{kind=link}

Text Version

Canadian Refineries - Text version

The map illustrates the location, company name and capacity (in barrels per day) of the individual refineries across Canada as of the end of 2015

Map details are:

British Columbia

- Prince George

- Husky Oil: 12,000 barrels per day

- Burnaby

- Chevron Canada: 55,000 barrels per day

Alberta

- Fort Saskatchewan

- Shell Canada: 100,000 barrels per day

- Edmonton

- Imperial Strathcona: 187,000 barrels per day

- Edmonton

- Suncor Energy: 147,000 barrels per day

Saskatchewan

- Regina

- Consumers Co-operative Refineries Limited: 130,000 barrels per day

Ontario

- Sarnia

- Suncor Energy: 85,000 barrels per day

- Imperial Oil: 121,000 barrels per day

- Corunna

- Shell Canada: 75,000 barrels per day

- Nanticoke

- Imperial Oil: 112,000 barrels per day

Quebec

- Montreal

- Suncor Energy: 137,000 barrels per day

- Lévis

- Valero: 265,000 barrels per day

New Brunswick

- Saint John

- Irving Oil: 313,000 barrels per day

Newfoundland

- Come by Chance

- North Atlantic Refining LP : 115,000 barrels per day

Source: NRCan and NEB

Petroleum Products Market

The petroleum products market in Canada is highly competitive, prices paid by consumers may vary based on market conditions.

Refinery economics

The overall economics or viability of a refinery depends on the interaction of three key elements: the choice of crude oil used (crude slates), the complexity of the refining equipment (refinery configuration) and the desired type and quality of products produced (product slate). Refinery utilization rates and environmental considerations also influence refinery economics.

Using more expensive crude oil (lighter, sweeter) requires less refinery upgrading but supplies of light, sweet crude oil are decreasing and the differential between heavier and more sour crudes is increasing. Using cheaper heavier crude oil means more investment in upgrading processes. Costs and payback periods for refinery processing units must be weighed against anticipated crude oil costs and the projected differential between light and heavy crude oil prices.

Crude slates and refinery configurations must take into account the type of products that will ultimately be needed in the marketplace. The quality specifications of the final products are also increasingly important as environmental requirements become more stringent.

Crude oil input

Crude oil is the primary input into the petroleum refining industry. While Canada is a large and growing net oil exporter, crude oil imports satisfy more than half of domestic refinery demand. The transportation costs associated with moving crude oil from the oil fields in Western Canada to the consuming regions in the east and the greater choice of crude qualities make it more economic for some refineries to use imported crude oil. Therefore, Canada's oil economy is now a dual market. Refineries in Western Canada run domestically produced crude oil, refineries in Quebec and the eastern provinces run primarily imported crude oil, while refineries in Ontario run a mix of both imported and domestically produced crude oil. In more recent years, eastern refineries have begun running Canadian crude from east coast offshore production.

Regardless of the source of crude oil, the price is determined in the world market and both imported and domestic crude oil is priced according to the supply/demand balance and pricing dynamics on the world oil market. In this respect, Canadian refiners are “price takers” and have very little influence on the price they pay for crude oil. Using more expensive crude oil (lighter, sweeter) requires less refinery upgrading but supplies of light, sweet crude oil are decreasing and the differential between heavier and more sour crudes is increasing. Using cheaper heavier crude oil means more investment in upgrading processes. Costs and payback periods for refinery processing units must be weighed against anticipated crude oil costs and the projected differential between light and heavy crude oil prices.

Crude slates and refinery configurations must take into account the type of products that will ultimately be needed in the marketplace. The quality specifications of the final products are also increasingly important as environmental requirements become more stringent.

Crude slates

Different types of crude oil yield a different mix of products depending on the crude oil's natural qualities. Crude oil types are typically differentiated by their density (measured as API gravity) and their sulphur content. Crude oil with a low API gravity is considered a heavy crude oil and typically has a higher sulphur content and a larger yield of lower-valued products. Therefore, the lower the API of a crude oil, the lower the value it has to a refiner as it will either require more processing or yield a higher percentage of lower-valued by-products such as heavy fuel oil, which usually sells for less than crude oil.

Crude oil with a high sulphur content is called a sour crude while sweet crude has a low sulphur content. Sulphur is an undesirable characteristic of petroleum products, particularly in transportation fuels. It can hinder the efficient operation of some emission control technologies and, when burned in a combustion engine, is released into the atmosphere where it can form sulphur dioxide. With increasingly restrictive sulphur limits on transportation fuels, sweet crude oil sells at a premium. Sour crude oil requires more severe processing to remove the sulphur. Refiners are generally willing to pay more for light, low sulphur crude oil.

Most refineries in Western Canada and Ontario were designed to process the light sweet crude oil that is produced in Western Canada. Unlike leading refineries in the U.S., Canadian refineries in these regions have been slower to reconfigure their operations to process lower cost, less desirable crude oils, instead choosing to rely extensively on the abundant, domestically produced, light, sweet crudes. As long as these lighter crudes were available, refining economics were insufficient to warrant new investment in heavy oil conversion capacity.

However, with growing oil sands production and the declining production of conventional light sweet crudes, refineries in Western Canada and Ontario have started to make the investment required to process the increasing supply of heavier crudes. Much of this investment by the large integrated oil companies (companies that are involved in both the production of crude oil and the manufacturing and distribution of petroleum products) is associated with ensuring a market for their growing oil sands production.

In Western Canada and Ontario, almost 50% of the crude oil processed by refiners is conventional light, sweet crude oil and another 25% is high quality synthetic crude oil. Synthetic crude is a light crude oil that is derived by upgrading oil sands. Most of the remaining crude oil processed by these refineries is heavy, sour crude. The crude slate is expected to change significantly in the years ahead as refiners increase their capacity to process heavy crude oil and lower quality synthetic crudes.

Refineries in Atlantic Canada and Quebec are dependent on imported crudes and tend to process a more diverse crude slate than their counterparts in Western Canada and Ontario. These refiners have the capacity to purchase crude oil produced almost anywhere in the world and therefore have incredible flexibility in their crude buying decisions. Approximately 1/3 of crude processed in Eastern Canada and Quebec is conventional, light sweet crude and another 1/3 is medium sulphur, heavy crude oil. The remaining 1/3 is a combination of sour light, sour heavy and very heavy crude oil. The crude slate in Eastern Canada is expected to remain much more static than that in Western Canada and Ontario, as these refiners are not constrained by the quality or volume of domestic crude production.

Refinery configuration

A refiner's choice of crude oil will be influenced by the type of processing units at the refinery. Refineries fall into three broad categories. The simplest is a topping plant, which consists only of a distillation unit and probably a catalytic reformer to provide octane. Yields from this plant would most closely reflect the natural yields from the crude processed. Typically only condensates or light sweet crude would be processed at this type of facility unless markets for heavy fuel oil (HFO) are readily and economically available. Asphalt plants are topping refineries that run heavy crude oil because they are only interested in producing asphalt.

The next level of refining is called a cracking refinery. This refinery takes the gas oil portion from the crude distillation unit (a stream heavier than diesel fuel, but lighter than HFO) and breaks it down further into gasoline and distillate components using catalysts, high temperature and/or pressure.

The last level of refining is the coking refinery. This refinery processes residual fuel, the heaviest material from the crude unit and thermally cracks it into lighter product in a coker or a hydrocraker. The addition of a fluid catalytic cracking unit (FCCU) or a hydro cracker significantly increases the yield of higher-valued products like gasoline and diesel oil from a barrel of crude, allowing a refinery to process cheaper, heavier crude while producing an equivalent or greater volume of high-valued products.

Hydrotreating is a process used to remove sulphur from finished products. As the requirement to produce ultra low sulphur products increases, additional hydrotreating capability is being added to refineries. Refineries that currently have large hydrotreating capability have the ability to process crude oil with a higher sulphur content.

Canada has primarily cracking refineries. These refineries run a mix of light and heavy crude oils to meet the product slate required by Canadian consumers. Historically, the abundance of domestically produced light sweet crude oils and a higher demand for distillate products, such as heating oil, than in some jurisdictions reduced the need for upgrading capacity in Canada. However, in more recent years, the supply of light sweet crude has declined and newer sources of crude oil tend to be heavier. Many of the Canadian refineries are now being equipped with upgraders to handle the heavier grades of crude oil currently being produced.

Product slates

Refinery configuration is also influenced by the product demand in each region. Refineries produce a wide range of products including: propane, butane, petrochemical feedstock, gasolines (naphtha specialties, aviation gasoline, motor gasoline), distillates (jet fuels, diesel, stove oil, kerosene, furnace oil), heavy fuel oil, lubricating oils, waxes, asphalt and still gas. Nationally, gasoline accounts for about 40% of demand with distillate fuels representing about one third of product sales and heavy fuel oil accounting for only eight percent of sales.

Total petroleum product demand is distributed almost equally across the regions, with Atlantic/Quebec, Ontario and the West each accounting for about one third of total sales. However, the mix of products varies quite significantly among the regions.

In the Atlantic provinces, where furnace oil (light heating oil) is the primary source of home heating, distillate fuels make up 40% of product demand, and heavy fuel oil, used to generate electricity, accounts for another 24%. Gasoline sales account for less than 30% of product demand.

In Quebec, where natural gas and hydroelectricity are prevalent, distillate fuel has a 34% share of sales and gasoline is about 40%. Similarly, in Ontario, gasoline sales outpace distillate sales and account for more than 45% of total product demand, with distillates at less than 30%.

In Western Canada, agricultural use is one of the primary drivers behind distillate demand and gasoline and distillate each account for about 40% of total petroleum product sales. These regional differences in product demand have influenced the configurations of the refineries in each area.

By comparison, in the U.S., the demand for gasoline is much larger than distillate demand and, therefore, refiners configure their installations to maximize gasoline production. Gasoline sales account for nearly 50% of demand while distillate sales account for less than 30% of product demand. In several Western European countries, most notably Germany and France, policies exist that encourage the use of diesel engines creating a much stronger distillate component. Gasoline accounts for less than 20% of petroleum product sales in Europe.

The US refineries are configured to process a large percentage of heavy, high sulphur crude and to produce large quantities of gasoline, and low amounts of heavy fuel oil. U.S. refiners have invested in more complex refinery configurations, which allow them to use cheaper feedstock and have a higher processing capability.

Canada's refineries do not have the high conversion capability of the US refineries, because, on average, they process a lighter, sweeter crude slate. Canadian refineries also face a higher distillate demand, as a percent of crude, than those found in the U.S. so gasoline yields are not as high as those in the US, but are still significantly higher than European yields.

The relationship between gasoline and distillate sales can also create challenges for refiners. A refinery has a limited range of flexibility in setting the gasoline to distillate production ratio. Beyond a certain point, distillate production can only be increased by also increasing gasoline production. For this reason, Europe is a major gasoline exporter, primarily to the U.S.

Refinery utilization

Another critical component of refining economics is the utilization rate, or how efficiently the refining complex is operating. The Canadian refining sector has undergone significant rationalization in the last three decades. In the early 1970s, there were 40 refineries in Canada. Since that time several factors have contributed to a major rationalization of company operations. The oil price shocks in 1973 and 1979 led to improvements in the efficiency of vehicles and to fuel switching from oil to natural gas and electricity. This curbed the demand for petroleum products and resulted in a substantial surplus of refining capacity. The spare capacity resulted in increased competition among refiners, which further eroded refining margins. Less efficient, smaller refiners were closed, sometimes in favor of new larger facilities.

Weak economic conditions in the early 1980s put additional pressure on the industry to rationalize their operations, resulting in a significant number of refinery closures. Today there are 19 refineries producing petroleum products in Canada. However, due to expansions at the remaining refineries over the last decade, current refining capacity in Canada is greater than it was in the 1970s.

In recent years, growth in the demand for petroleum products has led to an improvement in capacity utilization, increasing operating efficiency and reducing costs per unit of output. As a result, refinery utilization rates have been above 90% nationally for six of the last ten years. A utilization rate of about 95% is considered optimum as it allows for normal shut downs required for maintenance and seasonal adjustments.

Refinery capacity is based on the designed size of the crude distillation unit(s) of a refinery (often referred to as nameplate capacity). Occasionally, through upgrades or de-bottlenecking procedures, refineries can process more crude than the nameplate size of the distillation unit would indicate. In such cases, a refinery is able to achieve a utilization rate greater than 100 percent for short periods of time.

Environmental initiatives

Not all investment decisions are driven by refinery economics. Refiners also make investment decisions because of voluntary actions or legislative and regulatory requirements. In recent years, governments and industry have directed considerable effort towards reducing the environmental impact of burning fossil fuels. Many of the initiatives have been aimed at providing ‘cleaner´ fuels for Canadians. Petroleum refining is a very complicated and capital-intensive industry. New environmental regulations require industry to make additional investments to meet the more stringent standards.

Product supply and demand

The Persian Gulf War drove oil prices up in 1990-91, dampening demand and leading to a economic downturn. Since 1992 demand for petroleum products has been growing steadily at a rate of about 1 percent per year. However, product demand is a moving target and the demand for each product does not always grow at the same pace.

Gasoline demand has increased slightly in most of the last 10 years. The distillate demand (diesel oil, furnace oil and kerosene), driven primarily by on-road diesel requirements, dipped during the economic recession in 1991-92 but has been the fastest growing component since 1993. Because of the significant proportion of distillate demand that comes from the trucking industry, this component is the most closely linked with economic activity.

Some of the distribution challenges arise from the fact that petroleum products are refined in only a few geographic regions but they are consumed all across Canada. Of the western provinces, only Alberta and Saskatchewan produce more products and they consume. Manitoba and parts of British Columbia and most of the territories are supplied primarily from the three refineries in Edmonton.

Refined petroleum product production vs. sales

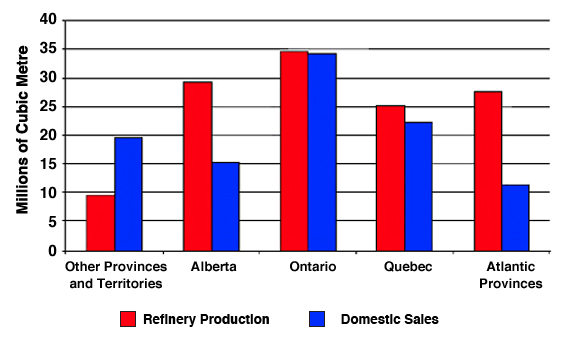

Text Version

The chart illustrates petroleum refinery production versus domestic sales in Canada.

Alberta

- Refinery production: 29 million cubic metres*

- Domestic sales: 15 million cubic metres*

Ontario

- Refinery production: 35 million cubic metres*

- Domestic sales: 34 million cubic metres*

Quebec

- Refinery production: 25 million cubic metres*

- Domestic sales: 22 million cubic metres*

Atlantic Provinces

- Refinery production: 27 million cubic metres*

- Domestic sales: 11 million cubic metres*

Other provinces and territories

- Refinery production: 9 million cubic metres*

- Domestic sales: 20 million cubic metres*

*approximate value

Source: Statistics Canada 45-004, 2004

Quebec and Ontario together are close to being in balance with significant volumes moving from Quebec to Ontario since the closure of the Oakville refinery. Atlantic Canada is a major exporter of petroleum products. However, even the provinces that are self-sufficient must still move petroleum products over long distances to supply all of their customers.

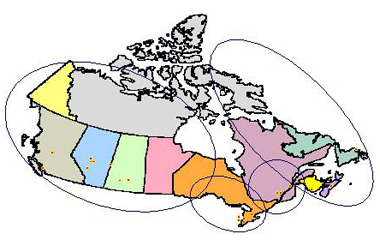

The figure below illustrates how far product is moved in Canada. Western refineries supply all product demand from Vancouver to Thunder Bay, including the northern territories. Refiners in southern Ontario move product to Sault Ste-Marie, northern Ontario and as far east as Ottawa. Montreal and Quebec City facilities supply the St Lawrence River corridor from Toronto to the Gaspé Peninsula, as well as the more remote areas of northern Quebec and occasionally parts of the Arctic. Petroleum products from the three Atlantic refineries find their way to the Arctic and Hudson Bay regions as well as the U.S. eastern seaboard.

Refinery supply orbits

Trade - crude oil market

Canada is a net exporter of petroleum products. Yet, at times, product imports can play a significant role in satisfying petroleum product demand. The availability of both crude oil and petroleum product imports in every region hinges on geographic constraints. Each of these regions has its own natural features and this creates some unique situations.

Some regions are better suited than others to import products. Because of their connection via major waterways, Atlantic Canada and Quebec have good access to supplies from the northeastern United States and Europe. Because of there easy access to water for both importing crude oil feedstocks and for exporting petroleum products, Atlantic Canada has two large export refineries that send large portions of their output to market on the U.S. eastern seaboard. When economic conditions are favourable, East Coast Canadian refiners have sent products to markets as far away as California.

Ontario also has access to supplies from large U.S. markets and can also bring in provisions via Quebec. However, logistical constraints, such as the size of ships that can navigate the Seaway and the seaway-shipping season, increase the cost of these supplies. Other modes of transportation, such as pipeline, unit train and trucking, are necessary to bring in products from other regions.

Western Canada is landlocked, and as such, has very limited access to supplies from other regions. The current infrastructure was not designed to transport supplies to the Prairies from other regions. However, the prairies supply a substantial volume of gasoline into the Vancouver market. In the event of a supply shortage in the Prairies, refiners have the ability to balance supply and demand by importing product into Vancouver from Washington State. This frees up additional product from Edmonton area refiners to be distributed to prairie markets.

Inventory levels

To provide added flexibility to the distribution of petroleum products, refiners and marketers maintain inventories of the various products in strategic locations throughout the distribution chain. If supplies of imported or domestic crude oil were interrupted for any reason, or if the product distribution system failed, companies would rely on commercial inventories to meet short-term needs while alternate arrangements were being made.

Canadian crude oil and petroleum product inventories have been relatively stable for the last five years. Inventory levels for some products, such as gasoline and furnace oil, fluctuate significantly over the year. Demand for these products is very seasonal and at its peak can exceed the production capacity of refineries. Therefore, refiners need to anticipate the peak consumption periods by building inventories in advance. Gasoline inventories increase during the first quarter of the year and are used during the summer months to supplement refinery production. Furnace oil stocks grow during the fall and are drawn during the coldest months of winter when demand is at its highest level.

Refiners also build up inventories of all products in advance of scheduled refinery maintenance (called turnarounds). Turnarounds can vary in frequency from annually to once every few years and sometimes require the refinery to be completely shut down for a period of several weeks. Refiners anticipate this by building up product stocks that can be used during the turnaround.

Refiners´ crude oil inventories fluctuate over a very narrow band and are less seasonal than product stocks. There are significant regional variations in crude oil stocks, with refiners in the West, who run domestic crude oil maintaining about 5-7 days of oil, and refiners in eastern Canada who run imported crude oil averaging 15-20 days.

Demand and consumption

Due to logistics and transportation costs, crude oil imports satisfy about 35% of domestic refinery demand. Refineries in western Canada run domestically produced crude oil, while refineries in Quebec and the Atlantic provinces run primarily imported crude oil. Refineries in Ontario run a mix of both imported and domestically produced crude oil.

On average, Ontario and Quebec account for about 55% per cent of the gasoline consumed in Canada. The western provinces account for about 36% of Canada's gasoline consumption, while the remaining 9% of gasoline is consumed in the Atlantic provinces and the Territories.

On average, Ontario and Quebec account for about 47% of the diesel fuel consumed in Canada, while the western provinces account for about 44%. The relatively greater dependence on diesel in western Canada reflects regional differences in fleet composition and the comparatively greater need to truck in most manufactured goods to the West from outside the region.