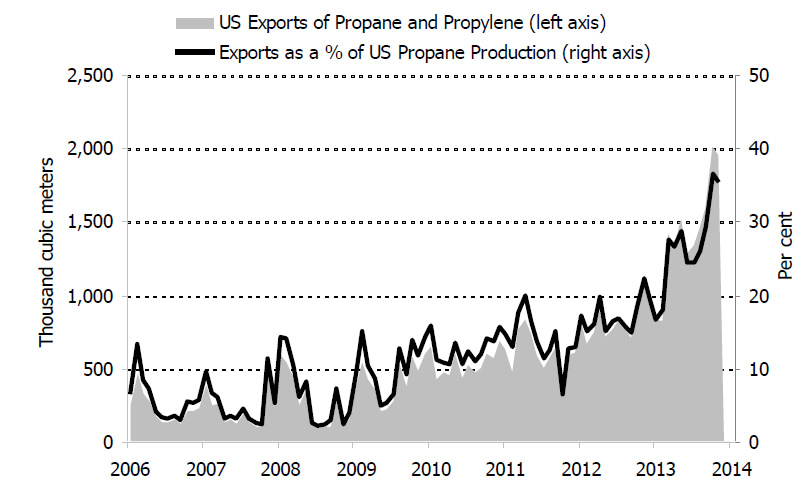

6.17 Figure 6.9 shows that U.S. propane exports have been growing, both in absolute terms and as a proportion of total U.S. production.Footnote 55

Figure 6.9: United States Propane Exports as a Proportion of Total Production, 2006-2014

The source for this information is the U.S. Energy Information Administration.

Text Version

Figure 6.9 United States Propane Exports as a Proportion of Total Production, 2006-2014

U.S. exports of propane, both in absolute terms and as a percentage of total U.S. propane production, have increased from 2010 to 2014. In 2006, approximately 5 to 15% of U.S. propane production was exported each month; in 2013, approximately 20 to 35% was exported.

The source for this information is the U.S. Energy Information Administration.

6.18 Thus, even though U.S. production has increased significantly in recent years, the simultaneous increase in the percentage of U.S. production exported overseas has likely affected the availability of propane in Canada and the U.S. When combined with the low inventories and high demand experienced this winter, these U.S. exports likely impacted the ability of the Canadian propane industry to adjust quickly to the supply and demand shocks of the winter of 2013-2014.

7. Next Steps

7.1 This preliminary report has described the operation of the Canadian propane industry, the current supply and demand situation in Canada, and the NEB and the Bureau’s initial perspectives on the factors that have contributed to recent propane shortages and price increases. This analysis remains preliminary, and the NEB and the Bureau will continue to work together to publish publicly a more detailed final report before April 30, 2014.