Federal Flood Damage Estimation Guidelines for Buildings and Infrastructure

Version 1.0, 2021

Natural Resources Canada, General Information Product 124e

Natural Resources Canada, Public Safety Canada.

© His Majesty the King in Right of Canada, as represented by the Minister of Natural Resources, 2021.

For information regarding reproduction rights, contact Natural Resources Canada at copyright-droitdauteur@nrcan-rncan.gc.ca.

Table of Contents

- 1.0 Introduction and purpose

- 2.0 Note on terminology

- 3.0 General practices

- 4.0 Range of flood hazards and factors affecting damage

- 5.0 Types of flood damage

- 6.0 Tools for estimating damage

- 7.0 Stage-damage curves

- 8.0 Future adjustments and regional indexing

- 9.0 Case studies

- 10.0 References

- Appendix 1 – Breakdown of Flood Damage Calculation Steps

- Appendix 2 – Causes of Coastal Flooding

- Appendix 3 - Velocity Stage-Damage Curves for Buildings

- Appendix 4 – Damage Reductions Resulting from Contingency Measures

- Appendix 5 – Willingness-to-Pay Studies

- Appendix 6– Business Disruption and Residential Displacement Estimation Methods

- Appendix 7 – Costs Associated with Traffic Delays

- Appendix 8 – Flood Damage Assessment Tools

- Appendix 9 – Summary of Database Issues and Considerations

- Appendix 10 – Data Capture Forms – residential

- Appendix 11 – Data Capture Forms – non- residential

- Appendix 12 – Stage Damage Curves and Values - Residential*

- Appendix 13 – Stage Damage Curves and values - Non-Residential*

- Appendix 14 – Sample Content and Prices

- Appendix 15 – Review of Building Classification Schemes and Photographic Examples of Building Classes

- Appendix 16 – Residential Property External Damages

- Appendix 17 – Summary of Non- Residential Classes and Salvage of Contents

- Appendix 18 – Damages Suffered by Multi-Level Below-Grade Parkades

- Appendix 19 – Estimating Damages to Crops, Livestock, and Barns and Outbuildings

- Appendix 20 – Case study, damages to unique strutures: Stampede Park

- Appendix 21 – Uncertainty Associated with Structural Classification Schemes and Stage-Damage Curve Development

- Appendix 22 – Available Measures of Price and Spending Change

- Appendix 23 – Method for Updating Residential Content Damages Currency

List of abbreviations and acronyms

- AAD

- Average Annual Damages

- AEP

- Annual Exceedance Probability

- BCA

- Benefit-Cost Analysis

- BCP

- Business Continuity Planning

- BE

- Bare Earth

- CAD

- Canadian Dollars

- CBO

- Community Based Operations

- CEA

- Cost-Effectiveness Analysis

- CFDEP

- Comparative Flood Damage Estimation Program

- CME

- Contents Moved and Evacuated

- CPI

- Consumer Price Index

- CSVR

- Content to Structural Value Ratio

- DALY

- Disability Adjusted Life Years

- DEFRA

- Department for Environment Food and Rural Affairs

- DEM

- Digital Elevation Model

- EAD

- Expected Annual Damages

- EPA

- Environmental Protection Agency

- FDDBMS

- Flood Damage Database Management System

- FDO

- Flood Defence Operations

- FEMA

- Federal Emergency Management Agency

- FIA

- Federal Insurance Administration

- GDP

- Gross Domestic Product

- GIS

- Geographic Information System

- HAZUS-MH

- HAZUS Multi-Hazard

- HEC-FDA

- Hydrologic Engineering Center Flood Damage Reduction Analysis

- IPCC

- Intergovernmental Panel on Climate Change

- LiDAR

- Light Detection and Ranging

- LIRA

- Land and Infrastructure Resiliency Assessment

- MCA

- Multi-Criteria Analysis

- NDMP

- National Disaster Mitigation Program

- NOAA

- National Oceanic and Atmospheric Administration

- NRCan

- Natural Resources Canada

- PFDAT

- Provincial Flood Damage Assessment Tool

- QGIS

- Quantum GIS

- QRA

- Quantitative Risk Assessment

- RCP

- Representative Concentration Pathway

- RFDAM

- Rapid Flood Damage Assessment Model

- SHS

- Survey of Household Spending

- TBL

- Triple Bottom Line

- USACE

- U.S. Army Corps of Engineers

- USDA

- United States Department of Agriculture

- WCM

- Watercourse Capacity Maintenance

- WDR

- Warning Dependent Resistance

- WHO

- World Health Organization

- WTP

- Willingness To Pay

1.0 Introduction and purpose

This document is part of the Federal Flood Mapping Guidelines Series. These guidelines aim to provide advice to support the management of flood risks and their consequences to communities.

Since the late 1960s, a number of studies have been undertaken across the country and methodologies developed to assess flood damages within flood-affected communities, in order to quantify flood related damages, evaluate the cost-effectiveness of various flood mitigation projects and understand the vulnerability of people to flooding.

The following guidelines have been developed by the Government of Canada to establish a standardized approach for estimating damages to buildings and other infrastructure resulting from flooding and the development of flood stage-damage functions, incorporating international and national (provincial/ territorial/ regional) best practices where appropriate. Thus, this document, Federal Flood Damage Estimation Guidelines for Buildings and Infrastructure Version 1.0 is intended to provide a summary of the current practices used by qualified professionals in Canadian jurisdictions and to provide recommended practices for qualified professionals to estimate flood damage, primarily due to riverine flooding.

This document provides technical guidance and serves as a resource for engineers, scientists, insurers and municipal planners involved in flood damage estimation. In addition, this document describes a range of flooding hazards which can influence damages incurred as a result of flooding. The specific objectives of this document are to:

- Describe the range of flooding hazards and the factors affecting flood damage

- Describe different methods available for estimating damage resulting from flooding - primarily riverine

- Provide guidance on how to develop and use stage-damage curves as well as considerations on their use, accuracy and limitations

- Provide guidance for future adjustments and regional indexing of stage-damage curves

The scope of this document is limited to estimating damage, resulting from flooding, or prior to a flood event as part of a risk assessment. Refer to other documents in the series for guidance on other components of flood risk management in Canada.

2.0 Note on terminology

All Federal Flood Mapping Guidelines Series documents will apply the following definitions, based on the Emergency Management Framework for Canada (Ministers Responsible for Emergency Management, 2017) and NDMP (NDMP, 2021) literature. It is recognized that provinces and territories may define these terms differently, and these definitions are not intended to be prescriptive outside the context of the Federal Flood Mapping Guidelines Series documents.

Flooding: The temporary inundation by water of normally dry land.

Flood Mapping: The delineation of a flood on a base map. This typically takes the form of flood lines on a map that show the area that will be covered by water, or the elevation that water would reach during a specified flood event. The data shown on the maps, may also include flow velocities, depth, other risk parameters, and vulnerabilities.

Hazard: A potentially damaging physical event, phenomenon, or human activity that may cause the loss of life or injury, property damage, social and economic disruption, or environmental degradation.

Risk: The consequence of a specific hazard, expressed in terms of likelihood, and based on considerations of vulnerability and exposure.

Flood maps are used for several different purposes, including identifying hazards and risks, land use planning, emergency planning and response, and public awareness and communication. Under the broad definition of ‘flood map’, different types of geospatial, hydraulic, and hydrologic information can be presented to meet specific assessment requirements. For consistency, four main types of flood maps are defined here.

For the purposes of this document, the following definitions also apply:

Contents Damage: refers to damages to moveable contents within a structure

Depth-Damage Curve: see Stage-Damage

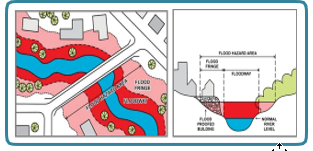

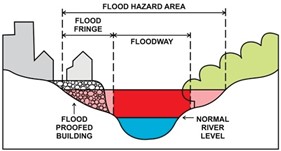

Design Flood: A specific flood magnitude that is used for delineating flood hazard areas.

Direct Damages: are those that occur immediately and can be directly attributed to flood inundation. Direct damages include damage to public infrastructure and private property.

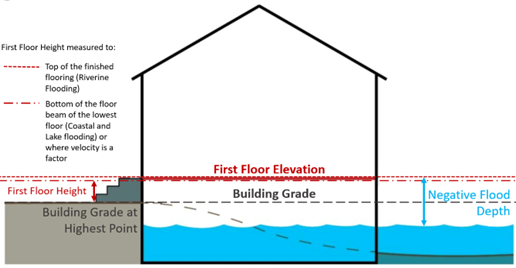

First Floor Height: height of first floor above grade (Figure 6)

Grade: the highest elevation of the property which can be established using a DEM derived from LiDAR, from ground level surveys, or detailed topographic maps (Figure 6)

Indirect Damages: occur as a result of direct flood impacts but they are more difficult to quantify, examples include: reduced economic activity, individual financial hardships, adverse impacts on the social well-being of a community, and disruptive impacts

Intangible Damages: damages that are more difficult to assess monetarily such as emotional stress, illness, or loss-of-life

Resilience: strategies that focus on reducing impacts from flooding through prevention and preparedness

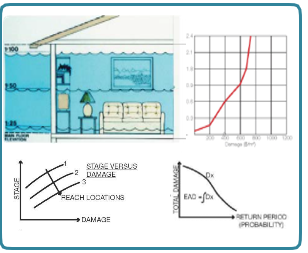

Stage-Damage: stage-damage and depth-damage are interchangeable terms which describe a one-dimensional mathematical relationship between the depth of water above or below the first floor of a building and the amount of damage that can be attributed due to that level of water (Figure 7). They typically represent the average damage of a group of buildings with similar properties due to flooding in a given community.

Empirical Stage-Damage vs Synthetic Stage-Damage: Empirical models use a data-driven approach, relying on actual damage datasets from past events in order to link building vulnerability to the record of damage data of the flood event. Synthetic curves are generated based on a conceptual approach and expert knowledge, hypothesizing and making assumptions about the potential damage, related to specific components of the building (McGrath et al. 2019).

Absolute vs Relative: absolute economic loss (in terms of currency) or relative loss (percentage of the estimated replacement value of property) of a buildings’ structure and contents. Most Canadian stage-damage curves are constructed using absolute value while in the U.S. the relative approach is most common.

Structure Damage: refers to damage to a building and the building components that are not taken when an individual moves, e.g.: furnace, hot-water heater, wall-to-wall carpeting. (IBI Group & Golder Associates, 2015)

Tangible Damages: damages to which a dollar value may be assigned.

Figure 6: Building measurements used in determining flood depth

Text version

Figure of a house showing the building measurements used in determining flood depth

(source: IBI Group, 2015)

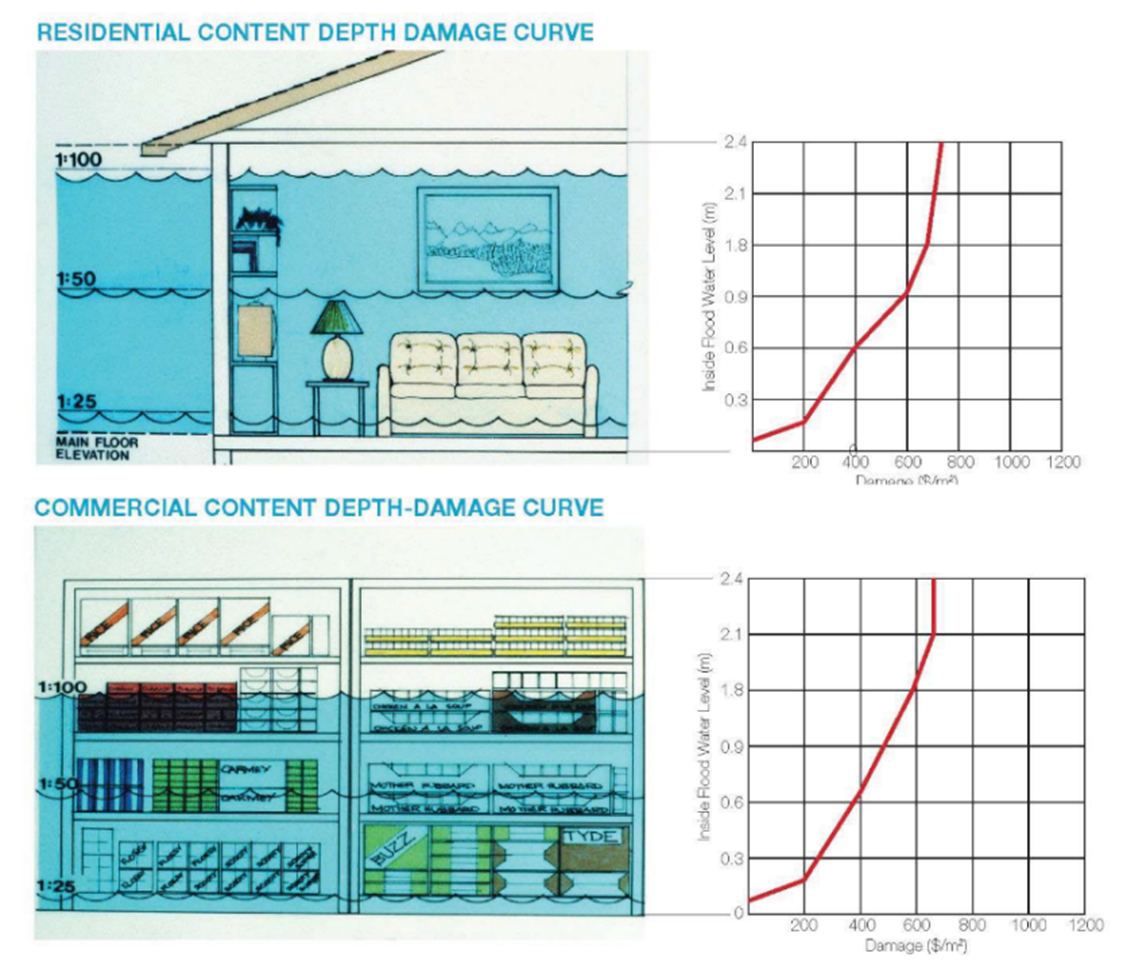

Figure 7: Example of Residential and Commercial stage-damage curves for contents

Text version

Figure showing an example of residential and commercial stage-damage curves for contents.

3.0 General practices

Practices in this document are included in each report section in tabular format. A summary of the general practices is included as Table 1, with additional information in Appendix 1.

| Number | General Practices |

|---|---|

| 1 | Flood Scenario and Depth Simulation. Refer to Federal Hydrologic and Hydraulic Procedures for Flood Hazard Delineation for details to develop a flood depth grid |

| 2 | Working with local community, assemble inventory of features that could be impacted, including buildings, infrastructure, population, etc. |

| 3 | Identify existing local stage-damage functions, develop functions if resources permit, or identify regionally similar functions |

| 4 | Establish and use a mechanism for internal checking and review of the selected/developed stage-damage functions and apply future adjustments or regional indexing as needed |

| 5 | Determine appropriate software toolset depending on the scope of project and expected results |

| 6 | As part of project activities, include a communications plan for disseminating results and any graphics, including maps |

| 7 | Complete a project report that includes a description of the following:

|

4.0 Range of flood hazards and factors affecting damage

This section describes the types of flooding which can be experienced across Canada, factors that may increase the damage resulting from flooding and select resiliency measures that can be implemented to decrease risk of flooding and damages. The information presented in this section is not an exhaustive list of all factors which may cause, contribute to, intensify or attenuate flood events.

4.1. Types of Flooding

Several types of flooding may occur across Canada, depending on the local setting, Table 2.

| Type | Description |

|---|---|

| Coastal / Storm Surge | When normally dry, low-lying land is flooded by seawater. This may occur by direct flooding, overtopping of a barrier or breaching a barrier, due to a combination of factors, including storm surge, tides waves, and freshwater input |

| Flash-flooding | Rapid on-set flooding, often features fast-moving water carrying a large amount of debris, can be fluvial or pluvial or a result from a heavy rain event, such as those produced by severe thunderstorms, hurricanes or tropical storms. |

| Groundwater flooding | As a result of rising water table. |

| Ice Jam | Chunks of ice clump together to block flow of a river at a natural or man-made feature. Flooding may occur upstream of the blockage or downstream when the ice jam breaks apart. |

| Large Lake Flooding | Abnormal sudden rise of lake level associated with a storm event |

| Pluvial flooding | Pluvial or surface water flood occurs when heavy rainfall creates a flood, independent of an overflowing water body. |

| Riverine (Fluvial) | Increase of water level beyond the channel capacity of natural or somewhat natural watercourse |

| Seiche | Period of oscillation of an enclosed body of water, may result in large waves |

| Tsunami | Series of waves caused by earthquakes or volcanic eruptions under the sea, or landslides |

| Urban flooding | Rainfall or snowmelt overwhelms the capacity of the urban drainage system, or when there is not sufficient overland flow route to move the water away |

4.1.1. Fluvial Flooding

Common factors that cause fluvial flooding are heavy snow melt and ice jams. Fluvial flooding can be slow-onset, relatively low velocity waters that extend beyond the river banks, or as a result of flash-flooding, see section 4.1.5. Inundation characteristics that influence damage include: area, depth, duration, velocity, rise rate, time of occurrence, contaminations, and salt-/fresh water. Typical stage-damage curves (see Section 7) may be used to assess damage caused by this type of flooding, however specialized curves and consideration is required for flash-flood fluvial events.

4.1.2. Pluvial Flooding

Pluvial flooding is generally related to poor drainage/stormwater management and results in pockets of flooding somewhat distant from the overland flow associated with the flood hazard area. This is typically treated the same as fluvial flooding in terms of estimating damages.

4.1.3. Groundwater Flooding

Groundwater flooding can occur when water levels within aquifer sediments increase as a result of hydraulic gradients induced by high river water levels or rainfall and snowmelt. The resulting high water table may affect constructed areas below grade such as basements and underground parking garages, either directly through infiltration between structural cracks and openings, or via artificial pathways created by water/stormwater/wastewater sub-surface infrastructure (IBI Group & Golder Associates, 2016). A high water table may also affect above grade properties when groundwater levels are high enough as run-off may occur. Typical stage-damage curves for basements and sub-surface infrastructure (see Section 7) may be used to assess damage caused by these types of flooding, groundwater and pluvial.

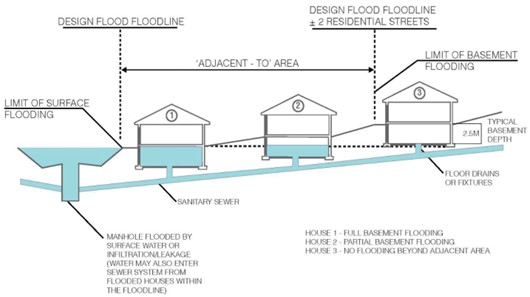

Basements that are lower than the floodwater elevation will suffer damages. To account for this potential flood damage, an adjacent-to area is delineated based on a distance of two dwelling units or +75 m from the design flood line (refer to Figure A-1, Appendix 1).

4.1.4. Coastal Flooding, Large Lake Flooding and Storm Surge

Flooding in coastal areas can be caused by a number of factors, depending primarily on the location and local climate conditions of the community, discussed in greater detail in Appendix 2. Similarly, large lake bodies can also experience storm surges, wave action and localized meteotsunamis generated from land and submarine slides or seiches.

Wave height is defined as the vertical distance between the trough and crest of a wave. In coastal areas, waves are irregular (in terms of direction, wave height, and wavelength) and are therefore characterized by “sea state” conditions. Significant wave height is commonly used for statistical representation of the sea state, where significant wave height is defined as the average of the highest one-third of wave heights in the sea state.

Flood forces such as high velocity flows, large waves, erosion, and floating debris can cause damage to structures and infrastructure (Federal Emergency Management Agency, 2006). Strong dynamic forces from high velocity flows may cause complete destruction of structures and their contents. Standard stage-damage curves do not consider velocity, and special consideration is required, see section 4.2.2.

Storm-surge flooding presents a greater threat to coastal communities than sea-level rise alone. Coastal communities are already coping with extreme water levels associated with climate variability (e.g., El Niño/La Niña Southern Oscillation) and storm-surge flooding. The risks associated with these events are expected to increase as sea level rises. Residential, commercial, institutional and municipal property and infrastructure in the region are vulnerable, and communities have begun to take action to reduce the risk through adaptation measures such as shoreline protection (Lemmen et al., 2016).

Storm surge can cause costly infrastructure damage and may isolate coastal communities though damage to transportation networks (Lemmen et al. 2016).

4.1.5. Flash-floods

Flash-floods, which can be caused by dam or dike breaching or failures may lead to high-velocity flows. The dynamic force of moving water from flash-floods or otherwise high velocity flows can cause, or contribute to, the failure of a structure if the velocity and depth of flooding combine to produce pressures that exceed the strength of structural elements and/or foundations. Large losses can be associated with destructive high velocity flooding.

4.2. Damage Influencing Characteristics

In this section, a number of factors that may influence and/or increase the damages incurred from a flood are presented, as many of these may not be accounted for in damage estimation software or risk assessment tools.

4.2.1. Effects of Climate Change

Coastal Flooding

Some low-lying coastal areas are at high risk of coastal erosion and coastal flooding, now and in the future, due to increases in sea levels and potential changes in intensity and frequency of severe weather events caused by climate change. “The global mean sea-level projection for RCP8.5, the largest emissions scenario, at 2100 is 74 cm (5%-95% range is 54 to 98 cm)” (James et al. 2014).

Significant rates of historical changes in relative sea level, largely related to glacial isostatic adjustments, are highly variable across Canada (e.g., >3 mm/year of sea-level rise at Halifax, Nova Scotia and >9 mm/year of sea-level fall at Churchill, Manitoba over the past century), making it a challenge to identify the effects of accelerated sea-level rise associated with climate change. (Lemmen et al., 2016).

The loss of sea ice in Arctic and Atlantic Canada further increases the risk of damage to coastal infrastructure and ecosystem as a result of larger storm surges and waves (Greenan B.J.W et al., 2018).

Fluvial and Pluvial Flooding

Looking at Canada as a whole, and based on available station data, there do not appear to be detectable trends in short-duration extreme precipitation (Zhang et al., 2019). Some stations show significant trends, but the number of sites that had significant trends is not more than what one would expect from chance (Shephard et al., 2014; Mekis et al., 2015; Vincent et al., 2018). Overall, more stations have recorded an increase, rather than decrease, in the highest amount of one-day rainfall each year. Precipitation is projected to increase for most of Canada, on average, although summer rainfall may decrease in some areas.

The lack of a detectable change in extreme precipitation in Canada is not necessarily evidence of a lack of change. On one hand, this is inconsistent with the observed increase in mean precipitation. As the variance of precipitation is proportional to the mean, and as there is a significant increase in mean precipitation, one would expect to see an increase in extreme precipitation. On the other hand, the expected change in response to warming may be small when compared with natural internal variability. Warming has resulted in an in-crease in atmospheric moisture, which is expected to lead to an increase in extreme precipitation if other conditions, such as atmospheric circulation, do not change (Zhang et al. 2019).

The seasonal timing of peak streamflow following snowmelt has shifted earlier in the year, driven by warming temperatures (Bonsal, 2019). These seasonal changes are projected to continue, with corresponding shifts from more snow-melt dominated regimes toward rainfall-dominated regimes. In the future, annual flows are projected to increase in most northern basins but decrease in southern interior continental regions, though no consistent trends in annual streamflow amounts have been identified. It is uncertain how projected higher temperatures combined with reductions in snow cover will combine to affect the frequency and magnitude of future snow-melt related flooding (Bonsal, 2019).

4.2.2. Velocity

An overbank velocity of 3 m/s acting over a 1 m depth can create sufficient force to overcome the design capacity of a typical residential wall (Paragon Engineering Limited, 1985). Generally, it is assumed that there is a low chance for building collapse for flow velocities less than 0.6 m/s, Appendix 3. While information from existing studies may be adequate for damage curve creation in most situations, it may be desirable to conduct specific calculations for notable buildings in the study area, with consideration of unique building materials, soil type, vegetation cover, and slope (Ontario Ministry of Natural Resources, 1997).

4.2.3. Ice

Ice can cause damage in several ways: flooding upstream of an ice jam (usually low velocity), high velocity flooding when the ice jam breaks up, and damage to structures near the river after the ice jam break-up. Ice jams may occur at natural bends of the river or at man-made locations (e.g.: bridge footings).

Frequent flood occurrence events (with low return period) generally produce minimal ice damages since ice is primarily confined to the main channel during these events (IBI Group & ECOS, 1982). For less frequent flood events (with high return period) ice may impact structures directly adjacent to the river. Since these structures would be subjected to severe damage caused by depth of flooding regardless of the influence of ice, the incremental damage from ice contact would be minimal (IBI Group & ECOS, 1982).

Ice can be pushed up many metres higher than flood waters by water flow and wind. Loading on substructures (such as pile supported structures) is many times greater under ice or debris loading than with clear water flows. Furthermore, ice can also damage structures through scarring and impact loading (unlike flood water alone). However, in some cases, shorefast ice can attenuate storm surges and may lead to less damage.

Further, freezing flood waters may cause extra damages to houses in the case of freeze-up jams (Burrell et al. 2015).

4.2.4. Duration

The longer a flood lasts, the larger the material damage and the damage due to the population and businesses due to interruption.

Duration is typically distinguished as short (<12 hrs) and long duration flooding (>12hrs) in the UK (Penning-Roswell et al. 2003). In the U.S. FEMA defines long-duration flooding as at least 72 hours. In both the UK and the US separate stage-damage curves have been developed for residential properties for short and long duration events.

In addition to the duration of inundation, the time to repair is also important. If saturated materials are not removed and/or dried immediately (24 to 48 hours) the likelihood of mold growth will increase and lead to increased damage (FEMA, 2005).

4.2.5. Sediment and Debris

The costs of removing deposited sediment from residential and commercial structures should be incorporated into structural damage estimates; the cost of removing sediment from roads should be included under indirect damages to highways and infrastructure (IBI Group & ECOS, 1982).

Beyond the post-flood clean of up debris, sediment and debris can cause additional damage after the flood due to erosion, scour, etc.

4.2.6. Contaminants

Contaminants such as toxic chemicals and sewage may exacerbate the damages resulting from flooding. The risks from such contaminants include increases to environmental hazards and disease (Erickson and Brooks, 2019). Bacterial diseases can pose significant health risks to the population. Toxic chemicals and gases in the flood water can also pose serious risks to human health. After the Hurricane Harvey flooding in Houston, Texas, more than 40 sites reportedly released hazardous pollutants (Erickson and Brooks, 2019).

4.2.7. Salt-/Freshwater

Flooding resulting from saltwater may increase damages, relevant in coastal areas. The presence of salt increases the conductivity of water and speeds up its ability to corrode metals and break down organic materials. In coastal regions this may also impact the natural chemical balance of the soil surrounding a property and could result in structural issues with foundations. Separate stage-damage curves which consider the impact of saltwater should be developed.

4.3. Damage Reduction Strategies

Numerous strategies can be employed to increase resilience to flood events. A few options are listed below, though this list is not exhaustive. Resilience strategies may be covered in more detail in the Federal Land Use Guide for Flood Risk Areas document.

4.3.1. Flood Warning Systems

Contingency measures, such as flood forecasting, warnings, and emergency measures, comprise some of the most effective techniques for reducing flood losses. Once the initial input datasets have been assembled, they have few or no environmental impacts, and can be implemented in a short period of time. They also offer a high degree of flexibility and can be adjusted in accordance with changing future conditions. Furthermore, they aid in promoting awareness and resident responsibility.

Given sufficient advanced warning time, in conjunction with a good public awareness campaign, total flood damages can be substantially reduced by owner-initiated activities (see Appendix 4). In fact, one of the most beneficial and cost-effective actions that a resident or business can take is to relocate items to a higher elevation. Research shows that communities that suffer frequent flooding will have reduced potential damages in comparison to communities that have not been impacted by a severe flood in recent memory [Stewart, 2007].

4.3.2. Municipal Bylaws

At the municipal level, local bylaws can be used to regulate the development of land and building construction that is subject to flooding. Refer to the Federal Land Use Guide for Flood Risk Areas document from the Federal Flood Mapping Guidelines series for more detailed discussion. Community floodplain mapping is recommended to identify these areas that are subject to flooding and delineate flood hazard zones.

5.0 Types of flood damage

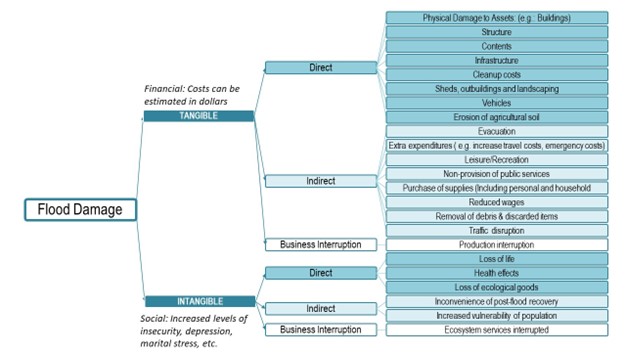

Damage resulting from major flood events can be broadly categorized as tangible damages or intangible damages. Tangible damages refer to damages to which a dollar value may be assigned. Intangible damages refer to damages that cannot easily be assessed monetarily such as emotional stress, illness, or loss-of-life.

The focus of this document is on quantifying tangible damages, which can be further categorized as direct damages and indirect damages, however, some prescriptive methods for estimating a number of indirect tangible damages are also included (Figure 8). Direct damages are those that occur immediately and can be directly attributed to flood inundation. Direct damages include damage to public infrastructure and private property. Indirect damages occur as a result of direct flood impacts but they are more difficult to quantify. Indirect damages include, for example, reduced economic activity, individual financial hardships, adverse impacts on the social well-being of a community, and disruptive impacts. Indirect damages are often estimated as a percentage of direct damages.

(Adapted from Flood Damage Assessment in Alberta, Best Practices and Guidelines, 2015)

Figure 8: Types of Flood Damage (not exhaustive).

Text version

Graphic listing a non exhaustive list of financial and social damages caused by a flood.

Flood damages may be assessed using a financial or economic impact approach. Financial impact refers to the sum of financial losses experienced by individuals or organizations as a result of a flood. The scale of the damage assessment should be defined by the flood-affected area. The outcomes of the assessment may be used to support flood management to reduce damages to properties and individuals. Beyond financial losses, at a larger scale, economic losses can be calculated as a sum of individual financial losses (and/or gains), to model economic losses for a region.

In many flooding situations, the actual damages incurred are less than the potential damages because sufficient warning is provided to the community such that mitigation measures can be taken in advance.

5.1. Tangible Direct Damage

There are several approaches to estimating tangible damage to buildings due to flooding.

Applying stage-damage curves is the most common and internationally accepted method for estimating tangible direct damage at urban scales. These stage-damage curves represent the relationship between flood depth and the estimate of absolute economic loss (in terms of currency) or relative loss (percentage of the estimated replacement value of property) of a building’s structure and contents. They may be derived by empirical (rely on data from past flood event) or synthetic techniques (conceptual approach and expert knowledge).

Probabilistic stage-damage functions are derived from stage-damage curves. They are commonly used to evaluate damages resulting from other natural hazards, e.g.: dam breaks, earthquakes, tsunami and fire. Probabilistic curves express the variability in the damage estimation process. These curves indicate the probability of damage exceeding certain spending thresholds (or damage states) based on various flood levels (McGrath et al., 2019).

Another method is through damage-frequency relationships. Damage-frequency relationships can be developed through direct examination of damage within the floodplain following flood events. If numerous estimates are available for a variety of flood events, a damage-frequency relationship could be developed from the data by plotting damage with respect to flood frequency or return period. However, the validity of using such relationships deteriorates with changes in land use over time as historical damage estimates based on historic land uses may not reflect the current-day land use or construction and contents costs.

Alternatively, a synthetic damage-frequency curve, from which average annual damages can be estimated for a given study area, can be used to assess damage. A synthetic damage-frequency curve can be produced from damage-frequency relationships by hydrologically determining various flood elevations for specific flood frequencies and synthetically deducing the damages that would result from these events. This method of computing a synthetic damage-frequency curve from damage-frequency relationships is considered to be the best approach for obtaining damage estimates based on current economic factors and has been proposed for use across Canada for riverine flooding.

While the above approaches are the most common, there are other methods of assessing other types of damages, for example using indicators or proxies.

5.1.1. Riverine Setting: Flood Damage Estimation Procedure

Buildings

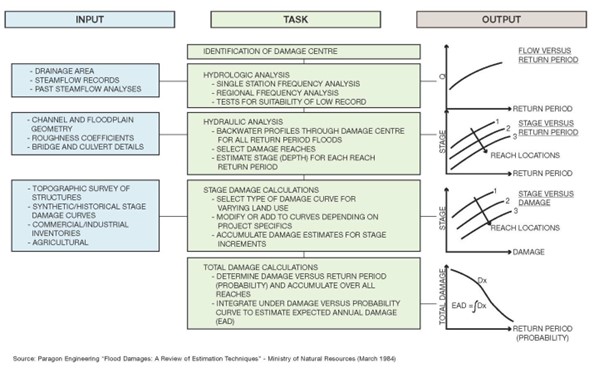

Flood damages in areas prone to riverine flooding may be estimated using a four-part procedure composed of a hydrologic analysis, a hydraulic analysis, stage-damage calculations, and total damage calculations. This procedure is summarized in Figure 9.

Flows associated with various return period or probability events of interest are computed through the hydrologic analysis. Technical guidance on hydraulic and hydrologic procedures for preparing flood hazard maps can be found in the Federal Hydrologic and Hydraulic Procedures for Flood Hazard Delineation document.

The level of inundation for each property depends upon the grade of the property, the flood elevation and the floor heights above grade or a combination of these. The grade of the property may be established using a DEM derived from LiDAR, or alternatively, from ground level surveys or detailed topographic maps. The flood elevation may be derived from hydraulic flood modelling or from historical flood events (if available). Floor heights above grade can be established from building approval records, traditional field survey, or the use of street-level videos/photography.

Given an inventory of flood affected properties for a given return period event, and the depth of inundation at each property, stage-damage relationships can be applied to estimate the dollar value of direct content and structural damages. Indirect damages may also be estimated.

Total damage calculations involve computing the total damage for each return period flood event considering direct and indirect damages. Accordingly, total damage may be plotted as a function of return period or probability. Damage estimates may be expressed as expected value of annual damages. Annual damages are extrapolated from damage versus probability curves. Repeating the assessment with consideration of different mitigation measures will produce different expected values of annual damages. The reduction in estimated annual damages associated with each mitigation measure can be compared to the annualized project costs to support decision making and selection of flood mitigation options (Paragon Engineering Limited, 1984). Appendix 1 contains a breakdown of the aforementioned flood damage calculation procedures.

Figure 9: General Flood Damage Calculation Methodology

Text version

A figure describing the general flood damage calculation methodology

Damage to Other Infrastructure

In addition to buildings, there are a number of other assets that may potentially be exposed to flood damage. For example, direct and indirect damages may be inflicted upon:

- Roads and transport infrastructure;

- Parks and recreational facilities;

- Water, sewerage and drainage systems;

- Communication networks;

- Electrical power;

- Food/agriculture systems

Traditionally, most of these assets were publicly owned. However, the increasing trend towards privatization of services may have an influence on the costing methodology used to assess damages.

In general, the repair and replacement of roads and bridges represents the largest component of damages to public assets. The amount of damage caused depends upon the flood-related factors and the ability of the road to withstand flood conditions. Relevant factors include both the initial repair cost and the possibility of a significant reduction in the overall life of the road surface as a result of the flood.

Generally annual maintenance costs and other documented historical costs can be used to develop locally specific damage costs. Where this information is not available, data from other studies may need to be used. Depending upon the specific circumstances, these damages can vary greatly. Damages to assets categorized as “other infrastructure” generally range between 10% and 25% of direct damages to residential, commercial and industrial structures.

If damage estimates or actual damages can be determined for a specific return period and aerial extent of inundation, infrastructure damages can be interpolated for greater and lesser return periods based on the aerial extent of inundation (e.g.;., 75% or 125% of measured inundation area). Some judgement may be required in terms of land use mix and actual infrastructure components located within the flood hazard area.

5.2. Intangible and Indirect Damage

In addition to direct damage to property, a variety of secondary economic, social and environmental impacts are caused by flood events. The benefit-cost approach to disaster mitigation assessments theoretically requires a complete enumeration of all gains/benefits and losses/costs associated with a project (Ganderton, 2005). In practice, however, it is not possible to identify, quantify, and monetize all potential impacts.

The convergence of social, environmental, and economic issues with disaster mitigation under the umbrella of climate change adaptation has stimulated the field of risk assessment. Indirect and intangible impacts are receiving greater attention and, in some cases, are shown to be as substantial as direct costs (Joseph et al., 2014). Despite this, there remains very limited useful data upon which to assess indirect or intangible damages and no consensus on methodologies (Gall & Kreft, 2013). This leaves a tremendous gap between current theory and practice as well as great disparity within practice (a note of concern).

A major reason there are no practical examples of studies that reflect robust and detailed disaster loss estimate theory may be that it requires location-specific details that are not readily transferable. Thus the great time and cost make it prohibitive and the necessary data may be unattainable.

Due to these limitations, it is not feasible to arrive at the “total cost” of a flood by summing estimates for all the components. However, there are some general methods available that allow for the consideration of monetized indirect and intangible impacts, as outlined in the following sections.

5.2.1. Intangible Damages

Intangible damages are those for which establishing market value is extremely difficult. Human health impacts and damage to the environment both have intangible aspects. It is challenging to quantify intangible impacts caused by flood events. Floods do not lend themselves well to controlled studies that connect population and flood characteristics to outcomes (Tapsell, 2009). The intangible impacts of flooding on health and quality of life are highly dependent upon variables beyond the flood characteristics including an individual’s prior health, income, family and community support, preparedness and experience, and a host of other social indicators and behaviours. A 2017 report by IBI Group prepared for the City of Calgary describes a case study in which intangible damages were assessed.

Public Health and Quality of Life

There is little evidence to characterize most intangible outcomes of specific flood events/contexts (IBI Group, 2017). The process of quantifying the individual impacts relies on a large number of assumptions for each component variable. Monetization of these impacts requires further assumptions and transfer of values from other sources, most with no relation to flooding or the local context.

The available monetary values for all the impacts originate from various studies and contexts but ultimately they are all assumptions based on willingness-to-pay surveys (WTP) or choices and preferences of people somewhere. Complex calculations based on these values, estimated probabilities, and flood and population characteristics can lead to a value for each impact. However, this can obfuscate the origin of the data and the assumptions it contains. The end result will have questionable meaning or relation to stakeholders.

Furthermore, individually monetized impacts can yield values that are generally insignificant relative to the direct damages. Complex attempts to quantify injuries, disease, infection, and exposure can also lead to low values. This is not to suggest that these factors are not important, but the economic risks in this case are actually rather low. However, the impact on affected households is obviously considerable.

Two WTP studies related to flooding, and their applicability to Canada, are summarized in Appendix 5. At this time, an average value of $1,000 CAD per household per year is recommended. This amount can be adjusted based on the community profiles according to a risk scale of low ($700), average ($1,000), and high ($1,300). Further research is required to establish a Canadian WTP value.

Environment

Lasting environmental effects owing to water contamination from flooding will depend greatly on the characteristics of floodplain development. Restoration work conducted in or near waterbodies covered by the Fisheries Act necessitates offsetting costs to compensate for damaged habitat. It can be assumed that the costs of fish habitat offsetting measures are representative of the monetized damage corresponding to river bank stabilization projects. The total values from past events can be correlated to flow rates for those events and applied to the new flood data for each return period.

5.2.2. Indirect Damages

Indirect damages include costs of evacuation, employment losses, administrative costs, net loss of normal profit and earning to capital, management and labour, and general inconvenience. Indirect damages are best evaluated by developing a checklist of potential effects and methodically assessing each one. For example, the checklist would include the amount of use and the duration of interruption of transportation and communication facilities, the number of workers and farmers depending on closed plants, and the amount of business lost during a flood emergency. The magnitude of each effect may be estimated by interviewing those affected during recent floods, and unit economic values may be assigned by market analysis. Finally, the results may be summed to render a total value for indirect damages.

The complexity of the above evaluation process has led agencies to estimate indirect damages from direct damages based on percentages of direct damages. The ratios are chosen based on a review of the literature, empirical evidence, and expert opinion. For indirect damages that are associated with buildings, such as business disruption and residential displacement, another approach is to develop synthetic stage-damage curves.

Loss as a Percentage of Direct Damages

Indirect damages can range from 10% to 45% of direct damages for specific land use categories but are commonly calculated as 20% of direct damages. The Canada-Saskatchewan Flood Damage Reduction Program estimated indirect damages as 20% of all direct damages. This figure is in accordance with guidelines developed by the U.S. Soil Conservation Service who, in the past, suggested the following ranges for indirect damages:

- Agricultural: 5% to 10%

- Residential: 10% to 15%

- Commercial/Industrial: 15% to 20%

- Highways, Bridges, Railroads: 15% to 25%

- Utilities: 15% to 20%

Business Disruption Damage Curves

The impacts of major flood events on business are complex and varied. The main indirect damages suffered by businesses relate to disruption of business activities during the flood and restoration process or failure to re-open post event. This may occur as a result of damages to the business’ structure, equipment, and inventory; or because of access restrictions owing to evacuations, road closures, or loss of utility services. Methods for estimating the tangible indirect damages associated with business disruption are presented in Appendix 6.

There are a number of other factors that may influence indirect business damages including, for example, the cost of loans versus relief funds, the relationship between the business and the specific location, and the relationship between the business and other services and suppliers.

Residential Displacement Damage Curves

Structural damage from floodwaters, loss of critical services, or access restrictions owing to evacuation and road closures can all lead to residential displacement. During and after a flood event, affected residents will have to find alternative accommodations and incur extra personal expenses. Expenses may include restaurant meals, daily essentials, hotel costs, and extra fuel. Residents of buildings that require substantial repairs will require alternative accommodation for a longer period and incur costs for moving and rent.

Residential displacement costs are not often explicitly estimated in flood damage assessments but the required assumptions are relatively straightforward. Methods for estimating the tangible indirect damages associated with residential displacement are presented in Appendix 6.

Traffic Disruption

Floods can cause major traffic disruptions as a result of water on roadways, road closures, and required evacuation. Traffic delays also have associated financial and social costs. While traffic disruption is occasionally mentioned in literature related to flood impacts, it is rarely included in flood damage assessments. There are some studies on the economic impact of particular highway closures caused by flooding or landslides, but very few on urban flooding. Overall, detailed modelling of flood impacts on traffic is normally beyond the scope of flood damage estimation and is generally not warranted because the expected value is small in relation to other damages. Nonetheless, a description of the costs associated with traffic delays is included in Appendix 7 as well as a set of assumptions which may be employed to estimate vehicle disruption from municipal traffic modelling data.

Waste Disposal

The majority of flood-damaged property is disposed of in landfills. During a large-scale emergency clean-up operation, proper sorting of recyclable material or hazardous waste is often not performed. Additionally, current practice is to dispose of many items that might have been repaired in the past. This amounts to a great deal of waste from each flooded building.

Waste disposal has costs associated with collection, operation of the facilities, land usage, and environmental impacts.

The amount of post-flood waste created is assumed to be related to the total direct damages to buildings and contents. Damage calculations for waste removal can be calculated using past flood data. For example, City of Calgary landfills normally charge $113 per tonne for basic waste and $170 per tonne of construction and demolition materials when part of a mixed load (Calgary 2019). The amount for mixed load materials waste is assumed to represent the landfill cost for the flood-related waste. An additional $50 per tonne can be added to account for the time of private operators to bring the waste to the landfills. In general, damages associated with waste disposal equate to approximately 1.7% of estimated direct building and content damages.

Flood Fighting and Emergency Response and Recovery

Flood fighting and emergency response requires considerable effort by local administration and volunteers and it is often unaccounted for in damage estimates, or alternatively, included under indirect damages computed as a percentage of direct damage. The best source for costs related to this category is municipal records on past events. With a known amount for a given flood return period, or for an observed flood event, estimates for other return periods can be extrapolated using the inundation maps. The relationship between cost and direct damage or inundated developed area can be used.

6.0 Tools for estimating damage

In Europe and across North America, numerous computerized flood database and damage estimation models are employed for estimating flood damages. The majority of European models, with the exception of the UK are area-based models that calculate damage based on aggregated land use characteristics. In North America, the models are primarily object-based, calculating damages to individual buildings and include a large number of object types and corresponding flood damage characteristics to determine damages. Advantages of the object-based models is that they can control for varying building density and type, can be easily setup for rapid calculation over larger areas, and they enable scenario analysis. Smaller-scale studies in which the damage estimates of individual properties strongly affect the outcome will benefit from an object-based approach.

6.1. Large-Scale Analysis

There are several models in use across the country for flood damage estimation in Canada. The first computerized flood damage assessment system used in Canada was developed in the 1980’s. A number of software tools and their abilities are summarized in Appendix 8; much of the summary is based on research conducted by Lyle & Hund (2017).

All of these approaches have relied on stage-damage curves for damage estimation. Canadian studies have typically employed methodology aligned with Acres (1968), whereas U.S. studies have typically employed methodology aligned with the Flood Insurance Administration (FIA) (Federal Emergency Management Agency, 2016b). The differences between these approaches are highlighted in Table 3.

Given that major modifications to Hazus-MH would be required for effective and accurate use in Canada, it is recommended that the CanFlood, Alberta Provincial Flood Damage Assessment Tool (PFDAT) and Ontario Flood Damage (FLDDAM) programs be adopted for Canadian flood damage assessment studies.

| Acres approach | FIA Approach |

|---|---|

| Canadian data and experience. | U.S. regionalized experience (no Canadian verification). |

| Units by construction type relative to architectural/economic categories. | Units by construction type. |

| Contents damage evaluated through survey. | Contents damage expressed as a percentage of appraised value of structure. |

| Structural damage evaluated through detailed estimation of categories. | Structural damage expressed as a percentage of appraised value of structure. |

| Requires classification by category. | Requires individual appraisal of each unit. |

| Contents damage relates to general income grouping through unit categorization. | Contents damage is not related to income. |

| Considers basement damage. | Does not adequately consider basement damage. |

| Detailed evaluation for non-residential damage curves. | Non-residential damage curves inadequately represented. |

When using these software, it is necessary to consider the source of the stage-damage curves applied in the damage estimation. Stage-damage curves typically represent an ‘average’ structure of a given category. Thus, when considering a single structure, the damage estimate contains uncertainty, based on the aggregation of the results from structures of a similar type, but different valuations and sizes. This uncertainty increases with increasing water depth. For example, variability of Ontario stage-damage curves from a sample of 76 one-storey residences with basements found a variability of ~$10,000 at a water depth of 0 m and ~$25,000 at a flood depth of 2.4 m (Paragon Engineering Limited et al. 1985; McGrath et al., 2019). For larger-scale analyses (e.g.: community level), the local inaccuracies can be expected to average out to a certain extent. In addition, many communities do not have sufficient resources to develop their own curves and may adapt those developed in other communities or regions. This can also lead to uncertainty in the resulting damage estimate. Thus, further refinement of the programs is recommended in order to incorporate the desired functions and ease-of-use for use in future Canadian studies.

A lack of detailed building inventory can lead to challenges in building or community level damage estimation and risk assessment. The challenges are largely related to the quality of data available and the amount of data processing required. In most municipalities these challenges can be easily overcome. However, in larger urban centers containing areas of dense and multi-use building arrangements, difficulties can arise.

6.2. Individual Building Analysis

The tools described in the previous section are also capable of object based, or individual building level analysis in addition to the large-scale analysis, however, individual building results must be used with caution, especially if stage-damage curves from other regions have been employed.

Xactimate® is a software tool used for individual building damage estimation as well as municipal level evaluations and claims handling. This software is used by many Canadian (and U.S.) insurance companies as well as restoration contractors and adjusters. The Xactimate system allows for digital data entry of a buildings’ dimensions, rooms and contents and is able to access an extensive database of costing tables and price lists. In addition, users can upload regional labour rates and price lists.

6.3. Database Issues and Considerations

Good database design is essential for damage estimation. The design should consider the necessary attributes required and limit user response options through inclusion of drop-down menus to promote standardization.

One major issue in the damage estimation process relates to the fact that assessed value within records includes land and improvements and therefore one cannot apply standard Content to Structural Value Ratios (CSVR) as it will overstate the content value. For multi-tenant buildings there is no way of disaggregating assessed value by specific unit or use such that one can apply an appropriate CSVR (Hence, the Hazus-MH and HEC-FDA damage estimation methodologies cannot be applied). Business type descriptors for retail are typically not subdivided into specific types (i.e., shoes, clothing, electronics, paper products, groceries), and therefore do not allow for the fine-grained contents assessment by specific business type.

Common data quality issues and possible solutions, as well as a discussion of available internet tools to assist in building classification can be found in Appendix 9. Future development of a comprehensive flood damage database would benefit from gathering of the following information (e.g. through tax assessments).

7.0 Stage-damage curves

Damage to residential and commercial properties and contents caused by inundation during flood events can be assessed using stage-damage curves. Direct flood damages should be estimated separately for residential and non-residential structures. Additionally, structural damages should be estimated separately from content damages.

Structural damage refers to damage to the building and to stationary building components such as furnaces, hot water heaters, carpeting, etc. Content damage refers to damage to moveable contents within a structure (McBean et al., 1986). Contents and structure data should be collected from a representative sample of units located within the defined flood hazard area. Effort should be expended to identify units that are “typical” of their residential classification in terms of size, assessed value, and apparent quality.

Baseline damage estimates should reflect total potential damages and should not consider any existing mitigation measures. Essentially, this approach assumes failure of existing mitigation structures and absence of any non-structural mitigation measures. This methodology permits benefit/cost analyses of proposed mitigation options against the baseline condition.

Sample data collection forms for residential (Appendix 10), and commercial properties (Appendix 11) are included.

Stage-damage curves, developed for the City of Calgary in the IBI Group and Golder Associates 2015 report, for residential and commercial properties are included in Appendix 12 and Appendix 13 respectively. The content item and price list utilized to develop the stage damage curves is found in Appendix 14.

7.1. Residential Stage-Damage Curves

Potential damages vary substantially based on type of use (building occupancy classification), construction materials, construction techniques and quality, and the quantity and nature of contents located within the structure. Therefore, it is necessary to formulate a classification scheme capable of encompassing considerable variations in housing types found throughout the study area. Accordingly, stage-damage curves may be developed for each category of the classification scheme. A number of residential classification schemes have been developed from previous Canadian studies and projects, a summary and example photographs are found in Appendix 15.

Exterior finishing materials show some variation by region: in the western provinces there are more stucco and siding materials, brick is used extensively throughout Ontario, while clapboard and siding are the predominant materials in Quebec and the Atlantic provinces. Exterior materials are generally not considered in flood damage estimates as they generally suffer little to no damage under general riverine flooding conditions. High velocity flows, ice and debris in the flood water can contribute to greater exterior damage.

7.1.1. Development of Content Damage Curves

In general, it is recommended that region-specific content damage curves are developed to reflect the characteristics of the study area. Additionally, content damage curves should be developed separately for each storey (basement and main level), and each residential structural category, calculated on a dollar-per-square-metre-of-floor-area ($/m2).

Following the development of the contents inventory, content stage-damage curves may be calculated for each storey and each class of residential dwelling unit. The calculated flood damages occurring at each depth of flooding above floor level should be averaged on a dollar- per-square-metre-of-floor-area basis.

In flood-affected areas where large high-value, single-family homes represent a small percentage of the total inventory (less than 1%), it is not possible to obtain a sufficiently large sample of content inventory. In these cases, the content damage curves may be estimated at a premium of 1.44 over the next highest class structures.

Garden tools, garden furniture, and garage contents should be inventoried as part of the residential contents survey (IBI Group & Golder Associates, 2015). To account for landscaping and yard clean-up costs, guidance is provided in Appendix 16 for different classes of properties. Appendix 16 also contains a description of studies in which external damages were considered in flood damage estimates.

7.1.2. Development of Structural Damage Curves

The structural characteristics of residential units in each class should be determined through field inspection by qualified architectural personnel and consultation with the local building industry. Typical basement unit floor areas and first floor areas may be determined for each class of residential unit from municipal assessment data, otherwise, interviewers should collect information on building floor areas, exterior finishes, building and room perimeters, and types of interior finishes (IBI Group & Golder Associates, 2016).

The average floor areas data collected through field inspection surveys can be combined to develop the profile of typical units in each residential classification.

Estimates of unit prices for cleaning, replacing and/or repairing flood damaged materials may be obtained from local suppliers and contractors. All structural damage curves should reflect the costs of cleaning, repair, and restoration estimated on the basis of current local material and labour costs. It should also include the cost of removing residual standing water, sediment, removal, disposal of damaged items, structural drying and sanitization, final inspection and testing for dryness and residual contamination.

It is common practice to remove and replace all non-structural materials that have been in contact with floodwater for residential flood remediation. In addition, due to moisture wicking upwards through semi-permeable building materials, very high ambient humidity levels inside structures, and the probability of mold growth on common residential finish materials, it is now a recommended and generally observed practice to remove virtually all finish materials on floor levels that experience any substantial duration and depth of flooding with Category 3 waterFootnote 1.

The major structural components of a typical dwelling unit, if properly maintained, have a life expectancy that virtually defies application of arbitrary depreciation rates. In general, deterioration is related primarily to wear of finishes, wall and floor coverings, and similar materials, as long as these materials in the typical home are generally well-maintained. Consequently, no depreciation estimates need be applied to replacement and/or restoration values used to construct the structural stage-damage curves.

Based on dwelling unit characteristics and unit prices, damage for each 300 mm of flooding should be estimated for each class of residential unit, floor level, and structural type.

Attached and detached garage damages should be included for all building classes excluding mobile homes, low-rise apartments, and high-rise apartments. Structural damages for low- and high-rise apartment parkades should be calculated separately on a structure-specific basis..

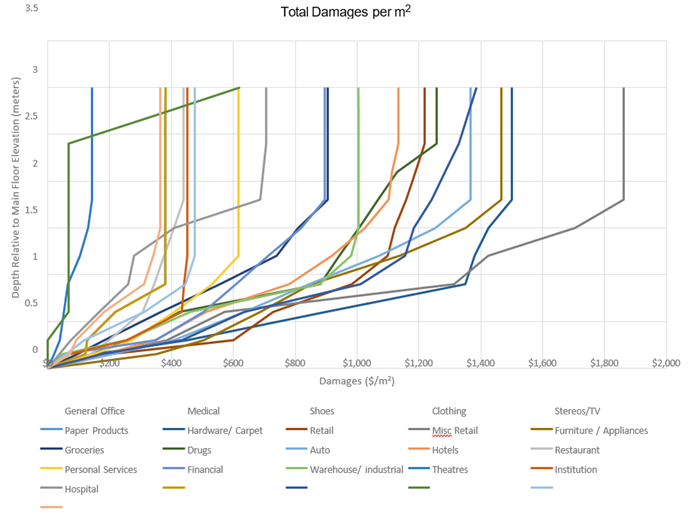

7.2. Non-Residential Stage-Damage Curves

Non-residential buildings including commercial/industrial and institutional establishments, include inventory, equipment, and building damage as well as clean-up costs. As with residential structures, content and structural damages should be calculated separately. Due to the range and diversity of activities associated with non-residential buildings, this group does not demonstrate the same uniformity as the residential grouping. Consequently, categorization is much more complicated and it is necessary for similar types of commercial activities to be grouped together.

Appendix 17 provides a detailed description of the commercial/industrial classes used in the Alberta Provincial Flood Damage Assessment study (IBI Group & Golder Associates, 2015). The corresponding commercial damage curves are presented in Appendix 13 and detailed descriptions of restoration activities and assumptions employed in constructing these curves and the representative commercial industrial establishments can be found in the 2015 report by IBI Group and Golder Associates.

7.2.1. Content Damage Curves

Commercial contents are primarily composed of inventory. Furthermore, commercial content damage estimations should be based on the non-salvageable portion of affected inventory.

In general, reported levels of salvageability are quite low reflecting the same restoration difficulties, health and safety concerns, and cost issues described for residential contents. Fixtures and furnishings damages should reflect replacement costs and commercial content inventories should reflect replacement (wholesale) values.

7.2.2. Structural Damage Curves

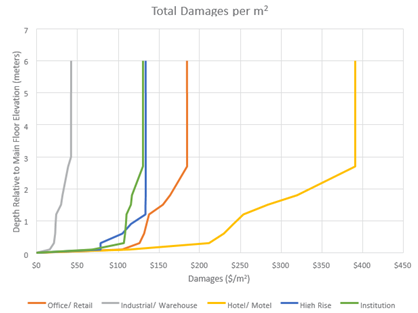

Structural damage curves for non-residential buildings were developed from first principles based on a six-fold classification scheme. The six categories in the classification scheme include office/retail, industrial/warehouse, hotel/motel, institutional, office towers, and multi-level parkades.

Structural damage curves can be constructed using actual building plans to determine areas and levels of finishes. Estimates of unit prices for replacing and/or repairing flood damaged materials may be obtained from local suppliers and contractors. Structural damage curves should reflect the costs of repair or restorations estimated on the basis of present-day regional material and labour costs.

One difference with respect to restoration of non-residential versus residential structures is the practice of “stepped” rehabilitation versus wholesale residential renovation at low levels of flooding. This is due to a number of factors including:

- The use of more durable materials that have a higher level of salvageability;

- Cleaning and structural drying is easier to implement;

- As commercial buildings are a for-profit venture, owners attempt to minimize repair costs and downtime; and

- Insurers exercise a higher degree of caution in residential remediation due to potential liability relative to health and occupancy issues.

Multi-Level Below-Grade Parkades

Stand-alone multi-level below-grade parkades, along with those associated with mid- and high- rise offices and residential buildings, constitute a new damage category not previously encountered in the literature. A value of $215/m2 is suggested to estimate damages for structures that belong to this category (IBI Group & Golder Associates, 2015) as further described in Appendix 18. Depending on the time of day, advance warning and neighborhood, the type and cost of vehicles that may be in the parkade will vary. This may need to be considered individually.

7.2.3. Industrial Damages

A field survey of specific industrial establishments is recommended employing the sample questionnaire contained in Appendix 11. With regard to the survey, one should (Ontario Ministry of Natural Resources, 2007):

- establish a contact for the plant manager or foreman;

- review with the contact, the nature and vertical placement of all major equipment and inventories;

- determine if inventories vary with season;

- determine the value of down-time in relation to revenue, to help assess indirect costs;

- assess structural damage that would be incurred; and

- if flood forecasting opportunities exist, determine what adjustments are enacted to decrease damage (another measure of indirect cost)

If the level of effort does not permit detailed damage surveys, it is suggested that the Province of Alberta 2015 Commercial/Industrial/Institutional Depth-Damage Relationships provided in Appendix 13 be employed with indexing to account for inflation and regional cost differences.

7.2.4. Agricultural Damages

Agricultural damages include damages to crops, soil, equipment and implements, farm supplies (such as fertilizer and seed), farm structures, and livestock mortality. They are primarily dependent on the timing and duration of flooding, in contrast to other damages, which primarily depend on the depth of flooding. Losses associated with damage to crops can be adjusted according to the type of crop and size of area inundated.

For each crop type in the study area, data requirements include:

- The yield and market value per hectare (acre) of land for each crop type;

- The flood-free gross income, calculated using adjusted normalized prices (if required) for each crop type (refer to Section 8.1 on price adjustments)

- The costs of production, broken down by month;

- The monthly probability of flooding for each flood depth, a value that can be estimated by a hydrologist;

- The monthly damage rates (also referred to as crop loss functions), a value up to 100% of the total production value of the crop obtained based on the history of flooding in agricultural areas for each month in which flooding occurs (these values can be derived from literature reviews and interviews with farmers and local agricultural specialists); and

- The aerial extent of each crop type in the study area.

Procedures for estimating damages to crops, livestock, and barns and outbuildings are presented in Appendix 19. The recommended coding for agricultural crops, livestock and buildings and equipment are shown in Appendix 15, Table F-8.

7.2.5. Unique Structures/Uses

Not all structural types or uses will fit into the standardized residential, commercial and industrial classifications established for stage-damage curves development. These structures include very specialized buildings like hospitals and sports facilities/arenas and uses such as campgrounds, parks and golf courses. In these instances, potential damages should be estimated from first principles employing data collection instruments to determine direct and indirect damages, similar to the methods employed for constructing the standardized contents and structural damage curves. Appendix 20 describes a case study in which this methodology was employed.

7.3. Limitations in Stage-Damage Curves

A brief discussion of the uncertainty associated with structural classification schemes and stage- damage curve development is presented in Appendix 21. Stage-damage curves are presented as a single relationship for a given water depth, a given dollar value of damage and typically exclude other damage-inducing parameters such as flow velocity, debris and contaminants.

7.3.1. Damage due to Velocity

When calculating damage in areas where velocity is a factor, depth should be calculated relative to the bottom of the floor beam of the lowest floor (the main level) in coastal and lake flooding, whereas the top of the finished flooring of the lowest floor is used as the reference level with riverine flooding (Federal Emergency Management Agency, 2006).

Specific calculations for structures under high-velocity flows must be conducted to determine whether structural failure will occur for given flooding characteristics (Paragon Engineering Limited, 1985). FEMA functions showing building collapse potential as a function of wave induced velocity and depth are shown in Appendix 3.

To estimate damage as a result of total destruction, the total structural and content damages that would result from inundation alone should be estimated for the basement and first floor and multiplied by a value of 2.86. Alternatively, the replacement cost of the structure may be estimated using the assessed value of the property under normal market conditions (less the value of the land) and added to the total insured value of the contents of the structure. These estimates may be converted to a per-square-metre basis to facilitate further analyses and the development of standardized damage functions.

If it is determined that a structure is not expected to collapse, then damages can be estimated based on inundation alone.

In the event of a mobile home collapse, or other type of home without a basement, it is assumed that none of the building contents would be saved or moved to higher ground. Therefore, damages may be estimated using the methods described in Section 7.1. Note that mobile homes need not be adjusted for the value of the lot since they are commonly leased.

8.0 Future adjustments and regional indexing

8.1. Updating to Current Year Dollars

Stage-damage curves should continually be updated to represent current-year dollars and take inflation into account. As a result of inflation, past damage-curve estimates may not be directly applicable to future flood events. However, since changes in a variety of prices are regularly tracked by Statistics Canada, it is possible to develop an appropriate index to update base-year estimates to accommodate relevant price changes over time.

Damage estimates from any previous base year can be updated to a new base year. To do so, one simply multiplies the damage values by the ratio of the current index value over the index value from the previous base year, as followsFootnote 2:

Current Damages = Base Year Damages x (Current Year Index / Base Year Index)

8.1.1. Available Measures of Price and Spending Change

Different procedures are required for the adjustment of residential versus non-residential damages, and similarly for the adjustment of contents versus structural damage. Accordingly, a number of price and spending change measures must be employed to adjust damage estimates to reflect current-year dollar values. These measures include the consumer price index (CPI), construction price indexes, and the survey of household spending (SHS). Descriptions of each price and spending measure are included in Appendix 22.

8.1.2. Updating Residential Content Damages

The “all-items” CPI is an aggregated index reflecting price movements of a collection of products and services purchased by consumers. The “all-items” CPI is commonly used to update content damage estimates from a previous year. However, the use of this index introduces error into the flood damage analysis since flooding affects only a particular group of items from the CPI basket.

To account for the aforementioned shortcoming of the “all-items” CPI, the adjustment computations can be conducted by selecting only the sub-categories of the “all-items” CPI directly related to flood damage; individual CPI values are available for all sub-categories of the “all-items” CPI. This procedure is described in Appendix 23, although it is not the preferred approach for updating residential content damages.

It is important to note that the CPI is intended to represent pure price changes of standardized goods. It intentionally does not account for changes in quality or technology. Computers and other electronics illustrate this effect; the index price of a computer with an unchanging processing capability will drop substantially over a relatively short time. However, because the technology continues to improve, the average new purchase price may be unchanged or possibly increase. Additionally, the individual CPI indexes cannot account for changes in consumer behaviour caused by changing prices or incomes.

For example, if clothing prices drop or income increases, a household may buy more clothing but have a clothing inventory with a value that did not decrease.

A better measure of the change in household content value over time is the Statistics Canada SHS. Average household expenditures are measured annually in categories similar to the CPI and are available at the provincial level. For example, if average household spending on televisions remains the same over a period of ten years, it is assumed that this dollar amount represents the value of television equipment in a household, even if the CPI of an unchanging television set fell substantially.

The results of the SHS can be used to index the residential content value between two years in the same way as the CPI by using the weighted value of spending for the flood-affected categories. The procedure is demonstrated in Appendix 23.

8.1.3. Updating Non-Residential Content Damages

The contents of commercial, industrial, and institutional buildings susceptible to flood damage are not reflected by the CPI basket in either composition or weighting. Furthermore, spending surveys do not exist for non-residential categories and the assumed relationship between household spending and content value does not apply to commercial structures.

Without conducting new content surveys for each commercial structure category, a general index that avoids product-specific omission of quality changes is required. As part of the CPI, Statistics Canada provides the special aggregate “Goods” to exclude services, shelter, and energy that would not be affected by flooding. As the components of this aggregate are weighted by province according to the SHS, it can be assumed to represent the general composition of commercial contents, including non-durables that are insignificant in value at any one time in a household but may represent a significant value of commercial inventory.

Therefore, the following formula may be employed to update commercial content damages:

Current $ = Base Year $ X (Current CPI Goods Aggregate / Base CPI Goods Aggregate)

8.1.4. Updating Structural Damages

Structural flood damage is the estimated cost for repair and/or replacement of building components damaged by flooding. The price of construction/restoration is dependent on the building type. The main building type categories are:

- House (single dwellings, semi-detached, and row-houses);

- Apartment (vertical attached dwellings); and

- Non-Residential (commercial, industrial, and institutional).