Updated forecasts of vehicle charging needs, grid impacts and costs for all vehicle segments

February 2024

Prepared for:

Natural Resources Canada

Natural Resources Canada

Submitted to:

Natural Resources Canada

Lawrence Ejike

Engineer, Transportation and Fuel Decarbonization Programs Branch

natural-resources.canada.ca

Dunsky Project Number: 23028

Prepared by:

Dunsky Energy + Climate Advisors

50 Ste-Catherine St. West, suite 420

Montreal, QC, H2X 3V4

www.dunsky.com | info@dunsky.com

+ 1 514 504 9030

With support from:

The International Council on Clean Transportation (ICCT)

The International Council on Clean Transportation (ICCT)

Executive Summary

To meet its climate targets, Canada must reduce GHG emissions from the transportation sector, responsible for 22% of national emissions in 2021. This will require a rapid transition from internal combustion engine (ICE) vehicles to electric vehicles (EVs) and other zero-emission vehicles (ZEVs), alongside other measures like increasing the use of public transit and active transportation. The federal government has set rising sales targets for ZEVs, reaching 100% by 2035 for new light-duty vehicles (LDVs) and 2040 for medium- and heavy-duty vehicles (MHDVs) where feasible.Footnote 1 To achieve this, the government published its Electric Vehicle Availability Standard in December 2023 which will apply to LDV sales starting in 2026. The government is also developing a strategy and regulations to support its MHDV targets.

A key component of these targets will be ensuring sufficient availability of EV charging infrastructure across Canada. Natural Resources Canada (NRCan) commissioned Dunsky Energy + Climate Advisors (Dunsky) and the International Council on Clean Transportation (ICCT) to develop updated charging forecasts for Canada and its provinces and territories, plus key urban regions, for the period 2025 to 2040. Our study expands on previous studies by updating our methodology, incorporating MHDVs, exploring how EV growth will increase demand on electricity grids, and estimating the capital costs and electrical grid investments needed.

Our key findings are as follows:

1. Growing EV adoption will drive the need for public charging infrastructure and EV ready multifamily buildings.

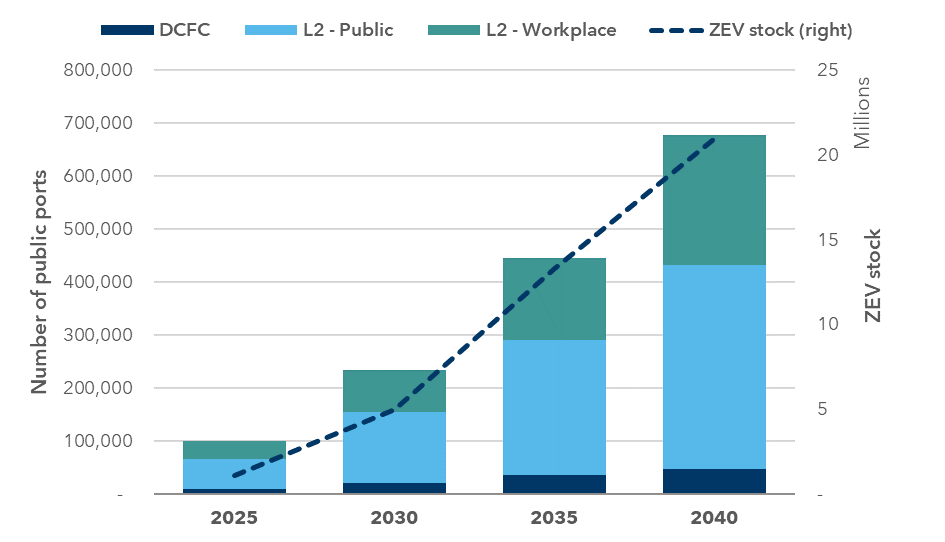

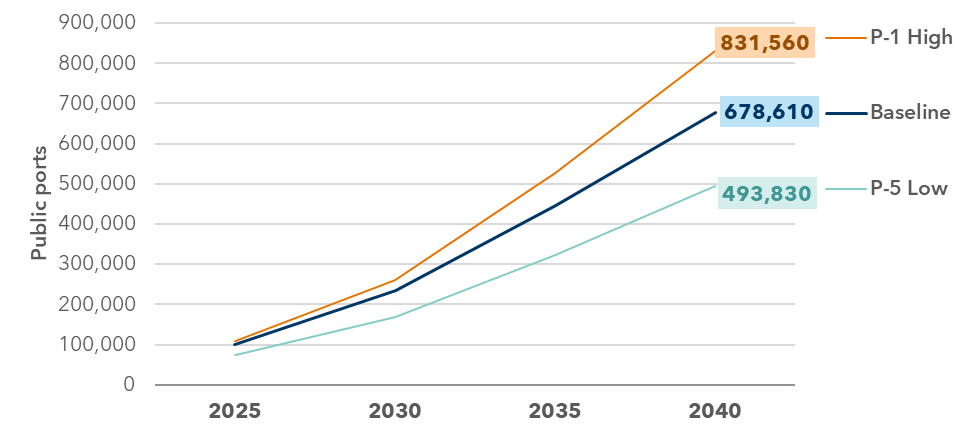

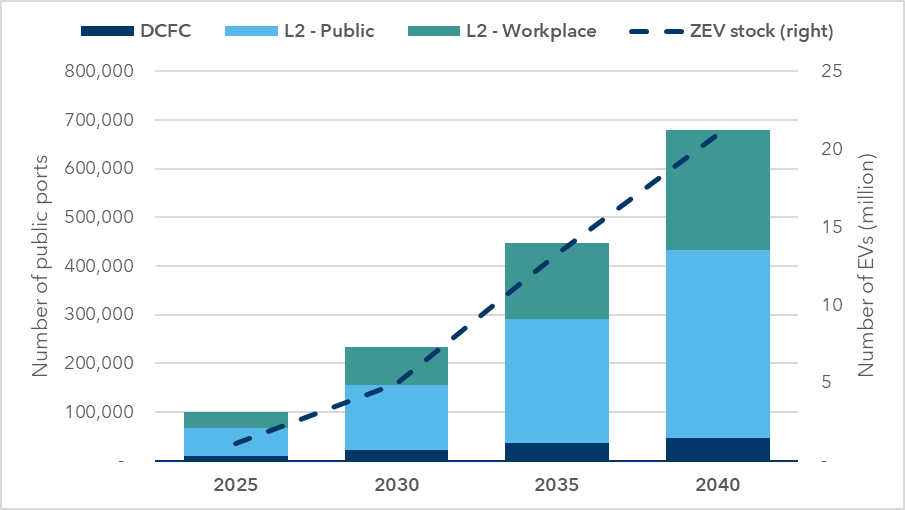

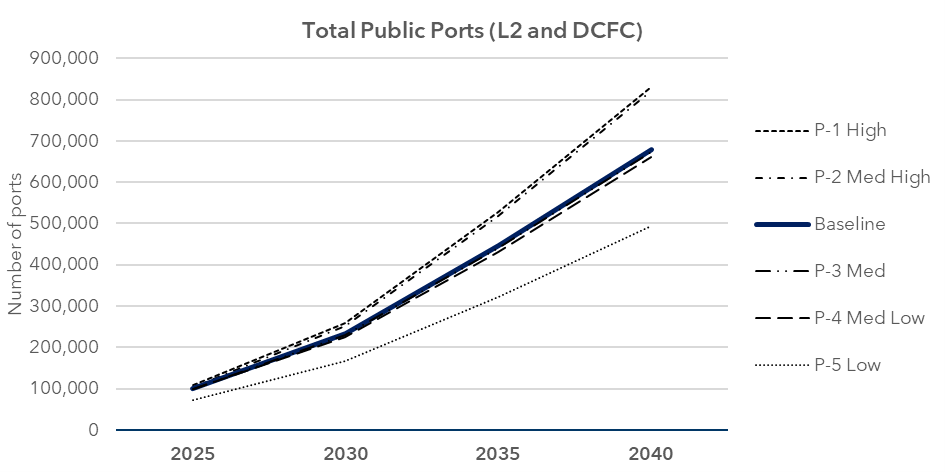

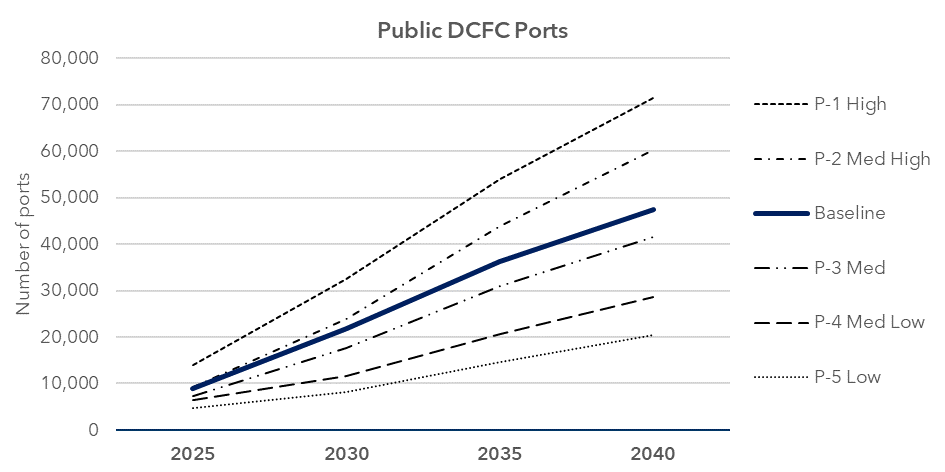

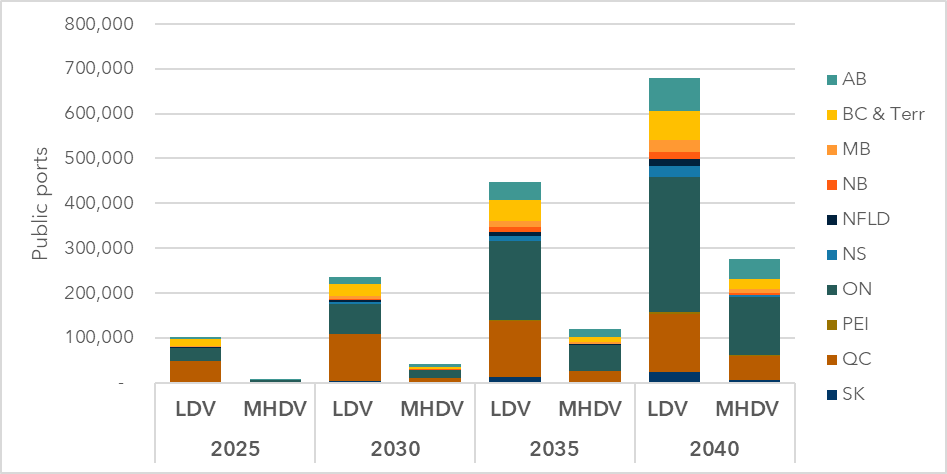

Based on the EV Availability Standard and provincial ZEV Sales Mandates, the number of zero-emission LDVs on the road is expected to grow from approximately 480,000 today to 5 million by 2030, and eventually reach 21 million in 2040.Footnote 2 Under our baseline scenario, this will require about 679,000 public charging ports (a mix of Level 2 [L2] and direct current fast charging [DCFC]) across the country in 2040, or one port for every 31 light-duty EVs (Figure ES 1). This will require the installation of, on average, 40,000 public ports each year between 2025 and 2040, on top of the nearly 30,000 public ports currently available or planned in Canada.Footnote 3

Most EV charging is done at home, but many Canadians in multifamily housing will be unable to install chargers unless existing buildings are retrofitted and new buildings are required to be EV ready. Our baseline scenario is a high home charging access scenario where governments and building owners invest in retrofits of 1.6 million parking spaces in multifamily buildings by 2030 (30% of units that exist today) and nearly 3.2 million by 2035 (60% of units that exist today). Simultaneously, this scenario assumes policy changes that require all new housing to be EV ready starting in 2030. This will require a concerted effort by all levels of government to incentivize and require EV ready retrofits through a mix of regulations (e.g., updates to the building and/or electrical codes) and financial incentives.

Note: DCFC stands for ‘direct current fast charger’. L2 stands for Level 2.

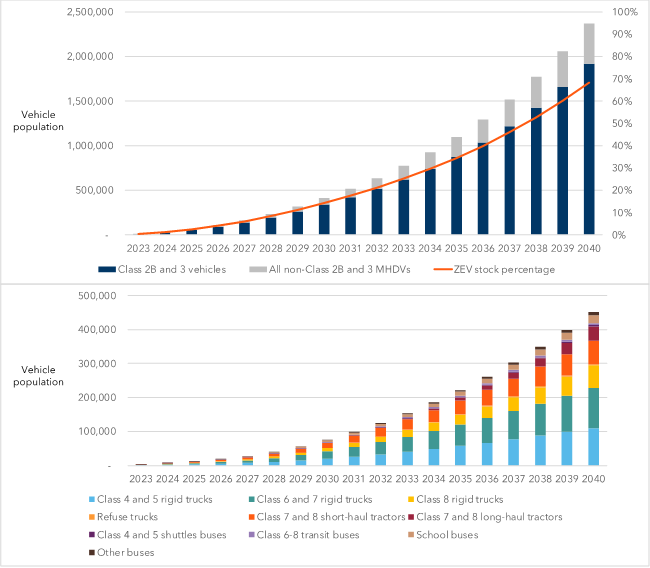

2. Adoption of zero-emission MHDVs—and the demand for associated charging infrastructure—is in its infancy but is likely to undergo rapid growth in the coming decade.

For the first time, this study estimates the charging needs for MHDVs to support the federal sales target of 100% zero-emission MHDVs by 2040, where feasible. We assume that battery electric vehicles (BEVs) will be the predominant technology, based on previous research by the ICCT and other groups.Footnote 4 However, we also model an alternate scenario under which hydrogen costs fall to competitive levels and a portion of the HDV fleet switches from BEVs to hydrogen-fueled ZEVs (either fuel cell electric vehicles or hydrogen combustion vehicles), and assess by how much the demand for electric charging would be reduced as a result. We do not attempt to model hydrogen refueling infrastructure needs.

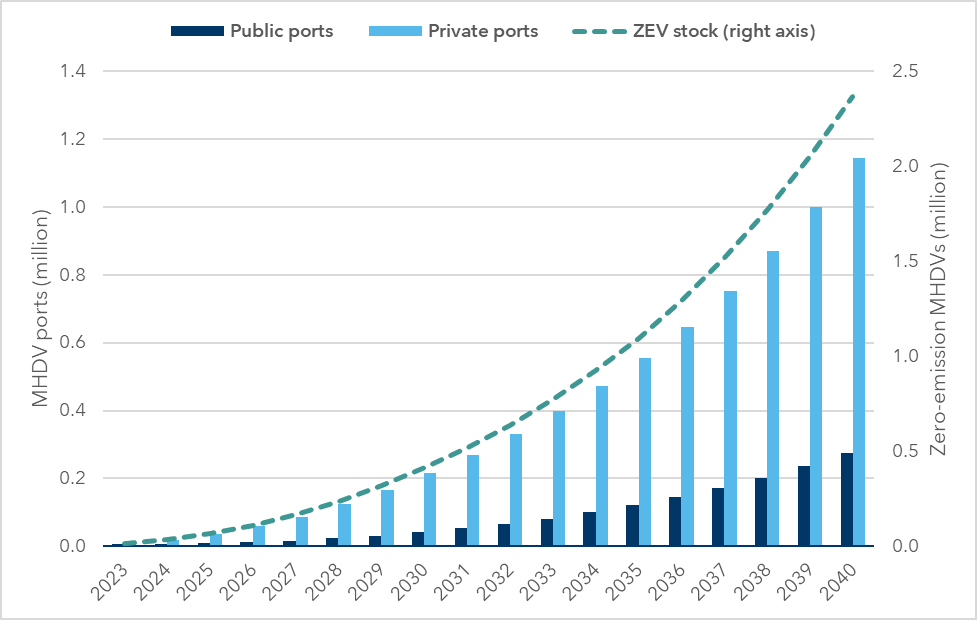

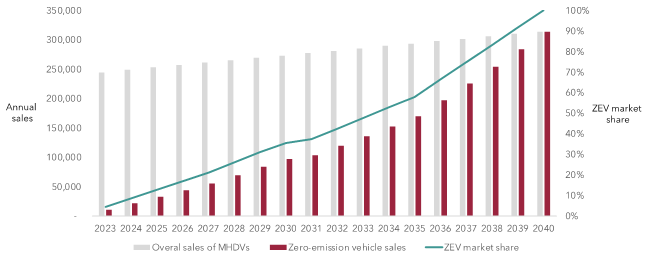

To meet the upper range of the federal sales targets, the number of zero-emission MHDVs on the roads under our policy reference scenario grows to 414,000 in 2030 and 2.4 million by 2040. Relative to LDVs, the growth of demand for public MHDV chargingFootnote 5 starts at close to zero today but grows comparatively quickly over the near term, reaching 41,000 ports in 2030, before growing rapidly to reach 120,000 in 2035 and 275,000 in 2040 (Figure ES 2). Private MHDV charging (including overnight charging in fleet depots and opportunity charging at destination locations such as warehouses) will also play a critical role in electrification of the MHDV fleet, especially in early market development stages. We expect that private and fleet depot charging will require an additional 217,000 ports in 2030 and 1.1 million in 2040.

3. Significant capital investments by governments and private actors will be required between now and 2040 to meet these charging requirements.

Deploying EV charging infrastructure will involve capital costs, including equipment, installation and local electrical upgrades. We developed estimates of national and regional capital costs for the deployment of both LDV and MHDV charging infrastructure, based on per-port cost estimates for various port types, and without considering necessary upgrades to electricity grids (discussed in Section 5).

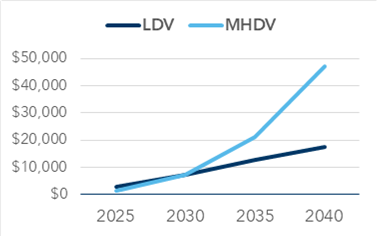

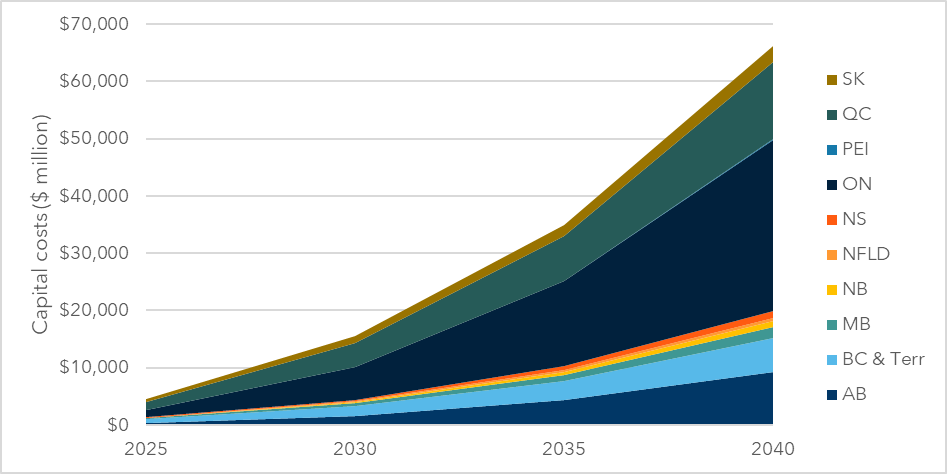

For LDVs, the cumulative capital costs to 2040 for public charging is nearly $18 billion under our baseline scenario. DCFC ports account for 64% of these costs despite making up a small share of ports (7%), due in part to their significant and growing power requirements (from an average of 125 kW per port in 2025 to 300 kW in 2040). For MHDVs, capital costs are generally higher on a per-port basis due to the higher average charging power needs for heavier vehicles with larger batteries. Cumulative capital investments of $47 billion are needed by 2040 to support public charging needs in the MHDV sector (Figure ES 3).

These significant investments in public charging infrastructure will be spread out over the next 15 years. However, the timing is different for each vehicle category. LDV capital costs remain constant – at about $1 billion annually – over the study period. Meanwhile, MHDV capital costs grow from $340 million in 2025, to more than $1.7 billion by 2030, and $6.4 billion by 2040. MHDV charging will also require significant grid upgrades that can be costly and involve long lead times. The associated investments need to happen up to 10 years before the chargers are deployed in order to ensure sufficient power is available at the charging sites. Significant investments for MHDV charging are therefore also expected prior to 2030.

Figure ES 3. Cumulative (left) and annual (right) capital costs for public LDV and MHDV charging from 2025 to 2040, in $ millions

Our analysis does not specify where these investments will come from. Governments at all levels will continue to play a major role in funding public charging infrastructure; for example, the Quebec government recently committed $514 million to add 116,700 chargers to the province’s public network.Footnote 6 Given the scale of investments required, however, public funds will increasingly need to leverage additional private investments; for example, the federal government’s Zero-Emissions Vehicle Investment Program (ZEVIP) provides contributions of up to 50% of capital costs. An earlier iteration, the Electric Vehicle and Alternative Fuel Infrastructure Deployment Initiative (EVAFIDI), leveraged $2 of private capital for every $1 of government funding.Footnote 7 Private sector actors, including automakers and charging providers, are also planning major investments in Canada’s public charging network, in particular DC fast charging in urban areas and along key travel corridors.Footnote 8

4. While most charging infrastructure is concentrated in urban regions and the largest provinces, programs must also consider how to provide equitable coverage across Canada, in particular for rural and remote communities.

We find that community public charging (i.e., located in population centres) represents more than half of future LDV charging needs, with around one-third for workplace charging (which in our model is a mix of public and private). Charging along highway and road corridors and in rural/remote regions represents a relatively small share of total ports (1-2%), although this type of charging is essential to ensure network connectivity and reduce range anxiety among EV owners. A recent federal audit found that “many areas of the country still lacked access to public charging stations … including rural, remote, and Indigenous communities and lower-income areas.”Footnote 9 Future network expansion plans should address these gaps in coverage to ensure equitable access to charging for all residents, and provide reliable charging along travel corridors in remote regions to reduce range anxiety.

For long-haul trucks, the need for a connected highway charging network is even more critical, as gaps in one province could reduce the uptake of EVs in other provinces. A recent study from the US found that long-haul HDV infrastructure can be concentrated along a few “no regrets” corridors, covering just 3% of the national highway freight network.Footnote 10 This suggests that a strategic approach to target highway MHDV charging investments may help achieve adoption targets at lower cost.

We found that four provinces (Ontario, Quebec, British Columbia, and Alberta) dominate overall future charging needs for both LDVs and MHDVs, accounting for 84% of public LDV ports and 92% of MHDV ports in 2040. However, all regions will need to rapidly grow their public networks from the current baseline to meet near-term milestones. We also explored charging needs in three major urban regions – Toronto, Montreal and Vancouver – finding that in addition to significant public charging needs (for example, the Toronto region alone will be home to more public charging ports (167,000) in 2040 than any province other than Ontario), more than 1.6 million EV-ready retrofits will be needed to enable residents in apartments and condos to charge at home.

5. The growing demand for EV charging will require upgrades and investments in electricity grids across Canada.

EV charging presents a significant additional load on electricity grids, adding to both energy and capacity needs. In speaking to utilities and system operators for this project, we heard that in many cases they are already planning for significant demand growth from electrification of transportation and other end uses (e.g., home heating). Utility representatives also told us how important it is to have federal targets and regulations (e.g., the EV Availability Standard and ZEV sales targets) to provide critical certainty and enable them to plan and invest in a future electricity system that is both larger and emissions-free.

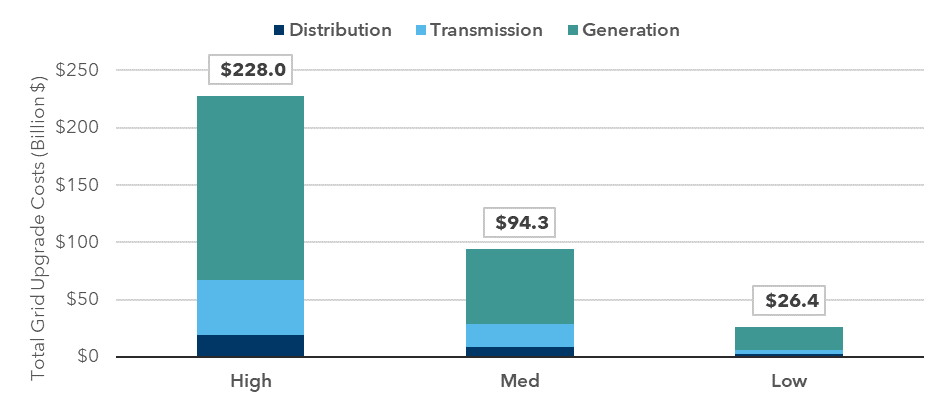

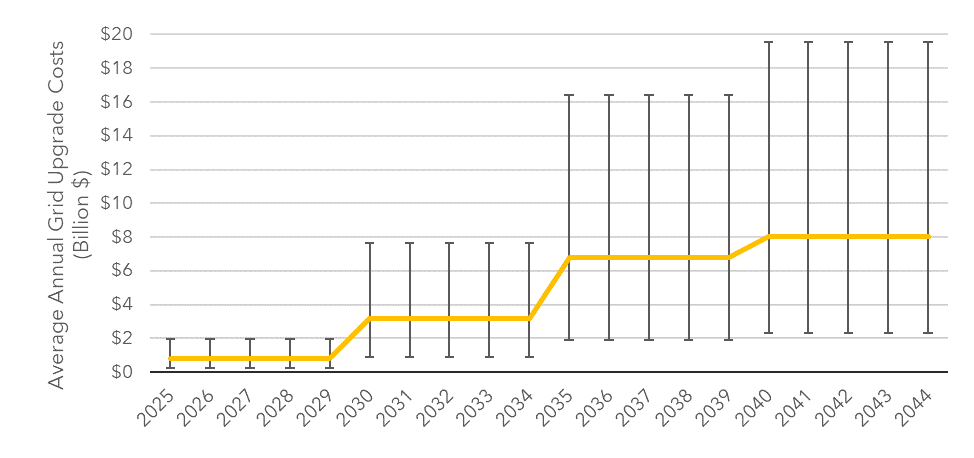

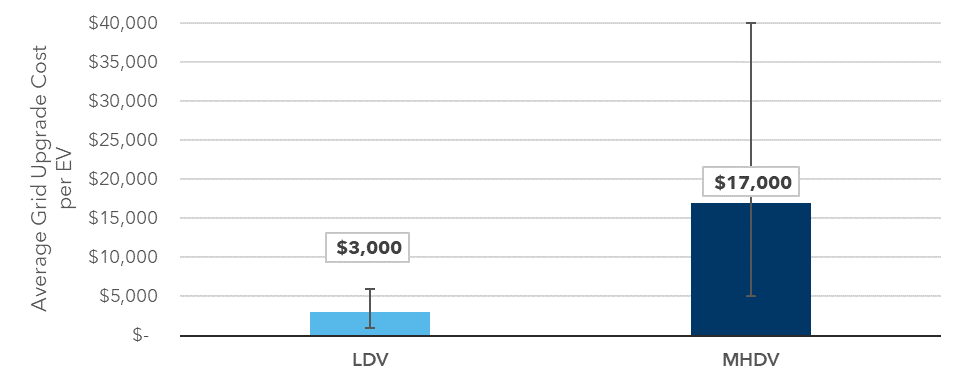

We estimate that LDV and MHDV charging could add up to approximately 4,300 MW of demand in 2030, growing to 22,500 MW in 2040. Our estimate of grid upgrades required to meet EV demand—including generation, transmission and distribution—ranges from $26 billion to 294 billion (mid-range: $94 billion) over the 2025 to 2040 period, reflecting the significant uncertainty around the magnitude of costs, as well as regional variations. On a per-vehicle basis this works out to $3,000 per LDV and $17,000 per MHDV. To put this cost into further context, Canadians spent approximately $70 billion on gasoline in 2022; in a future where the vehicle fleet is increasingly electric, we expect to see greater revenues for electric utilities which can use this to finance necessary grid upgrades.

Since EV charging is a flexible load, our results incorporate management mechanisms to shift the timing of charging from peak to off-peak periods. Actual charging patterns will depend on several factors which are difficult to forecast; however, other studies have shown significant potential for EVs to provide grid services acting as distributed energy resources (DERs), such as behind-the-meter battery storage. Managed EV charging is one of the most cost-effective measures to reduce peak electricity demand.Footnote 11 If utilities and provincial governments implement such strategies at scale, they could further reduce the overall demands on the grid and the need for costly generation, transmission and distribution upgrades, beyond what is forecast by our results.

6. The overall need for public charging—and associated investments—can be reduced through public policy interventions.

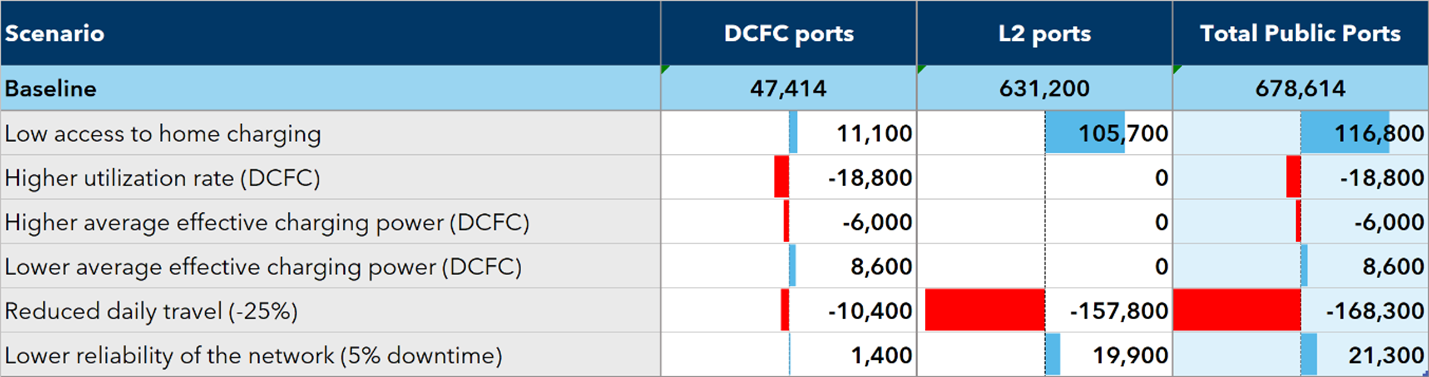

We developed several alternative scenarios to explore what different EV charging futures could look like (Figure ES 4). Under a scenario where Canadians drive 25% fewer kilometres, the number of public LDV ports required is 58,000 lower in 2030 and 168,000 lower in 2040. In scenarios where effective charging power and utilization rates are higher, the number of public ports could fall by another 25,000. A 25% decrease in driving distance would require significant investments in alternative modes of transport—including public transit, cycling and walking—as well as changes to urban planning and design to encourage less car-oriented communities.

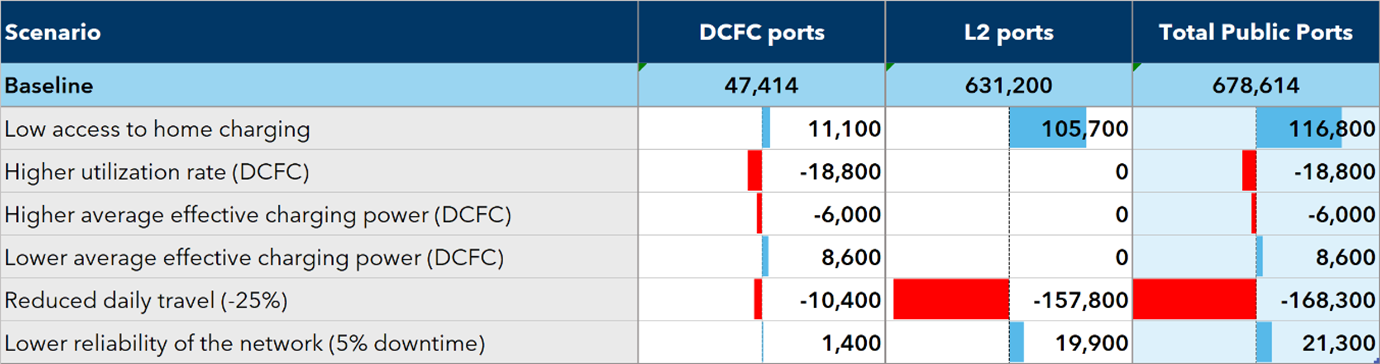

Text Version

| Scenario | DCFC ports | L2 ports | Total Public Ports |

|---|---|---|---|

| Baseline | 47,414 | 631,200 | 678,614 |

| Low access to home charging | 11,100 | 105,700 | 116,800 |

| Higher utilization rate (DCFC) | -18,800 | 0 | -18,800 |

| Higher average effective charging power (DCFC) | -6,000 | 0 | -6,000 |

| Lower average effective charging power (DCFC) | 8,600 | 0 | 8,600 |

| Reduced daily travel (-25%) | -10,400 | -157,800 | -168,300 |

| Lower reliability of the network (5% downtime) | 1,400 | 19,900 | 21,300 |

An alternate future pathway in which multifamily buildings have less access to charging, public networks are less reliable, and charging power is lower, could result in a need for 153,000 (+23%) more public ports across Canada than the baseline (Figure ES 5). Under this pathway, public charging networks would need to be overbuilt to compensate for lower reliability, and more public charging would be required to compensate for the slower pace of MFU EV-ready retrofits. Avoiding this scenario would require policy interventions to update regulations and standards (e.g., model building and/or electrical codes) as well as financial and other incentives to support EV-ready retrofits.

Figure ES 5. Selected alternative future LDV charging pathways (High, Baseline or Low charging pathways)

Exploring such alternate scenarios, as Figure ES 5 illustrates, is useful to help understand how future policy changes, technology shifts and market trends could impact the demand for EV charging infrastructure and to understand the degree of uncertainty associated with the results. This study provides an assessment of charging needs at both national and regional levels that can provide direction to program administrators, policymakers, communities, companies and landowners in continuing and accelerating EV charging deployment. The results should be regularly updated with on-the-ground utilization data, learnings from user experience, and market shifts. It will be up to governments at all levels, along with other public and private sector EV stakeholders, to further build on this work by developing more targeted plans and strategies to guide future investment and deployment decisions.

Table of Contents

- Executive Summary

- Table of Contents

- 1. Introduction

- 2. Light-Duty Vehicle Charging Needs

- 3. Medium- and Heavy-Duty Vehicle (MHDV) Charging Needs

- 4. Regional Findings

- 5. Grid Impacts Assessment

- 6. Conclusion

- Appendix A. Literature Reviewed

- Appendix B. Supplemental Information on LDV Charging Needs

- Appendix C. Supplemental Information on MHDV Charging Needs

- Appendix D. Supplemental Information on Regional Infrastructure Needs

- Appendix E. Supplemental Information on Grid Impacts

Chapter one

1. Introduction

1.1 Background

In support of its legislated goal of net zero emissions by 2050, the Government of Canada has introduced policies and targets to decarbonize the transportation sector, which is responsible for 22% of national greenhouse gas emissions.Footnote 12 Increasing the adoption of zero-emission vehicles (ZEV) is a key component of this goal. The federal government has published regulations (the Electric Vehicle Availability Standard) to require ZEVs to make up a growing share of new light-duty vehicle (LDV) sales, rising from 20% in 2026 to 60% by 2030 and 100% by 2035.Footnote 13 For the medium- and heavy-duty vehicle (MHDV) segment, the federal government has set targets for 35% of total sales to be ZEVs by 2030, reaching 100% by 2040 (where feasible). It is currently developing regulations to establish these targets in law (with interim sales requirements that would vary for different MHDV categories based on feasibility).Footnote 14

Achieving these targets will require coordinated action from all levels of government, as well as the automotive industry, utilities, and other private sector stakeholders. A key component is ensuring sufficient electric vehicle (EV) charging infrastructure to support the anticipated uptake of EVs across the country. Through Natural Resources Canada (NRCan) and the Canada Infrastructure Bank (CIB), the federal government has provided funding to support the installation of thousands of EV charging stations across Canada since 2016.Footnote 15 The federal Emissions Reduction Plan for 2030 sets a target of adding 50,000 new ZEV charging stations to Canada’s network, and commits $400 million of additional funding to support this goal.Footnote 16 This is in addition to the Canada Infrastructure Bank’s $500 million (ZEV) Charging and Hydrogen Refuelling Infrastructure Initiative (CHRI).Footnote 17

It is critical that policymakers and funders have a detailed understanding of how and where EV charging infrastructure needs to be deployed to meet anticipated demand. Accordingly, Natural Resources Canada commissioned Dunsky Energy + Climate Advisors (Dunsky) to develop an EV charging needs assessment for Canada, with support from the International Council on Clean Transportation (ICCT), building on previous studies in 2018 and 2022. This study expands the scope of previous work, which assessed Canada-wide EV charging needs, to include:

- Charging needs for medium- and heavy-duty vehicles (MHDVs).

- Regional differences and needs regarding the amount and type of charging infrastructure required over time.

- Potential electric grid impacts and investments required to accept new charging infrastructure.

The results are intended to support the Government of Canada—as well as provincial and municipal governments, utilities, and other stakeholders—in planning to ensure that sufficient charging infrastructure will be deployed to support Canada’s targets.

1.2 Structure of the report

Section 1 describes the background and general research approach taken for this study, comparing it to Dunsky’s 2022 charging needs assessment.

In Section 2, we focus on light-duty vehicles (LDV) requirements for residential and public/community charging infrastructure. This includes a description of Canadian and provincial EV sales forecasts from now to 2040, our high-level methodology, inputs and assumptions, and combined Canada-wide results showing the number of charging ports by type and location as well as energy requirements, EV/port ratios, and capital costs. We also summarize the results from our sensitivity analysis for LDVs.

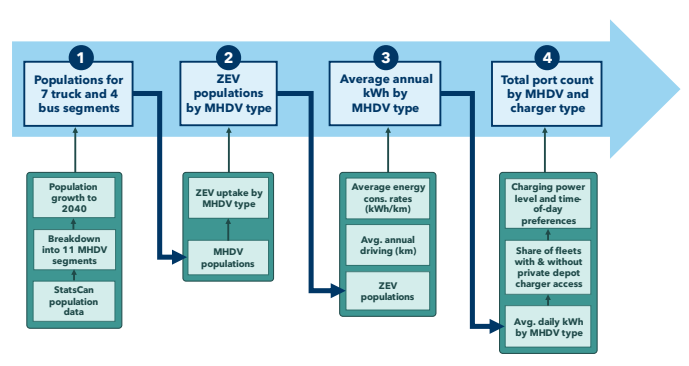

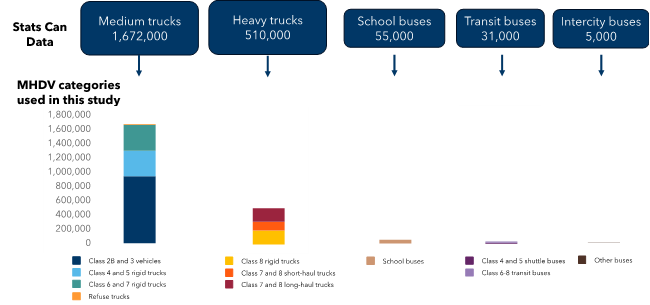

In Section 3, we describe the methodology used to determine MHDV charging infrastructure needs to 2040. This includes our estimate and assumptions for MHDV stock growth to 2040, expected energy demand from EV growth, the number of sites and charging ports needed to meet this demand across Canada, and the associated capital costs.

In Section 4, we present our EV charging port count and capital cost results by region, with results for each province and territory as well as the three census metropolitan areas (CMAs) with highest EV uptake.

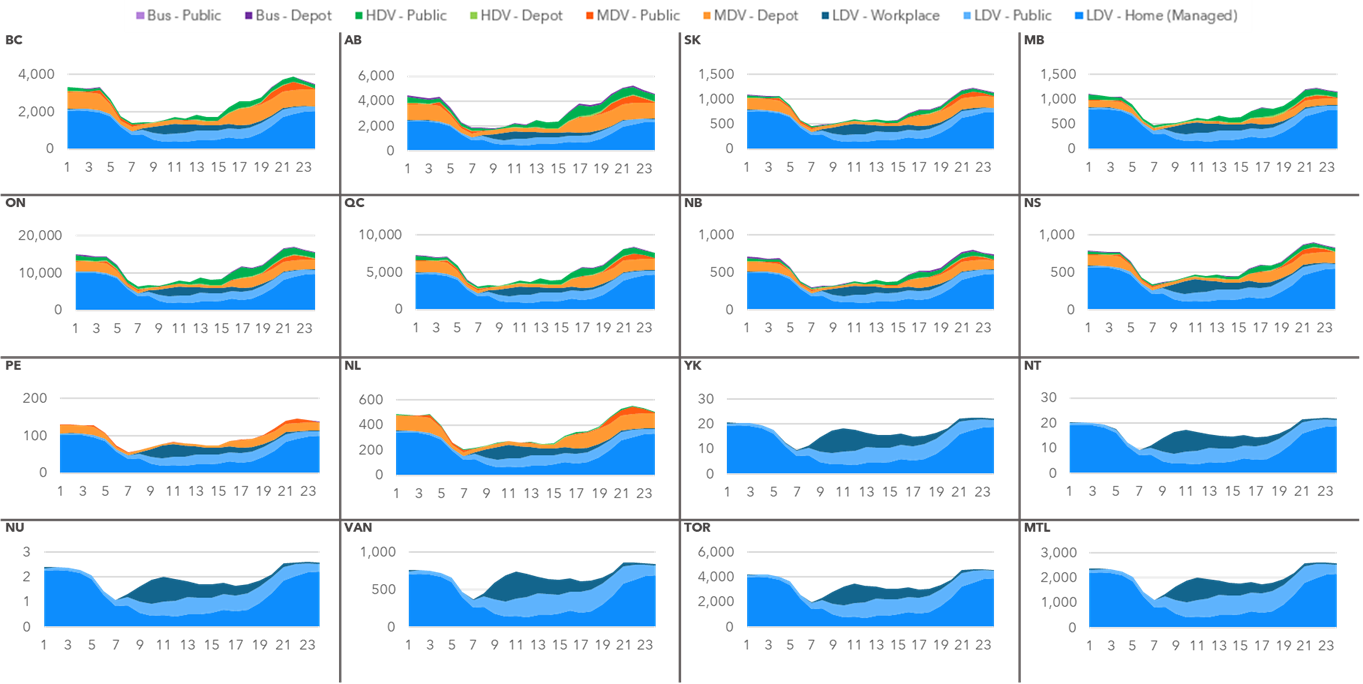

In Section 5, we assess the impacts of EV adoption and charging needs on Canada’s electricity systems for both LDVs and MHDVs. This section includes regional findings for growth in peak demand to 2040, and an assessment of the upgrades and investments required to prepare for future EV-related electricity demand growth.

Finally in Section 6, we summarize the results and discuss some of the key findings and their implications for Canada and the federal government as it develops policies and programs to support the rollout of EV charging infrastructure across the country.

1.3 Concepts and Definitions

To ensure consistency, the following definitions will be used throughout the report:

- Electric Vehicle (EV): An EV is a vehicle that uses one or more electric motors for propulsion with onboard energy storage that is recharged by plugging it into an external source of electric power. For the purposes of this report, light-duty EVs have a weight rating of 4,535 kg or less. EVs include:

- Battery Electric Vehicle (BEV): A BEV is a type of EV that only uses electric motors and the energy stored in its rechargeable battery packs. It does not use an internal combustion engine (ICE).

- Plug-in Hybrid Electric Vehicle (PHEV): A PHEV is a type of EV that includes both electric motors and an ICE. Its battery can be recharged by plugging it into an external source of electric power.

- Charging Port:Footnote 18 An EV charging port is the outlet used to charge the EV. The port can be located at a charging site and is categorized as a “permanent installation” if hard-wired. Although not always technically correct, the term “charger” is often used to refer to a charging port for simplicity’s sake. Charging ports are also sometimes referred to as Electric Vehicle Supply Equipment (EVSE). Charging ports include:

- Direct Current Fast Charger (DCFC): A type of charging port that allows for faster charging of the EV. With current technology, drivers can typically charge 80% of their battery in 30 minutes.

- Level 2 (L2) Charger: A type of charging port that can provide power at 240 volts and up to 30 amps. Drivers can typically add 15 to 40 km of range in one hour of charging.

- Charging Site: An EV charging site is an infrastructure location where electric energy can be supplied to recharge EVs. A charging site can have multiple charging ports that are permanent installations.Footnote 19

- EV ready: means parking spaces that feature an adjacent energized electrical outlet at which Level 2 charging can be installed in the future. A comprehensive EV-ready retrofit prepares nearly 100% of parking spaces to be EV ready.

- Public charging: charging ports on public or private land that can be used by any EV driver. This type of charging is typically visible through data accessible online.

- Includes charging along highways, in communities, and at certain workplaces offering public charging (to all, not just employees).

- Private charging: charging ports located on private land and providing charging services to a restricted number of EV drivers determined by the charging station operator.

- Includes charging provided to employees (and not the general public) at the workplace, charging at the depot, and charging at home.

- Workplace charging: charging ports used primarily by employees while they are working. Workplace charging may be public (i.e., accessible by anyone regardless of whether they work nearby; public charging in commercial areas operates in this manner) or private (i.e. located on private lands and accessible only by employees). In our modelling, we consider that workplace charging is 50% public and 50% private.

- Shared commercial charging: This type of charging is shared among fleets but is exclusively dedicated to commercial vehicles. It is placed in strategic locations for fleets like taxi stands and downtown delivery zones.

- Multifamily units (MFU): We used the Canadian Census Structural Dwelling Type (Table 98-10-0138-01) to categorize dwellings into single-family units (SFU) or MFU. We consider row houses and apartments of any height to be to MFU based on the following common characteristics: apartments in multifamily building feature shared parking areas, either in parking structures or surface parking. It is more challenging for multifamily building residents to install EV charging in these building types, even when they do have access to a parking spot, due to legal, financial, technical and logistical barriers inherent in both condominiums and rental apartments. The rationale for this approach is to differentiate between building types where charging infrastructure installation will be relatively straightforward, and those where government or other support is likely to be needed due to building type, tenure, or both. This does not necessarily map onto program definitions for multifamily buildings as they exist today.

- Single family units (SFU): We used the Canadian Census Structural Dwelling Type (Table 98-10-0138-01) to categorize dwellings into SFU or MFU. We consider single-detached, semi-detached, and duplexes to be SFU. People living in single family units (single family homes, duplexes, triplexes and row houses) are more likely to have access to, and ownership of, a parking space attached to their living space (e.g. a private garage or parking pad). Installation of EV charging in these settings can be relatively simple, although panel and/or service upgrades or other electrical works are sometimes required and implementing appropriate EV energy management systems in these building types can be complicated.

1.4 Study Background and Approach

The study took two broad approaches to understanding EV charging needs, costs, and grid impacts across Canada: fact-finding and data gathering through a review of existing literature and stakeholder interviews, and modelling and analysis.

1.4.1 Information Gathering

We reviewed academic and grey literature to ensure our methodology was grounded in current best practices and based on the latest data. Appendix A includes a list of sources reviewed and incorporated into our analysis. We also reviewed EV charging commitments made by the automotive industry in Canada to understand how these relate to government targets.

We conducted stakeholder interviews in spring and summer 2023 to incorporate input from a wide range of stakeholders in the LDV, MHDV and utility sectors to better understand Canada’s charging infrastructure needs and approaches to quantifying them. This included 14 utilities across nine provinces, who were able to provide (1) quantitative information related to grid capacity, expected impacts from EV adoption, and likely costs; and (2) their overall perspective of the feasibility of supporting the transition towards EVs. We also conducted interviews with other key stakeholders (Table 1) who were able to provide useful data (e.g., province-specific highway traffic data and/or vehicle registration data, targets and forecasts and utilization rate of the ports).

We identified data availability gaps that could limit our ability to forecast EV adoption, EV charging needs and grid impacts. To mitigate this risk, we leveraged alternate data sources to fill gaps, using professional judgement as needed to adapt data sets. This included such steps as taking province-wide ratios of BEVs and PHEVs to assess PHEV sales by region in cases where PHEV registration data has been lumped in with conventional hybrids. We also used our stakeholder interviews and industry context to fill jurisdiction-specific data gaps based on local knowledge (e.g., necessary geographic coverage and identifying key travel corridors.)

| Stakeholder | Number interviewed | Notes |

|---|---|---|

| Utilities | 14 | Across nine provinces |

| Provincial and Territorial governments | 6 | Additional PTs were engaged informally |

| Industry groups and associations | 11 | Includes associations representing Canadian LDV and MHDV sectors |

| International experts | 4 | Included experts in the US, Germany and China |

1.4.2 Modelling and Analysis

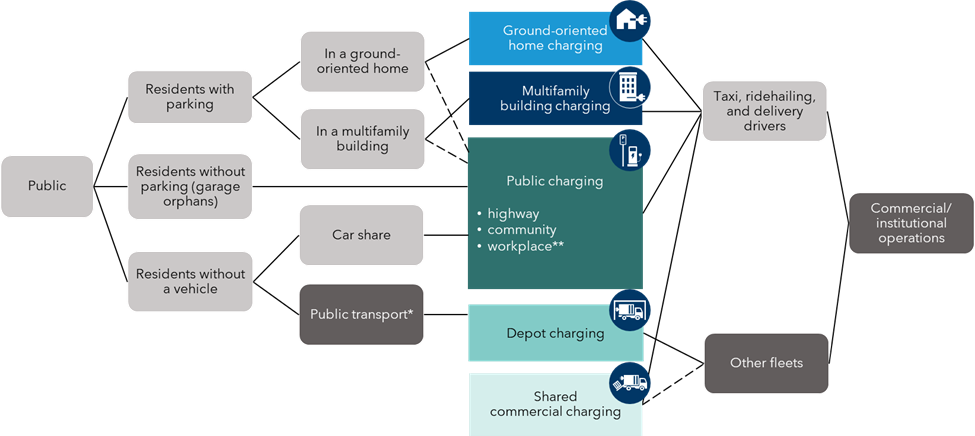

EV charging users include the public (residents, workers, and tourists) and fleet operators. Each of these user groups has different needs related to how, when, and how much they charge; as a result, they each use different combinations of charging locations, as shown in Figure 1.

* Public transport fleets occasionally use on-the-go/overhead charging, but this practice is not yet widespread.

** We consider workplace charging to be a form of both public and private charging; some is accessible only to employees (private) while other “workplace” charging is at charging sites that are open to the public. This analysis assumes that 50% of workplace charging is public and 50% is private.

Figure 1. Charging users and the charging categories that meet their needs

This study’s primary focus is on understanding infrastructure needs for public charging and shared commercial charging. However, to understand the amount of public and shared commercial charging required, and to assess the overall grid impacts of EVs, we also had to understand the potential levels of home charging access and deployment in depots. To understand this interdependency, we conducted scenario analysis on levels of home charging access (more details in Section 2).

We performed in-house modeling to establish the EV charging requirements for each region to meet federal ZEV sales targets for LDVs and MHDVs. In addition to the 13 provinces and territories, we conducted more granular analysis at the three largest Census Metropolitan Areas (CMAs) in Canada (Toronto, Montreal and Vancouver). The provincial numbers reported below include the results for the three CMAs.

Given the significant differences in charging use cases and needs between LDVs and MHDVs, we assessed these two sectors separately with tailored approaches. We provide more detail on the specific methodologies used in the LDV and MHDV sections below.

Estimating EV charging needs is an emerging practice. There is consensus in the literature and practice around certain aspects: for example, separately analyzing needs along corridors and in communities. As for more detailed aspects of the methodology (for example, setting the right balance of public DCFC and Level 2 charging infrastructure), there are not yet norms or standards — each region has different needs, urban form, and behaviours. Finding the right balance will involve making careful policy choices rather than finding the one clear path forward. Our aim in this study was to integrate emerging best practices with a tailored approach, based on local contexts and input from key stakeholders.

Our overall results present total charging infrastructure needs by type in each region by scenario, including estimated deployment costs and high-level grid impacts (qualitative issues raised by interviewees and high-level estimates of grid upgrade costs). We also present the results in terms of the effective ratio of EVs per charging port which allows us to compare our results with findings in other studies/jurisdictions.

1.4.2.1 LDV Charging Scenarios

We established two scenarios for the LDV charging needs assessment (Table 2) that are each based on the same EV adoption trajectories provided by Transport Canada (see Section 2.1).

The high scenario, which is considered the base case, assumes ambitious, Canada-wide action to support EV ready housing, wherein:

- A policy change, likely at the federal level, occurs that requires all new housing (including multifamily buildings) to be EV ready starting in 2030. This policy could be enacted through the federal Building Code, Electrical Code, or provincial/municipal codes covering a majority of Canada’s population; our analysis is non-prescriptive about the specific policy mechanism(s). Quebec has announced its intent to adopt such a policy at the provincial level, while several municipalities in BC and Ontario have these rules in place.

- Widespread investment in retrofits that provides charging in 30% of parking spaces in the existing residential stock by 2030 and 60% by 2035.

The low home charging access scenario assumes that current and announced policy measures remain in place, but that no additional policy measures are adopted to spur retrofits and new construction of EV ready housing. This scenario therefore results in higher public charging needs.Footnote 20

| Policy area | Criteria | Low Home Charging Scenario | High Home Charging Access (Base Case) |

|---|---|---|---|

| New construction | % new single-family units with EV ready parking | Quebec: 100% (regulations in place) | Quebec: 100% (regulations in place) |

| Everywhere else: 95% | Everywhere else: 95% | ||

| % new multi-family units with comprehensive EV ready parking | Vancouver CMA: 80%. Rest of BC: 40% | Federal policy change effective 2030 and applies to 100% of new units | |

| Toronto CMA: 50% | |||

| Quebec (incl. Montreal CMA): 100% starting in 2024 | |||

| Everywhere else: 0% | |||

| Retrofits of existing multifamily buildings | % of 2021 stock that undergoes comprehensive EV ready retrofits | BC, Vancouver CMA: 10% by 2030, no change after 2030 | Everywhere: 30% by 2030, 60% by 2035 |

| Everywhere else: 0% |

1.4.2.2 MHDV Charging Scenarios

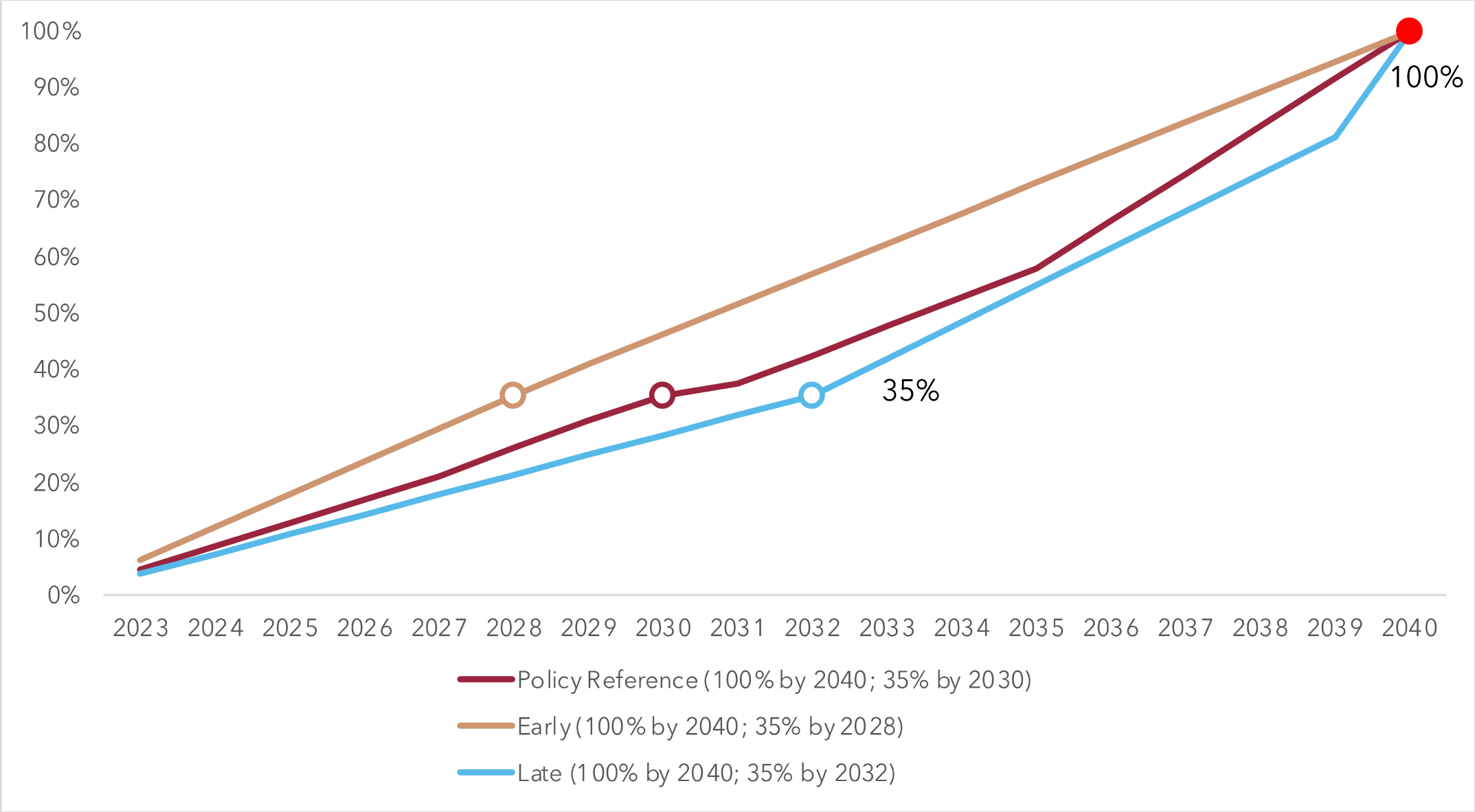

We consider three scenarios for the MHDV charging needs assessment. All three scenarios meet the target of 100% ZEV sales by 2040, but the alternate scenarios show different trajectories to get there, as shown in Table 3. The pace at which the zero-emission MHDV market develop will significantly impact the needs for supporting infrastructure in the short term. We further assume that all MHDVs will be battery-electric vehicles (BEVs), due to a higher degree of technology maturity and a better economic performance in all MHDV segments.Footnote 21 We also perform a sensitivity analysis to assess the extent to which charging needs for BEVs would be reduced if hydrogen-powered vehicles were to see a significant market uptake as a result of lower hydrogen prices.

| Year that ZEVs make up 35% of all MHDV sales | Year that ZEVs make up 100% of all MHDV sales | |

|---|---|---|

| Base Case | 2030 | 2040 |

| Early Case | 2028 | 2040 |

| Late Case | 2032 | 2040 |

1.4.2.3 Updates to previous Dunsky Charging Infrastructure Needs Projections

In our previous study, conducted in 2021, we estimated the Canada-wide EV charging needs (on corridors and in communities) for light-duty vehicles to 2050, based on optimal ratios of EVs to chargers for both L2 and DCFC charging infrastructure.Footnote 22 This study presented two scenarios: high and low home charging access for EV owners in multifamily buildings. We present the results from the 2021 study in Section 2.4.1, in a comparison with the updated results from this study.

For this 2024 study we updated both the scope and methodology to provide a more granular understanding of Canada’s EV charging infrastructure needs, and to reflect evolving best practices and information when it comes to forecasting future infrastructure needs.

The main scope updates for the current study are:

- Added assessment of MHDV charging needs.

- Provided province/region-specific estimates of infrastructure needs and impacts.

- Assessed grid readiness and costs associated EV charging infrastructure.

- Adjusted the study horizon to 2040 (as opposed to 2050 in the 2021 study).

We also made several updates to our previous methodology and assumptions for LDV charging needs. Most notably, we based our infrastructure needs forecast on an estimate of regional energy demand (in kWh) for different vehicle and charger types and expected charger utilization, instead of the previous approach that used an assumption of optimal EV-to-charger ratios to estimate the numbers of chargers for a given vehicle stock. This bottom-up approach helped us develop a more accurate understanding of how EV charging needs vary by province and region, and provided the input data needed for the grid impacts assessment.

We also extended our analysis to include additional charging use cases, such as shared commercial vehicles (taxis, ride-hailing fleets), depot charging, tourism needs, and additional coverage of rural and remote communities. Other modeling changes include an updated Transport Canada LDV EV sales forecast resulting in more EVs on the roads in 2040; a higher ratio of BEVs to PHEVs; and updated assumptions on effective charging power, utilization rate, and infrastructure costs. See the following sections for a more detailed description of our methodology. A more detailed comparison of the assumptions for the two studies can be found in Appendix B.

Chapter two

2. Light-Duty Vehicle Charging Needs

Light-duty vehicles (LDV) are responsible for approximately 50% of Canada’s transportation sector GHG emissions, and 12% of national emissions across all sectors. Transport Canada defines LDVs as cars, sports utility vehicles, or light trucks with a Gross Vehicle Weight Rating of 4,535 kg or below.

2.1 EV Adoption Forecast

The first step in our analysis was to establish forecasts of EV sales for Canada and for each province or territory. We based our forecast on Canada’s announced ZEV sales targets and the December 2023 ZEV Availability Standard, which would require a ZEV sales share of at least 60% of new vehicles by 2030 and 100% by 2035 nationwide. We began with Transport Canada’s internal forecast, which is updated annually and distributes EV sales across provinces and territories based on historical adoption trends and is aligned with the Availability Standard.

We also accounted for provincial requirements by updating Transport Canada’s forecast to align with recently updated provincial ZEV mandates in British Columbia and Quebec (Table 4). For all other provinces, we used the Transport Canada forecast. This resulted in a slightly higher total ZEV stock than would be required to meet Canada’s federal targets.

| 2026 | 2030 | 2035 | |

|---|---|---|---|

| Canada | 20% | 60% | 100% |

| BC | 26% | 90% | 100% |

| Quebec | - | 2 million EVs in circulation | 100% |

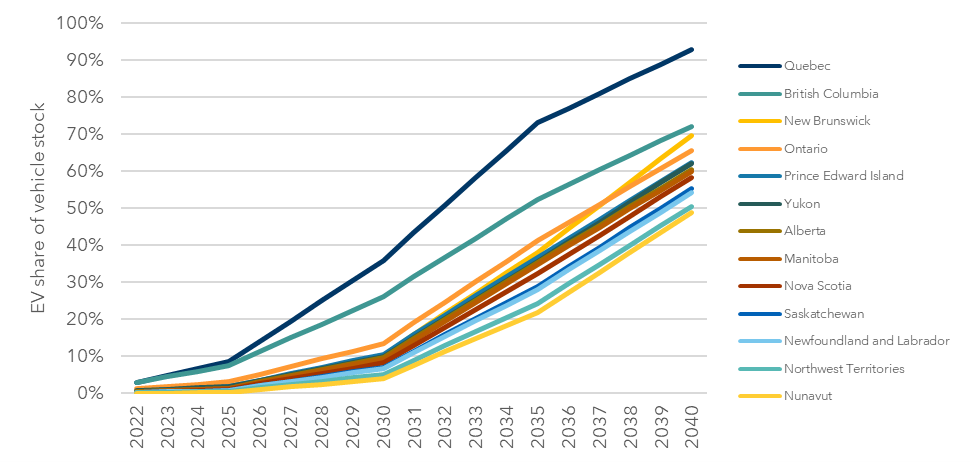

Figure 2 shows the forecast of EVs as a share of total LDV stock by province and territory between 2022 and 2040.

Figure 2. Electric vehicles as a share of the total light duty vehicle stock by province and territory, 2022-2040

2.2 Residential Charging

Key inputs and assumptions to residential charging demand forecasts

- Population forecasts: We used Statistics Canada forecasts for Canada, Provinces and Territories.Footnote 23

- Census Metropolitan Area (CMA): Private parking access varies between 50% (duplex) and 85% (single or semi-detached, apartment).

- Non-CMA: Private parking access assumed to vary between 75% (duplex) and 95% (single or semi-detached house, apartments).

- Charger types: We assume 10% of light-duty BEVs and 25% of PHEVs use L1 at home; the remainder use L2.

- Charging access in existing multifamily buildings is assumed to be 1%.

- In 2023, less than 1% of EV owners live in multifamily buildings. Single family unit owners are more likely to purchase an EV until 2040, by which point all residents are equally likely to own an EV regardless of housing type.

- Sensitivity analysis: We compared residential charging under “High” and “Low” home charging access scenarios.

Although our primary objective was to forecast public and shared commercial private charging needs, we needed to first understand the presence of residential charging to understand the magnitude of public charging required.

Charging at home (whether in single family homes or in multifamily buildings) plays the largest role in the charging ecosystem in terms of the number of ports and the overall amount of energy dispensed at those locations, and this is expected to continue in the future. Indeed, a customer survey by Hydro Quebec showed that residents with access to home charging do 90% of their charging at home in that province.Footnote 24 Similarly, a survey of EV owners in the U.S. found that 90% charge at home daily or weekly.Footnote 25

Additional housing stock classifications and assumptions are presented in Appendix B.

2.2.1 Multifamily Buildings

Multifamily building residents often face higher barriers to EV charging than residents in ground-oriented dwellings (although these residents can also face barriers, e.g., access to on-street parking only). While one-third of Canadians live in multifamily buildings, only 12% of EV owners do, according to a 2022 survey.Footnote 26 This disparity is even greater in cities like Metro Vancouver where, as of 2021, 43% of residents live in apartments; this share is expected to rise.Footnote 27 Retrofits in multifamily buildings allow people living in apartments or condos to have access to residential charging.Footnote 28 Without such access, owners of EVs in multifamily buildings must rely on public or workplace charging.

Furthermore, not all multifamily housing offers parking; indeed, while most post-war developments until recently do include at least one parking space per unit, municipalities are increasingly reducing or eliminate parking minimums in new developments to help encourage more sustainable travel modes. Multifamily housing without parking can never be made EV ready. Our model includes estimates of the share of existing and future housing units that will offer no parking. Appendix B provides our parking and charging access assumptions.

While there is no data on EV ready parking spaces that are currently EV ready, we estimate that there are under 50,000 EV ready multifamily parking spaces today in Canada. Our base scenario (high home charging access) sets a course where: (1) all new residential buildings are required to be EV ready starting in 2030 and, (2) comprehensive EV ready retrofits are conducted on 30% and 60% of the 2021 residential building stock by 2030 and 2035, respectively. Our analysis found that under this scenario, an average of 87 to 88% of all households live in EV ready units (meaning they have the ability to install a charger without further upgrades) across the time period from 2025 to 2040—effectively, the policy package to improve home charging access keeps pace with a shift towards greater EV adoption among residents of multifamily buildings. Under this scenario, 2.1 million multifamily units will have EV ready parking by 2030, 4.3 million by 2035 and 4.7 million by 2040 (Table 5).

Under our alternate low home charging access scenario, we find that the share of EV owners living in EV ready units falls from 88% in 2025 to 82% in 2040, with variation between provinces depending on housing type and mix. In other words, policies do not keep pace with EV adoption, and an increasing number of EV users rely exclusively on public charging over time. The number of EV ready retrofits in multifamily buildings, which is driven only by programs that exist or have been announced today, reaches approximately 81,000 in 2030, with no further growth in retrofits after 2030. The pre-2030 trend is driven by BC, where there is a growing movement towards EV ready building policies and a greater push towards retrofitting multifamily buildings.

| MFU parking spaces that are EV ready | Scenario | 2030 | 2035 | 2040 |

|---|---|---|---|---|

| From retrofits | High (base) | 1.6 million | 3.2 million | 3.2 million |

| Low | 81,000 | 81,000 | 81,000 | |

| From new construction | High (base) | 590,000 | 1.0 million | 1.5 million |

| Low | 390,000 | 560,000 | 700,000 | |

| Total | High (base) | 2.1 million | 4.3 million | 4.7 million |

| Low | 480,000 | 640,000 | 790,000 | |

| % of all MFU that is EV ready | High (base) | 29% | 52% | 54% |

| Low | 7% | 10% | 12% | |

| % of all housing (SFU and MFU) that is EV ready | High (base) | 87% | 88% | 87% |

| Low | 85% | 82% | 79% |

2.3 Public Charging

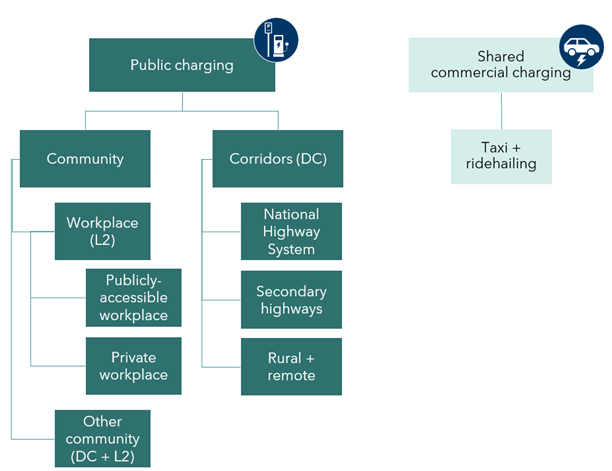

Our analysis split public EV charging into three categories (Figure 3):

- Community charging: Level 2 and DCFC stations in communities of various sizes, including workplaces, public parking lots, and curbside charging.

- Corridor charging: DCFC stations along major highway and road corridors, as well as in remote and rural communities to maximize geographical coverage.

- Shared commercial charging: ultra-fast charging stations accessible only to commercial fleets (e.g., taxis and ride hailing), either on public or private lands.

The textbox presents the main inputs and assumptions for public charging. For more details, see Appendix B.

Figure 3. Public LDV charging includes community, corridors, and shared commercial charging infrastructure.

Key inputs and assumptions to public and shared commercial charging demand forecasts

- NRCan’s Electric Charging and Alternative Fuelling Stations Locator was used to develop a baseline estimate of public charging.

- People with home charging access use public charging 15% of the time, while people without home charging use it 100% of the time.

- 50% of workplace charging is public charging (i.e. at charging sites that anyone can access), while 50% of workplace charging access is restricted and is private charging (i.e. accessible only to employees at that location). We followed the approach of NREL in setting this assumption.Footnote 29

- Vehicles travelling on highway trips longer than 160 km use corridor charging.

- The number and type of public charging ports is based on the average energy use of BEVs and PHEVs, which is a function of average vehicle efficiency (data from NREL and ICCT), average annual driving distances (provincial/territorial data), charging preferences (share of charging at home, at work, public) and port utilization rates (based on utilization data in advanced EV markets).

- We use the average effective charging power of port types, which is a more realistic number than the nameplate charging power. However, both are correlated. Port charging power increases over time in line with technology forecasts. See Appendix B for details.

- We use an average charging port utilization rate based on a review of actual utilization data from charging network operators and professional judgement. See Appendix B for details.

- We assume a 97-98% reliability factor over the study period, meaning that public charging ports are in operation for 97-98% of the timeFootnote 30. This means that the network will be “overdesigned” by 2-3% relative to demand (i.e., more ports than would otherwise be needed if the network was 100% reliable). This assumption is based on the 97% reliability requirement embedded in the US National Electric Vehicle Infrastructure (NEVI) program; most charging networks in Canada today have not reached this level of reliability but we expect improvements over time. In Section 2.6 we explore the impact on results if reliability is lower. See details in Appendix B.

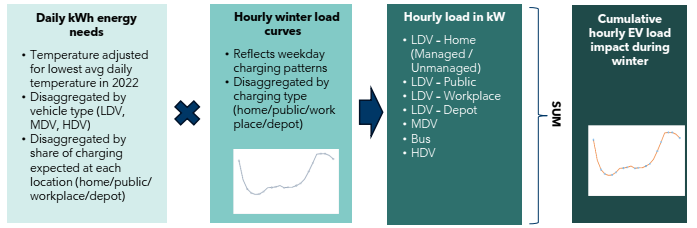

- We calculated the average annual historical (2013-2022) temperature data (provincial/territorial) using Weather Canada’s average monthly temperatures. We used this to estimate total daily EV energy needs, using the relationship between EV electricity consumption and ambient temperature (e.g., EVs consume 16% more energy at 0°C than at 8°C).

- For our corridor assessment along the National Highway System (NHS) and other secondary highways, we assumed that 100% of charging would be provided by DCFC (due to their faster charge times versus L2), and there would be a charging station at least every 65 km. We assumed that only trips over 160 km would require charging.

- To expand the geographical coverage of our corridor assessment, we also assessed the DCFC needs in rural and remote communities that were located outside of our geographical buffers. More details can be found in Section 2.3.2.

2.3.1 Community Charging Needs

Community charging infrastructure is needed to support EV charging for day-to-day needs, and for people without access to private charging, in cities, towns and other population centres. Community charging includes workplaces, curbside, and publicly accessible parking lots. Access to these types of charging is crucial to enabling EV adoption, especially for people without access to home charging. Diversified charging infrastructure, incorporating both fast- and slower-charging infrastructure, will allow EV owners to select the optimal charging methods for their individual needs. Community charging consists of public DCFC (i.e., fast charging) and Level 2 ports (which are located at workplaces, on-street and off-street parking).

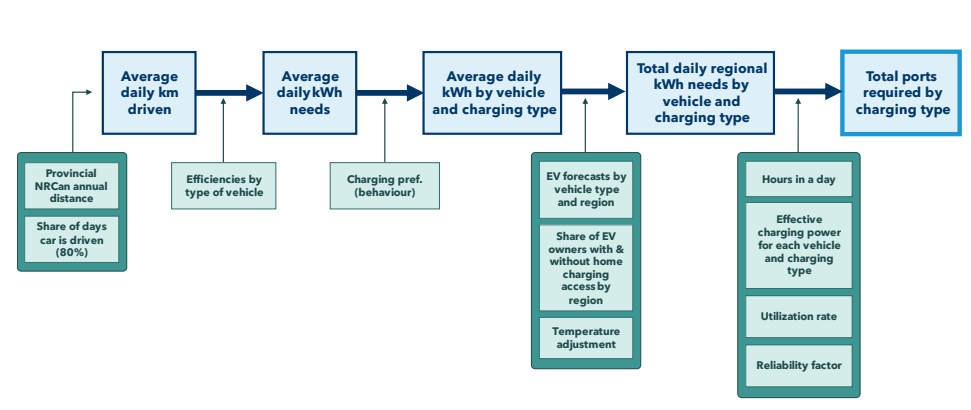

Our general methodology for estimating community public charging needs is as follows (Figure 4):

- We estimated average daily driving distances (vehicle-kilometres travelled, or VKT) as a product of annual average driving distances in each province and the share of days a vehicle is driven (80%).Footnote 31

- We then developed an average daily energy use (in kWh) based on average VKT and vehicle efficiency (which varies by vehicle type).

- We estimated the average daily energy use (kWh) by vehicle and charging type, using behavioural insights on charging preferences (from NREL).

- Finally, we developed or estimate of total daily regional energy needs (by vehicle and charging type), as a factor of daily energy use, EV uptake forecasts (by region and vehicle type), and the share of EV owners with/without home charging access (by region). We used a temperature adjustment to factor in regional climatic variations and how that might impact vehicle and charging use/efficiencies.

- The final step was to estimate the total number of ports required by charging type (L2 and DCFC). This is based on the total daily regional energy needs, adjusted for several key factors: effective charging power for each vehicle and charging type; port utilization rate; reliability factor; and the number of hours in a day.

Figure 4. Methodology to estimate total daily energy demand from light-duty vehicles (LDVs)

2.3.2 Corridor Charging Needs

A key component of the LDV analysis was understanding needs for fast charging infrastructure along transportation corridors. The National Highway System (NHS) includes 38,000 km of highways across Canada, with additional provincial and secondary highways adding to this total. Highway corridor charging is assumed to exclusively use DCFC due to their faster charging times relative to L2 chargers. As a result, energy needs are higher for corridor stations. We separated highway corridor charging from community DCFC charging for this analysis as highway systems often cut across provinces or regions, and as such their expansion benefits from a coordinated planning approach by federal and/or provincial governments.

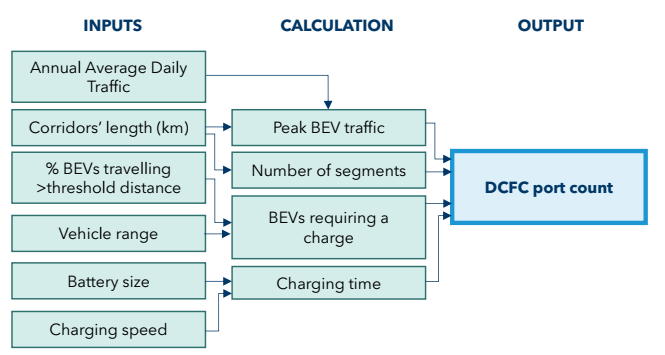

To understand corridor charging needs we took the following steps:

- Identified the highways to be included as charging corridors. To ensure the proposed coverage met the needs of travellers within each province, we used the National Highway System (NHS) as a starting point (all core, feeder, and northern/remote routes), and supplemented this with secondary and provincially significant highways not covered by the NHS, based on input received from provincial and rural community stakeholders.Footnote 32,Footnote 33 A list of all the secondary highways and their length, by region, considered in this analysis can be found in Appendix B.

- Calculated the number of stations required, assuming that there would be one DCFC station every 65 km on all highway types (in accordance with best practices in CanadaFootnote 34). Also, a minimum of 2 ports per station was assumed for the NHS network and a minimum of 1 port per station for the secondary highways until 2035, after which it also increased to 2 ports per station. This allows the infrastructure to be build out gradually on the secondary highways.

- Assessed BEV travel volumes over time based on average annual daily traffic (AADT), adjusted to represent peak volumes, which is the more important parameter when estimating EV charging needs.Footnote 35 If the regional AADT data was unavailable, the vehicle-kilometres-travelled (VKT) data was utilized to estimate peak traffic volumes along the NHS corridors.Footnote 36 We estimated future peak BEV volumes based on our adjusted TC forecasts for EV penetration by region. (Note that the analysis only includes BEVs as PHEVs do not use fast charging).

- Assessed climatic or geographic impacts (i.e., cold weather, significant elevation change) on energy demands.

- Assessed charging needs as a function of travel volume and the share of trips requiring a charge (e.g., we excluded trips that are short enough to accomplish with one full charge, which we consider to be less than 160 km).

- Calculated charging time as a function of average charging power levels (kW) and battery capacity (kWh).

Figure 5 outlines the approach we used to estimate the number of DCFC ports required across the main highway corridors in each region.

Figure 5. Methodology for Estimating DCFC Port Count Along NHS Corridors

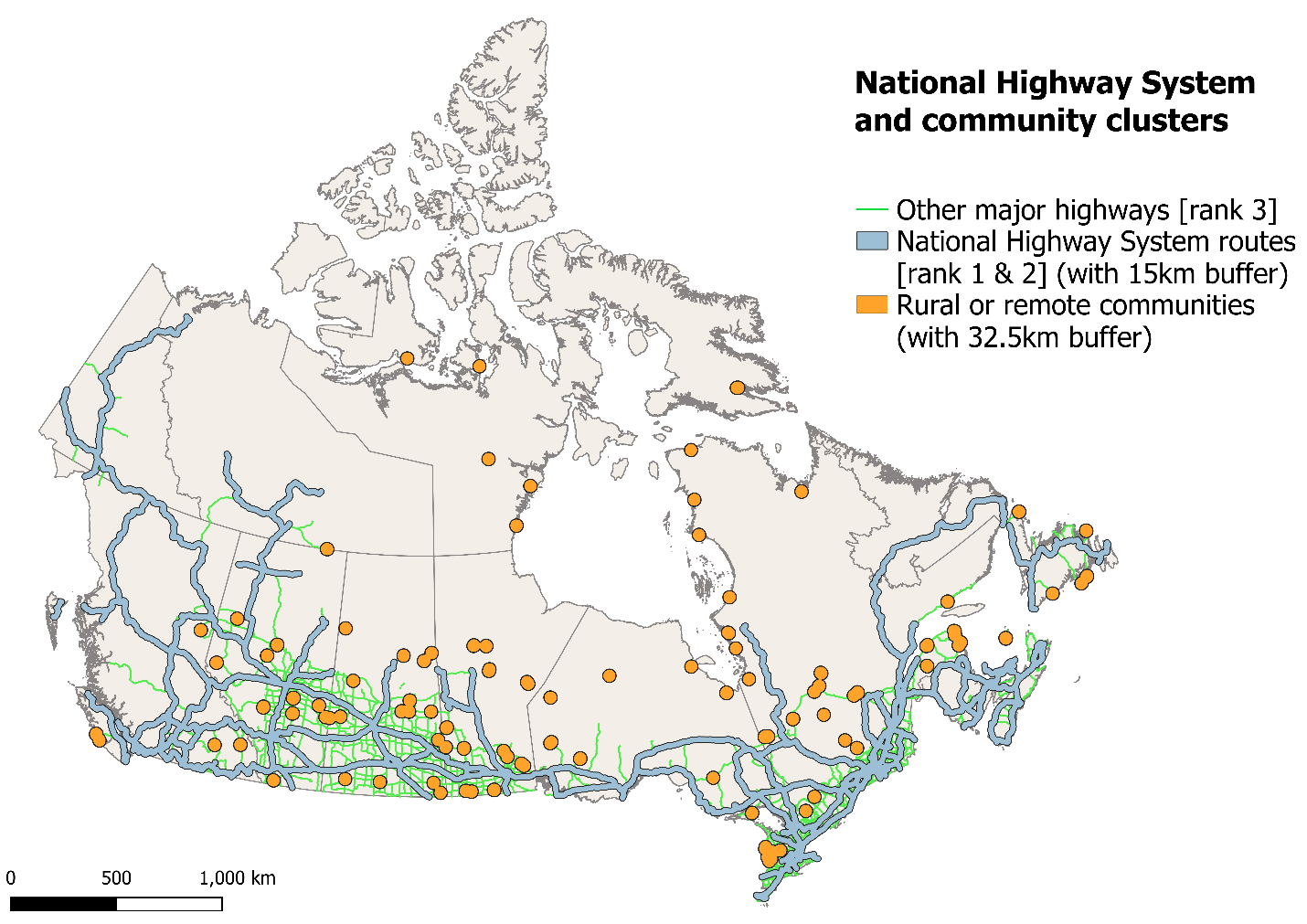

Rural and Remote Communities

We performed additional analysis to ensure that rural and remote communities, particularly in Canada’s north, received adequate geographical coverage creating an effective DCFC network. First, we identified all population clusters greater than 1,000 residents that are further than 32.5 km from the National Highway System. Footnote 37 We then allocated two DCFC ports for each of these communities. The map below (Figure 6) shows the distribution of these rural and remote communities.

Figure 6. Map of Canada showing rural and remote community clusters with fast charging needs

2.3.3 Tourism Charging Needs

In addition to our analyses above we developed a model to account for the specific needs of some communities that receive very high peak traffic from tourism. The impact of tourism on highway corridors was already accounted for in the hourly peak AADT values analyzed for each province, as it quantifies the tourism on road as well. However, additional analysis was required to account for tourism impact on DCFC and L2 community charging, especially in certain regions with higher levels of tourism. Based on the visitor volume data available by each provincial and territorial government, the daily average number of tourist vehicles in 2019 was calculated, with an assumption of 2.5 tourists per vehicle and similar ratio of EV-to-LDV as the provincial numbers. This was supplemented to the previously calculated EV fleet size to factor the impact of tourism on community charging needs.

2.3.4 Shared Commercial Vehicles: Taxis and Ride-Sharing Services

The business case for building charging infrastructure can be particularly challenging if overall utilization of the infrastructure is low — a challenge many site hosts face in the near term as EVs still represent a relatively small portion of the overall vehicle stock, and potentially even into the longer term depending on improvements to charging access at home. This challenge is exacerbated by the fact that most personal EV owners do most of their charging at home.

Charging infrastructure specifically targeting shared fleets can result in much higher utilization rates due to (1) their higher annual mileage than personal vehicles and (2) their higher dependence on DCFC infrastructure. Because of their long daily commutes, taxis and commercial ride-sharing services (such as Uber) also present an excellent opportunity for electrification and being early adopters.

Most shared fleet segments prefer DCFCs over L2 charging. Electric taxis, ride-hailing, and vanpool vehicles are looking for a fast way to top up and one-way car share vehicles would ideally have staff charge them up quickly before bringing them back to an ideal location. This need for fast top-ups supports the rationale of providing dedicated ports for shared fleets. It is important to design charging infrastructure for this type of EV owner because they need very fast charging (DCFC of at least 250 kW) strategically located along the route, and because drivers don’t always have access to residential charging.

To estimate fast-charging infrastructure needs for taxis and ride-sharing services, we took the following steps:

- Quantified the number of vehicles using publicly available fleet estimates from key markets, including the City of Toronto and the province of Quebec. These were then scaled across provinces relative to labour force numbers from Statistics Canada on the share of people employed as taxi or limousine drivers. Our assumptions for taxi and ride-hailing fleet size are presented in Table 35, Appendix B.

- Forecasted the fleet growth to 2040 using a fleet compound annual growth rate of 1% to the 2023 baseline.

- We followed the same approach to estimate vehicle energy needs as the community charging analysis (Figure 4).

- We assumed that 100% of taxis and on average 20% of ride-sharing drivers are driving full time.Footnote 38 Across all drivers, we use an implicit assumption of an average of 81.5% of home charging access for taxis and ride-sharing drivers.

Our results for shared commercial charging needs are presented as part of our public and home charging results. In our results, we outline specific number of ports estimated for taxis and ride-sharing services.

2.4 Combined Results

Figure 7 shows the growth in public charging ports (DCFC and L2) relative to EV adoption to 2040 under our base scenario (high home charging), showing that the need for public ports grows in step with EV adoption, but that the ratio of public ports to EVs becomes more efficient over time. Table 6 shows the combined results for Canada-wide LDV charging infrastructure needs between 2025 and 2040. Assuming a federal ZEV sales regulation is implemented as planned, Canada would need approximately 447,000 public ports by 2035, rising to 679,000 by 2040. Of this total, around 9 in 10 are expected to be Level 2 chargers in communities and publicly accessible workplace parking areas. The remainder are DCFC installed in communities, along highway corridors, and for use by taxis and other shared commercial vehicles.

The number of private ports (in homes and workplaces) is significantly larger than the number of public ports, reaching 11.9 million in 2035 and 18.5 million in 2040, due to the reliance on home charging (and to a lesser extent, private workplace charging) among Canadian vehicle owners. The share of EV ready multifamily buildings will need to increase substantially to meet these numbers, as discussed in Section 2.2.1.

Figure 7. Public charging needs (L2 and DCFC) and EV growth to 2040 under base case (high home charging)

| Scenario | Type of port | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|---|

| High access to home charging (base case) | DCFC - community | 6,200 | 18,900 | 31,400 | 41,700 |

| DCFC - corridor + rural | 1,600 | 1,900 | 3,100 | 3,900 | |

| DCFC - taxis + rideshare | 1,200 | 1,200 | 1,800 | 1,800 | |

| Total - DCFC | 9,000 | 22,000 | 36,300 | 47,400 | |

| L2 - community | 58,200 | 132,900 | 255,000 | 385,300 | |

| L2 - workplace | 33,300 | 79,600 | 155,500 | 245,900 | |

| Total - L2 | 91,500 | 212,500 | 410,500 | 631,200 | |

| Total – Public ports | 100,500 | 234,500 | 446,800 | 678,600 | |

| L1 - home | 141,100 | 588,500 | 1,470,900 | 2,207,300 | |

| L2 - home | 828,100 | 3,718,600 | 10,250,500 | 16,065,900 | |

| L2 - work | 33,300 | 79,600 | 155,500 | 245,900 | |

| Total Private | 1,002,500 | 4,386,700 | 11,876,900 | 18,519,100 | |

| Low access to home charging | DCFC - community | 6,300 | 20,200 | 37,800 | 52,800 |

| DCFC - corridor + rural | 1,600 | 1,900 | 3,100 | 3,900 | |

| DCFC - taxis + rideshare | 1,200 | 1,200 | 1,800 | 1,800 | |

| Total - DCFC | 9,100 | 23,300 | 42,700 | 58,500 | |

| L2 - community | 58,400 | 135,500 | 270,900 | 418,700 | |

| L2 - workplace | 33,500 | 84,500 | 188,300 | 318,300 | |

| Total - L2 | 91,900 | 220,000 | 459,200 | 737,000 | |

| Total – Public ports | 101,000 | 243,300 | 501,900 | 795,500 | |

| L1 - home | 140,600 | 571,800 | 1,358,200 | 1,983,200 | |

| L2 - home | 825,300 | 3,614,400 | 9,458,300 | 14,404,400 | |

| L2 - work | 33,500 | 84,500 | 188,300 | 318,300 | |

| Total Private | 999,400 | 4,270,700 | 11,004,800 | 16,705,900 |

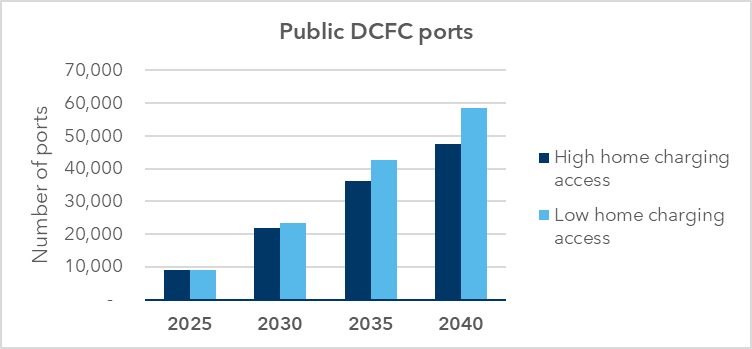

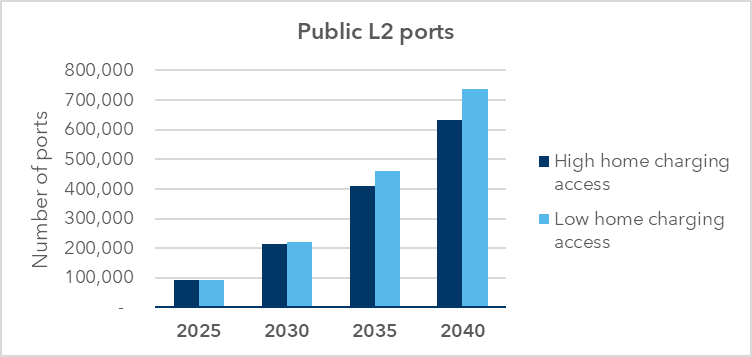

Figure 8 and Figure 9 compare public charging needs for DCFC and L2 ports, respectively, between the high and low home charging scenarios. These show that lower home charging access leads to higher demand for public charging due to a greater need for public charging access by those without parking and/or charging at home. As a result, the low home charging access scenario results in a need for an additional 8,800 public ports in 2030, 55,100 in 2035, and 116,900 in 2040.

Table 7 shows the EV-to-port ratios associated with these outputs. By 2030, if Canada acts to ensure home charging access for multifamily building residents (see Section 2.2.1), Canada should target having roughly one public port (L2 and DCFC) for every 21 EVs on the road. The ratios broken down by type of charging range from 170 BEV/DCFC ports to 17 EV/public and private workplace L2, reflecting the differences in charging power and expected utilization between these different port types. Our forecast shows that, over time, the ratio of EVs to ports grows as the network is built out, EV ownership increases, and charging power and charger utilization increase over time. The total number of EVs/ports including all private charging remains fairly constant over the study period at slightly less than one-to-one.

Figure 8. Assessed needs for public DCFC ports under both home charging access scenarios (2025-2040)

Figure 9. Assessed needs for public L2 ports under both home charging access scenarios (2025-2040)

| Scenario | EV-to-Port-Ratios | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|---|

| High home charging access (base case) | BEV / DCFC ports | 85 | 170 | 303 | 379 |

| EV / L2 port (community + public and private workplace) | 9 | 17 | 24 | 24 | |

| EV / public L2 ports (community + public workplace) | 12 | 23 | 32 | 33 | |

| EV / public ports | 11 | 21 | 30 | 31 | |

| EV / total ports (including residential) | 1.0 | 1.1 | 1.1 | 1.1 | |

| Low home charging access | BEV / DCFC ports | 84 | 161 | 257 | 307 |

| EV / L2 port (community + public and private workplace) | 9 | 16 | 21 | 20 | |

| EV / public L2 ports (community + public workplace) | 12 | 23 | 29 | 28 | |

| EV / public ports | 11 | 20 | 27 | 26 | |

| EV / total ports (including residential) | 1.0 | 1.1 | 1.2 | 1.2 |

2.4.1 Comparison with Dunsky’s 2021 Assessment

Table 8 shows the key results of Dunsky’s previous assessment, conducted in 2021, compared with the updated results from this 2024 study (using the high home charging access scenario in both cases).Footnote 39 Due to updates in methodology and scope, the updated study forecasts a need for a higher number of public charging ports in the near term (2025 to 2030 period), resulting in a lower ratio of EVs to public ports for these years (i.e., more public ports needed for every EV on the road). The port counts and ratios converge between the studies in 2035 and 2040 as the network is built out.

Notably, our updated assessment calls for nearly twice the number of public DCFC and L2 ports in 2025 than previously. This difference in the near term is due to a more granular scope of analysis (we set a higher bar for geographical coverage, conducted a detailed assessment of provincial requirements, and ensured broader coverage along highway corridors and in remote/northern communities), integrating shared commercial vehicle charging needs, and more conservative assumptions around charger utilization and power levels.

| Study | Type of port | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|---|

| Current (2024 study) – Base scenario (High home charging access) | Public ports | 100,520 | 234,440 | 446,760 | 678,610 |

| L2 | 91,520 | 212,510 | 410,480 | 631,200 | |

| DCFC | 8,998 | 21,931 | 36,282 | 47,414 | |

| EV/Public Port ratio | 11 | 21 | 30 | 31 | |

| EV/L2 ratio | 9 | 17 | 24 | 24 | |

| BEV/DCFC ratio | 85 | 170 | 303 | 379 | |

| Previous (2021 study) – High home charging access scenario | Public ports | 52,000 | 195,000 | 442,000 | 643,000 |

| L2 | 48,000 | 181,000 | 410,000 | 593,000 | |

| DCFC | 4,300 | 13,800 | 32,000 | 50,200 | |

| EV/Public Port ratio | 20 | 24 | 28 | 32 | |

| EV/L2 ratio | 21 | 26 | 30 | 35 | |

| BEV/DCFC ratio | 180 | 250 | 300 | 330 | |

| Difference | Public ports | 48,520 (+93%) | 39,440 (+20%) | 4,760 (+1%) | 35,610 (+6%) |

| L2 | 43,520 | 31,510 | 480 | 38,200 | |

| DCFC | 4,698 | 8,131 | 4,282 | -2,786 | |

| EV/Public Port ratio | -9 (-45%) | -3 (-13%) | +2 (+7%) | -1 (-3%) | |

| EV/L2 ratio | -12 | -9 | -6 | -1 | |

| BEV/DCFC ratio | -95 | -80 | +3 | +49 |

Note: We present results from 2025 to 2040 to align with our current study period, although the 2021 study modelled EV charging needs to 2050.

2.4.2 Comparison with Other Studies and Jurisdictions

Table 9 compares our 2030 results to outputs from studies by two leading U.S. agencies: the National Renewable Energy Laboratory (NREL) and the California Energy Commission (CEC). Controlling for differences in assumptions (for example, the California study considers a scenario with much lower home charging access), the BEV-to-DCFC and EV-to-L2 port ratios are comparable with this study’s findings.

| Study | Juris-diction | Projection year | Market share (BEV/ PHEV) | Average charge power (kW) | Home charging access among EV owners | BEV/ DCFC | EV/ all public + workpl. L2 |

|---|---|---|---|---|---|---|---|

| Dunsky, 2023 (high home charging) | Canada | 2030 | 75/25 | 233 | 87% | 170 | 17 |

| NREL, 2023Footnote 40 | U.S. | 2030 | 90/10 | 150-350 | 90% | 1631 | 21 |

| CEC, 2023Footnote 41 | California | 2030 | 88/12 | 2902 | 66% | 160 | 10 |

Policymakers in the European Union have begun to use installed kilowatt-to-EV ratios rather than EV-to-port ratios to set policy and track progress. This approach has the benefit of controlling for differences in average port charging power that are often obfuscated by direct comparisons of EV-to-port ratios. Table 10 shows the required energy output for public EV charging infrastructure installed per all EVs on the road, according to this study. By 2030, our results show a need for 1.2 kW to 1.3 kW per EV.

| Scenario | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|

| High home charging (base case) | 1.7 | 1.2 | 1.0 | 1.0 |

| Low home charging | 1.7 | 1.3 | 1.2 | 1.3 |

| ZEV stock shares in % of all LDVs | 4.3% | 18% | 45% | 66% |

The European Union Alternative Fueling Infrastructure Regulation (EU AFIR) requires member states to ensure, at the end of each year, a public charging infrastructure total power output of at least 1.3 kW for each BEV and 0.8 kW for each PHEV registered in its territory.Footnote 42 The Regulation stipulates that states can target a lower power output once the share of ZEV in the territory reaches at least 15% of LDV stock, and does not prescribe this ratio, recognizing that charging provisions can become more efficient as the concentration of EVs increases.

We cannot directly compare the ratios in Table 10 with the AFIR requirements because the ratios in Table 10 are for all EVs, while the AFIR provides requirements on the basis of BEV and PHEV separately. To directly compare, we made the following calculation in Table 11:

Total kW required (AFIR) = 1.3 * nBEV+ 0.8 * nPHEV

This analysis shows that if public charging in Canada were built to meet this study’s high home charging access scenario (a lower public charging requirement than in the low home charging access scenario), the EU’s AFIR requirement would be exceeded, even in the years after the ZEV stock share is greater than 15%.

| Installed energy output (GW) | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|

| Total required in EU (AFIR) | 1.3 | 5.8 | 16.1 | 25.8 |

| Dunsky, 2023 total needs assessedFootnote 43 | 1.9 (>AFIR) | 6.2 (>AFIR) | 16.1 (=AFIR) | 26.2 (>AFIR) |

| ZEV stock as % of all LDVs | 4.3% | 18% | 45% | 66% |

2.5 LDV Charging Infrastructure Costs

2.5.1 Methodology

We developed per-port cost estimates using 2022 dollars and based on in-house total installation and equipment costs assessment. Our results include estimated costs for utility upgrades, installation and equipment, and include discussion on the level of uncertainty and variation associated with each. These cost estimates were informed by discussions with utilities, municipalities and governments to understand the total costs of installation plus charging equipment.

Importantly, the cost per port for the same type of infrastructure varies widely across projects, depending especially on:

- Charging power (Level 2 vs DCFC infrastructure, DCFC from 25 kW to 350 kW and beyond).

- The number of ports deployed per site (there are economies of scale with a greater number of ports per site, though larger sites might exceed available electrical capacity triggering more costly upgrades).

- The location (e.g., curbside charging is more expensive than in off-street locations).

- The quality of the design. The use of load management techniques including EV energy management systems, can significantly reduce per-port costs.

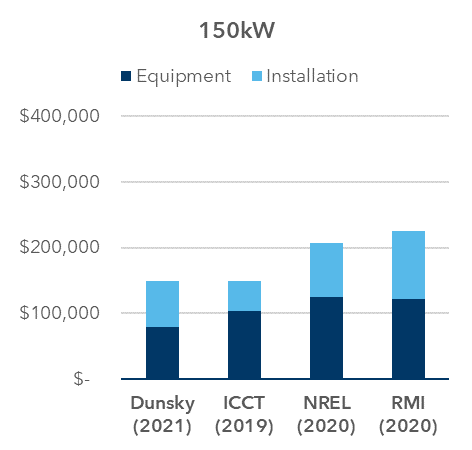

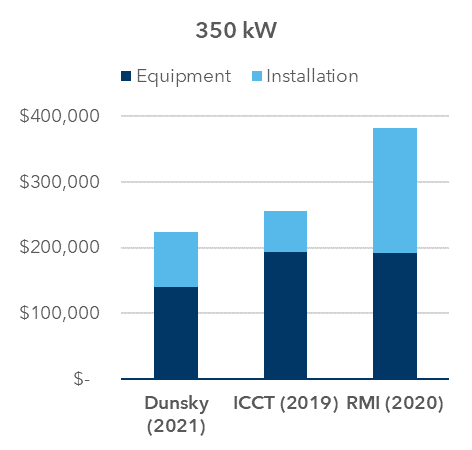

A number of studies have attempted to quantify per-port equipment and installation costs. One such study is a study that Dunsky conducted for NRCan in 2021, with the goal of advising NRCan as it contemplated shifting focus towards higher power levels for DCFC infrastructure. The figures below compare our own estimates with estimates made under previous studies by the International Council for Clean TransportationFootnote 44, the National Renewable Energy LabFootnote 45, and RMI.Footnote 46

Figure 10: Comparison of DCFC deployment cost estimates per port, various years

Multiple factors will influence how these capital costs change over time. An increase in these costs could be expected as labour and equipment costs increase over time. To counteract that increase, however, we expect that economies of scale will be realized from installing multiple ports in the same location, along with increased equipment supply and familiarity in the market among contractors, electricians, and designers. This could cause costs to decline from their current levels by 2030 and 2035. Indeed, a study from the International Council on Clean Transportation estimates that 150 kW DCFC costs will decrease by 3% in 2030 compared to 2021, even when including an increase in installation costs of 4% per year.Footnote 47 At the same time, a trend towards higher power output for DCFC infrastructure will ultimately lead to a long-term increase in per-port costs while the costs per kW nameplate capacity (values in parenthesis in Table 12) will decrease.

For Level 2 charging, on the other hand, we do not anticipate as significant an increase in charging power over time. Instead, we expect that the primary factors impacting L2 deployment costs will relate to where chargers are installed, including whether they are installed in on-street locations (where costs can easily exceed $20k per port) vs off-street parking lots, the number of ports deployed in a given location and associated economies of scale, and the degree to which installations may become more expensive over time if locations with simpler installations are targeted first.

| Type of Port | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|

| DCFC | $160,000 (125 kW average) |

$240,000 (175 kW average) |

$240,000 (250 kW average) |

$240,000 (300 kW average) |

| L2 | $15,000 | $10,000 | $10,000 | $10,000 |

Further studies on actual infrastructure deployment costs and key factors could help to further refine this analysis. Public organizations that fund charging infrastructure deployment are in an excellent position to report on actual costs from funded projects and help to refine our collective understanding of the likely costs of expanding on this infrastructure in the future.

2.5.2 Results

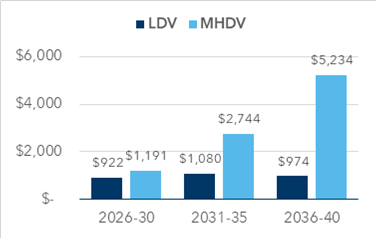

Our cost assessment in Table 13 shows that meeting public charging infrastructure needs for LDVs would cost $17.7 billion by 2040. Most of these costs come from the installation of fast-charging ports, even though they account for less than 10% of total public ports.

| Type of Port | 2025 | 2030 | 2035 | 2040 |

|---|---|---|---|---|

| DCFC | $1,500 | $5,300 | $8,700 | $11,400 |

| L2 | $1,400 | $2,100 | $4,100 | $6,300 |

| Total Public Cost | $2,900 | $7,400 | $12,800 | $17,700 |

2.6 Alternate Scenarios for LDV Charging Needs

We performed a sensitivity analysis to assess the impacts of varying key assumptions on the number of public ports needed for LDVs. This section presents the individual impacts of changing assumptions on number of ports and explores different alternate scenarios, illustrating the range of possibilities that may unfold in response to changing conditions in the EV charging ecosystem.

2.6.1 Sensitivity Analysis

We conducted a sensitivity analysis on five key modeling inputs:

- Access to home charging (see Table 2 for a detailed description).

- Utilization rate of DCFC ports.

- Effective charging power of DCFC ports.

- Daily vehicle kilometres travelled.

- Network reliability.

The scenarios and their descriptions are presented in Table 14, and Table 15 outlines the impact on the number of ports needed by 2040 for each individual scenario modelled. The results are presented relative to the base case (high home charging access).

| Scenario | Definition & Assumptions | Source |

|---|---|---|

| Base case | Baseline assumptions + high access to home charging (see Table 2). Assumptions: 1) Federal policy change (e.g. building/electrical code) happens in 2030 and applies everywhere (100% EV ready new MFU after 2030). 2) Retrofits: 30% of 2021 stock is EV ready by 2030, 60% by 2035. |

Dunsky analysis |

| Low access to home charging | Low home charging access, in MFUs especially. No or few additional efforts on building/electrical code and retrofits to increase home charging access. Assumptions: 1) EV ready for new construction only in regions where already announced (Quebec, BC, Toronto, Vancouver, Montreal). 2) 10% of BC-Vancouver 2021 stock retrofitted, 0% elsewhere. |

Dunsky analysis |

| Higher utilization rate of DCFC ports | Assumes utilization-oriented pathway (economically viable utilization rate of network for private sector). Assumptions: Roughly doubles utilization rate of network relative to baseline, reaching 20% by 2040, leading to a higher portion of “profitable” chargers but an increased likelihood of congestion and lineups for EV drivers: 11% (2025), 18% (2030) and 20% (2035-2040). |

"Average network utilization of 15% for DC fast charging, the rate currently observed by top-tier charge point operators in Europe." Footnote 48 |

| Higher effective charging power of DCFC ports | Assumes higher nameplate capacity of DCFC ports and higher voltage architecture for EV to accept higher capacity. Assumptions: Assumes average charging power of all DCFC ports installed in Canada 50kW higher than baseline:175 kW (2025), 225 kW (2030), 300 kW (2035) and 350kW (2040). |

Identified ±50 kW as interval around baseline assumptions based on various studies. Footnote 49 Footnote 50 |

| Lower effective charging power of DCFC ports | Assumes lower nameplate capacity of DCFC ports and business-as-usual voltage architecture development for EV. Assumptions: Assume average charging power of all DCFC ports installed in Canada of 50 kW lower than baseline (75 kW by 2025, 125 kW by 2030, 200 kW by 2035 and 250 kW by 2040). |

ICCT assumes 75 kW and 125 kW by 2025 and 2030 respectively in its 2030 analysis for USA.Footnote 51 |

| Reduced daily travel | Assumes citizens will reduce their daily travel through densification policies and increasing use of public transit. Assumption: All LDVs reduce daily travel distance by 25% relative to baseline. |

NREL uses a 25% lower daily travel distance in its sensitivity analysis.Footnote 52 |

| Lower reliability of the network | Assumes overall network uptime is reduced by 2-3% compared to baseline of 97%-98%. This likely still reflects an improvement over current Canada-wide reliability. Assumption: Assumes all ports are on average down for 18.25 days per year (95% reliability). |

Based on: “A report commissioned by Natural Resources Canada showed that, in January 2022, 6% of AC and 5% of DC chargers were offline while 7% and 11% of AC and DC (respectively) charging sessions failed, lasting less than 5 minutes”.Footnote 53 |

Table 15: Impacts of alternate scenarios on 2040 number of ports required for Canada relative to baseline

Text version - Table 15