Publication details

- ISBN

978-0-660-79962-9 - Catalogue number

M154-200/3-2025E-PDF

As stated in subsection 127.45(20) of the Income Tax Act, “for the purpose of determining whether a property is a clean technology property, any technical guide, published by the Department of Natural Resources and as amended from time to time, is to apply conclusively with respect to engineering and scientific matters”. This technical guide is with respect to the category of clean technology property that is electrical energy storage equipment.

This is the first edition of the Clean Technology (CT) Investment Tax Credit (ITC) Technical Guide: Electrical Energy Storage Equipment and it reflects the Income Tax Act and Income Tax Regulations current as of September 29, 2025.

The Class 43.1 and 43.2 Secretariat also maintains the Technical Guide to Class 43.1 and 43.2 and the Technical Guide to Canadian Renewable and Conservation Expenses (CRCE) under separate cover. Taxpayers are advised to consult those guides for specific information on the types of properties eligible for inclusion in Class 43.1 and/or CRCE.

This Guide may be amended from time to time to reflect amendments to the Income Tax Act and Income Tax Regulations with respect to clean technology property. Taxpayers should consult the latest versions of the Income Tax Act and Income Tax Regulations whenever they are considering a project to ensure that decisions are based on the legislation in force at the time.

General description

Electrical energy storage equipment (described in subparagraph (d)(ii) of the definition clean technology property in subsection 127.45(1) of the Income Tax Act, which references property described in subparagraph (d)(xviii) of Class 43.1 in Schedule II to the Income Tax Regulations) includes fixed location equipment that is used primarily for the purpose of storing and discharging electrical energy.

Electrical energy storage equipment where the electrical energy to be stored and discharged is not generated from electrical energy generation equipment described in Class 43.1 (e.g., photovoltaic electrical generation equipment described in subparagraph (d)(vi)) must have a roundtrip efficiency of greater than 50%. Please refer to the Additional Guidance section for more information.

Note: Not all electrical energy storage equipment described in Class 43.1 is eligible clean technology property for the purpose of the CT ITC. Refer to the Ineligible Properties section for applicable restrictions (underlined) on electrical energy storage equipment included in Class 43.1.

Eligible properties

Eligible properties for electrical energy storage equipment include the following:

- batteries;

- compressed air energy storage;

- flywheels;

- ancillary equipment (including control and conditioning equipment); and

- related structures.

Ineligible properties

Ineligible properties for electrical energy storage equipment include the following:

- equipment that uses any fossil fuel while in operation (please refer to the Additional Guidance section for more information);

- buildings;

- pumped hydroelectric storage;

- hydro electric dams and reservoirs;

- property used solely for backup electrical energy;

- batteries used in motor vehicles;

- fuel cell systems where the hydrogen is produced via steam reformation of methane; and

- property that would otherwise be included in Class 10 or certain parts of Class 17 (e.g., certain pieces of moveable equipment and portable tools, certain automotive equipment, electronic data processing equipment and system software, telephone and related equipment and access roads, sidewalks, parking areas, crane pads and other similar surface construction).

Additional guidance

In this section:

- General requirements

- Fixed location equipment

- Power conditioning equipment

- Equipment that uses any fossil fuel while in operation

- Round trip efficiency

- Thermal batteries

- Property used solely for backup electrical energy

General requirements

In order to qualify, in addition to other limitations, clean technology property must:

- Be equipment that is situated in and intended for use exclusively in Canada;

- Not have been previously used or acquired for use or lease, for any purpose before acquisition by the taxpayer; and

- Be acquired and become available for use between March 28, 2023 and December 31, 2034.

Fixed location equipment

Eligible electrical energy storage equipment must be installed in a manner that causes it to remain in a fixed location relative to the ground. Equipment affixed to a vehicle or other mobile object (like a trailer) is ineligible.

Power conditioning equipment

Eligible electrical energy storage equipment includes equipment that is used to condition incoming power for storage, or conversely, to condition discharged power for use or transmission. Power conditioning equipment may include bi-directional inverters, voltage transformers and equipment used for phase synchronization. Typically, the eligible boundary for electrical energy storage equipment is located beyond the power conditioning equipment at isolation switches used to lock out the electrical energy storage system.

Equipment that uses any fossil fuel while in operation

Eligible electrical energy storage equipment must be described in Class 43.1 and not use any fossil fuel in operation. This exclusion is not intended to apply to the electricity used to charge an electricity storage system, but rather to the direct use of fossil fuels by such a system.

Eligible electrical energy storage equipment may be charged with electrical energy from sources not described in Class 43.1 (e.g. a utility grid, a diesel generator, a gas-fired power plant) but it must meet the 50% round trip efficiency requirement.

Round trip efficiency

Roundtrip efficiency is the electrical energy output of an electrical energy storage system divided by the electrical energy input into the system, expressed as a percentage, and inclusive of all system losses and electrical inefficiencies involved in the storage of the electrical energy under normal conditions.

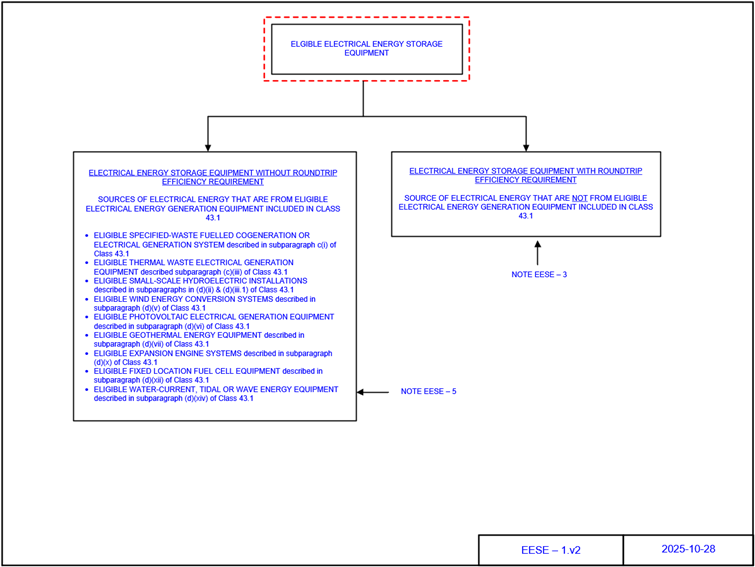

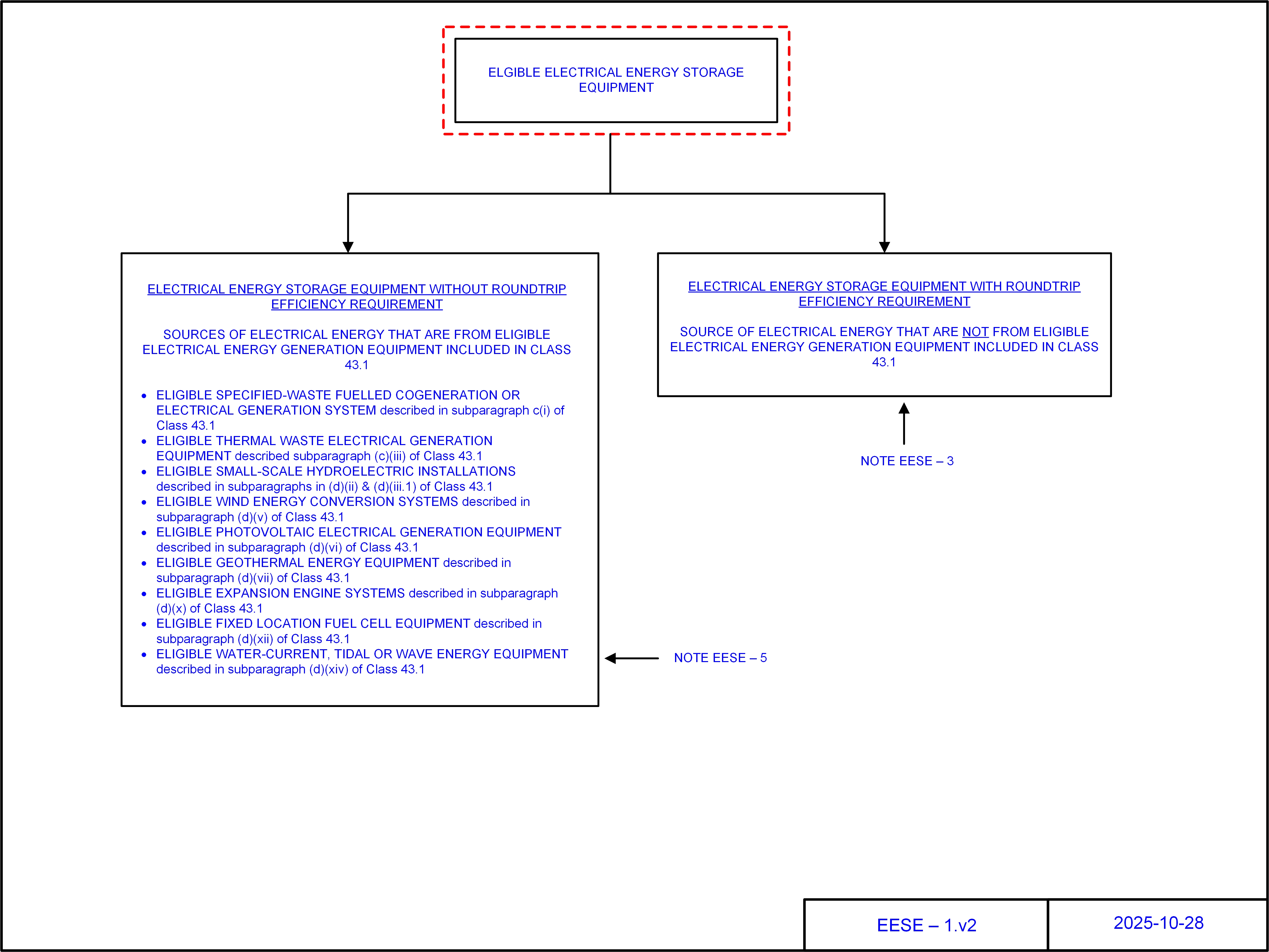

Figure 1 outlines the sources of electrical energy equipment that are described in Class 43.1 for which the roundtrip efficiency is not a consideration for the eligibility of electrical energy storage equipment.

Thermal batteries

Electrical energy storage equipment only qualifies as clean technology property if it both stores and discharges electrical energy. Fixed location energy storage property that discharges thermal energy does not qualify.

Property used solely for backup electrical energy

Electrical energy storage equipment may be used to provide backup electrical energy in the event of a power outage, but the equipment must also be actively used for some other purpose during normal operating conditions (e.g., peak shaving, load shifting, ancillary services etc.).

Costs typically included in capital cost of clean technology property

Costs typically included in the capital cost of electrical energy storage equipment that is clean technology property include:

- Construction of working platforms that are not an integral part of a building or other structure.

- Purchase and installation of battery storage equipment including battery modules, inverters, cooling systems and housings or enclosures that are not buildings.

- Purchase and installation of compressed air energy storage equipment including motors, compressors, expanders, generators, cooling and lubrication equipment, thermal storage equipment, heat exchangers, air filters, piping and compressed air storage vessels or well casings and well head equipment used in connection with geological compressed air energy storage systems.

- Purchase and installation of flywheel equipment including rotors, motor/generators, bearings, vacuum pumps, cooling systems and housings that are not buildings and the cost of vaults, structures or other civil works other than buildings that are required for the safe anchoring and containment of the flywheel equipment.

- Purchase and installation of ancillary power electronics, controls, instrumentation and safety equipment required to operate the electrical energy storage equipment.

- Purchase and installation of power transformers and switchgear equipment required for grid interconnection or integration with electrical generation equipment included in Class 43.1.

Note: The Department of Finance has published draft legislation in August 2024 that included proposed amendments to Section 127.45 that would provide that, for the purpose of computing a taxpayer’s CT ITC, the capital cost of clean technology property would not include any amount that is an expenditure in respect of a “preliminary work activity”. Once enacted, these amendments would apply retroactively as of March 28, 2023.

Proposed definition

Preliminary work activity means an activity that is preliminary to the acquisition, construction, fabrication or installation by or on behalf of a taxpayer of property including, but not limited to, a preliminary activity that is

- obtaining a right of access to a project site or obtaining permits or regulatory approvals (including conducting environmental assessments);

- performing front-end design or engineering work, including front-end engineering design studies, or process engineering work for the project, including

- collecting and analyzing of site data,

- calculating energy, mass, water or air balances,

- simulating and analyzing the performance and cost of process design options,

- selecting the optimum process design, and

- conducting feasibility studies or pre-feasibility studies;

- clearing or excavating land;

- constructing a temporary access road to the project site; or

- drilling of a well.

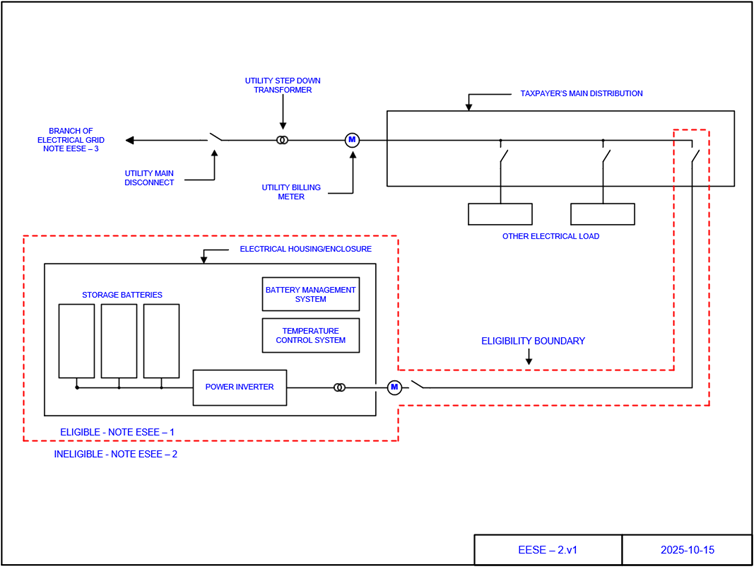

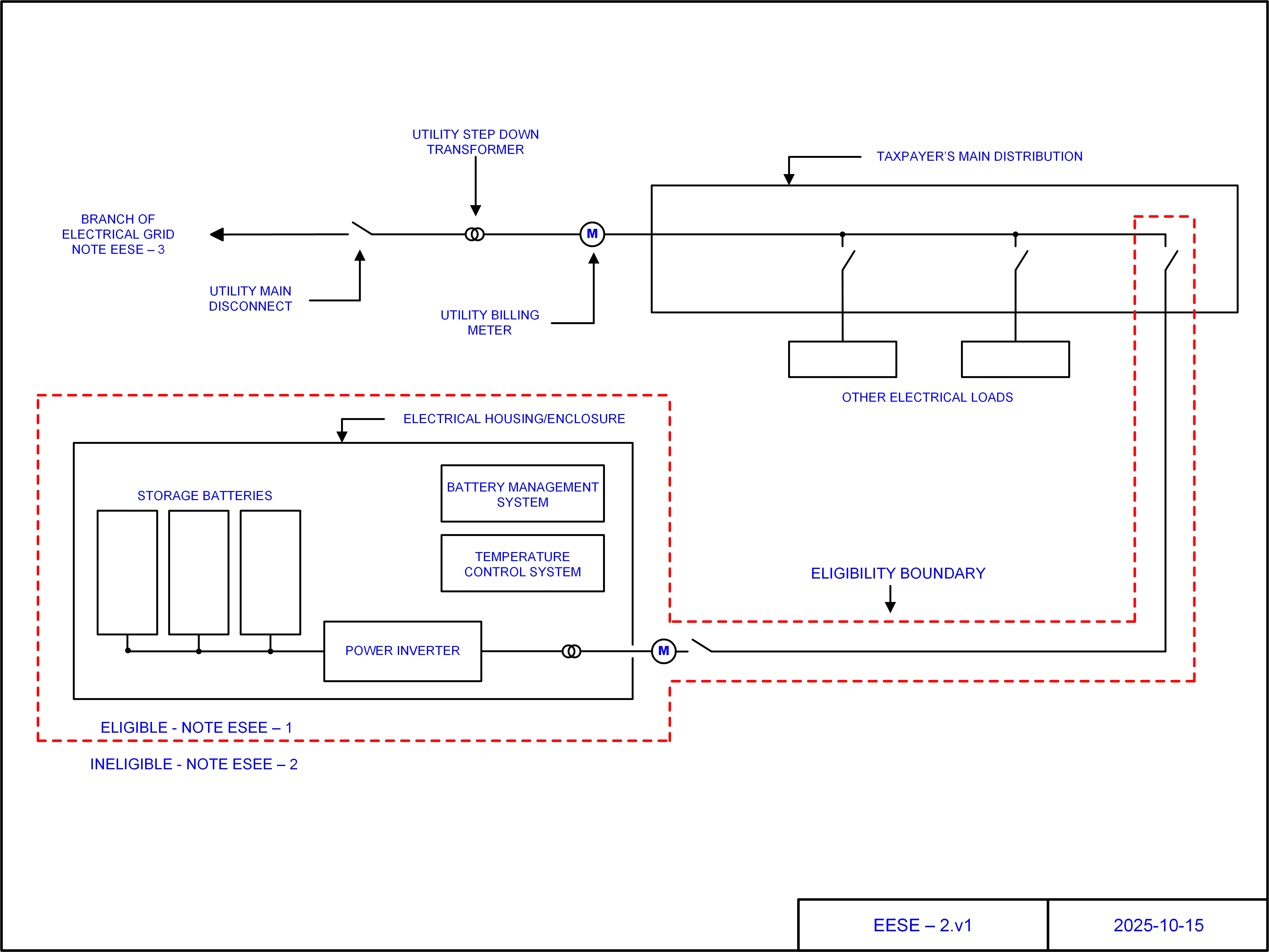

Schematics of qualifying systems

Typical configurations of components that would qualify as electrical energy storage equipment are shown in the schematics below.

Key to notes on schematics for electrical energy storage equipment

- EESE-1

- For eligible properties, see Eligible Properties section of this Guide.

- EESE-2

- For ineligible properties, see Ineligible Properties section of this Guide.

- EESE-3

- There is no roundtrip efficiency threshold for equipment that stores electrical energy that is generated by property described in Class 43.1. Other electrical energy storage equipment must have a roundtrip efficiency of 50% or more to be eligible clean technology property.

- EESE-4

- Eligible electrical energy storage property includes equipment used to discharge electrical energy and equipment used at the first level of power transformation. The first level of transformation includes equipment used for phase synchronization and voltage regulation. After the first level of transformation, the storage and subsequent discharge of electrical energy stops, and the electricity is ready for use (e.g., ready to be put on transmission lines). Typically, the eligible system boundary for electrical energy storage equipment is located after the first level of transformation at isolation switches that allow a utility to lock out a generating plant's power production.

- EESE-5

- If the electrical energy to be stored is generated by electrical energy generation equipment described in Class 43.1, the electrical energy storage equipment is eligible for the CT ITC regardless of its roundtrip efficiency.

Figure 1 - Sources of electrical energy that are equipment included in class 43.1 and not included in class 43.1

{kind=link}

Text version of Figure 1

Schematic illustrating the eligible electrical energy storage equipment, with or without roundtrip efficiency requirement. Electrical energy storage equipment does not require roundtrip efficiency requirement if the source of electrical energy originates from eligible electrical energy generation equipment included in Class 43.1. Electrical energy storage equipment must meet a roundtrip efficiency requirement if the source of electrical energy does not originate from eligible electrical energy generation equipment included in Class 43.1. For notes on this schematic (EESE-3 and EESE-5), please refer to key to notes on schematics for electrical energy storage equipment section.

Figure 2 - Battery electrical energy storage equipment used for peak/load shifting

{kind=link}

Text version of Figure 2

Schematic illustrating the boundary of a battery electrical energy storage equipment used for peak/load shifting. Within the boundary are storage batteries, power inverter, battery management system, temperature control system and transformer inside an electrical housing or enclosure, meter and the branch of electrical connection to the taxpayer’s main distribution. For notes on this schematic (ESEE-1 and ESEE-2), please refer to key to notes on schematics for electrical energy storage equipment section.

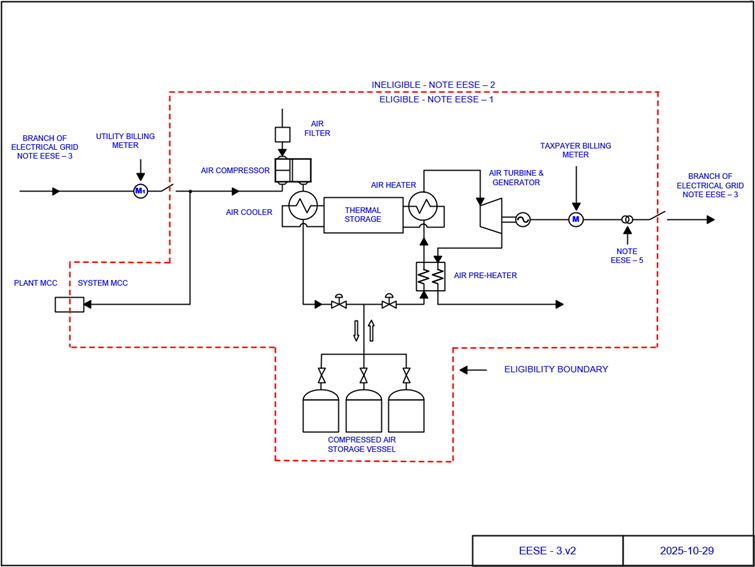

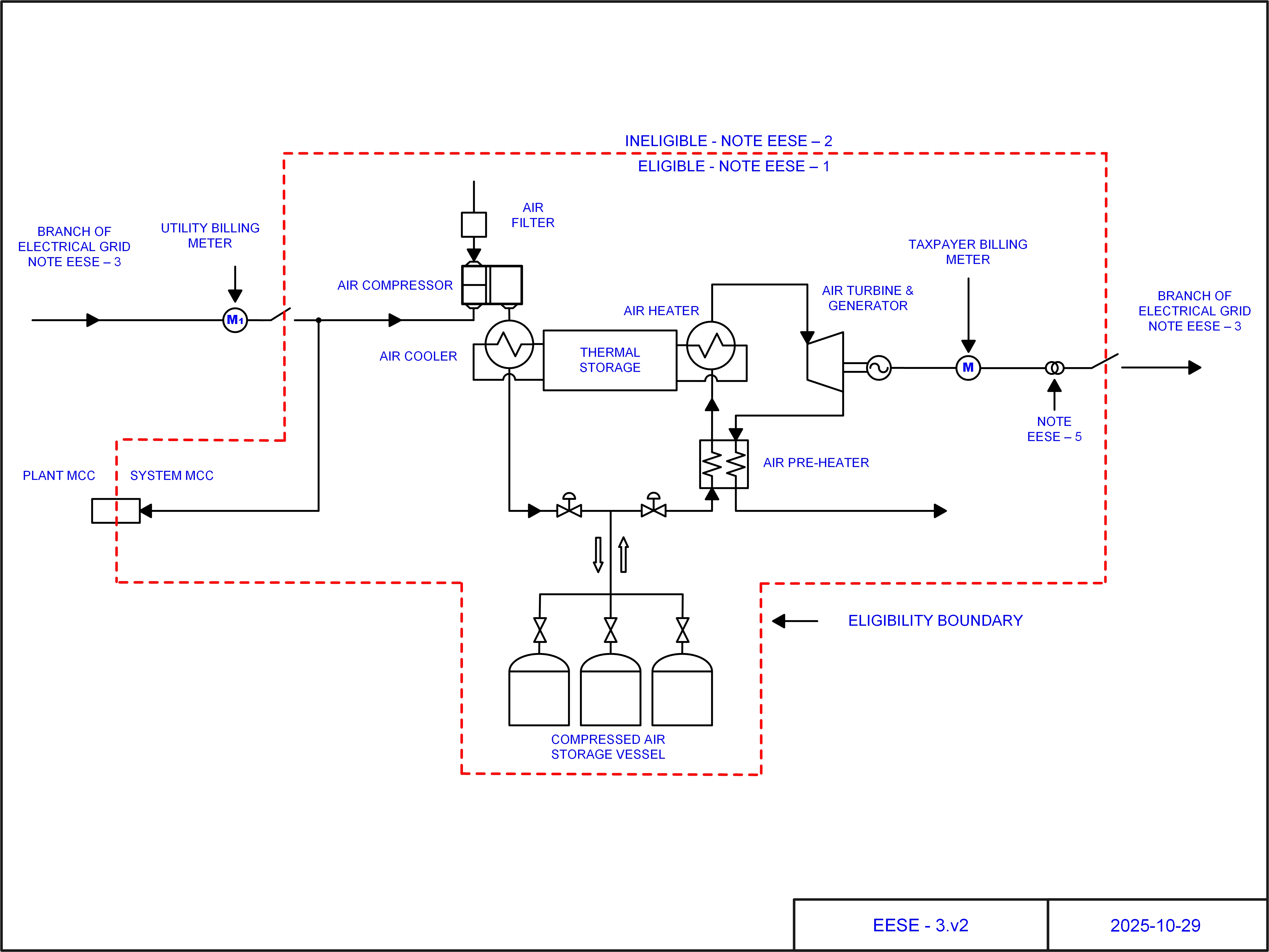

Figure 3 - Compressed air energy storage equipment

{kind=link}

Text version of Figure 3

Schematic illustrating the boundary of a compressed air energy storage equipment. Within the boundary are air filter, air compressor, air cooler, thermal storage, air heater, air turbine and generator, air pre-heater, compressed air storage vessel, meter and transformer. For notes on this schematic, please refer to key to notes on schematics for electrical energy storage equipment section.

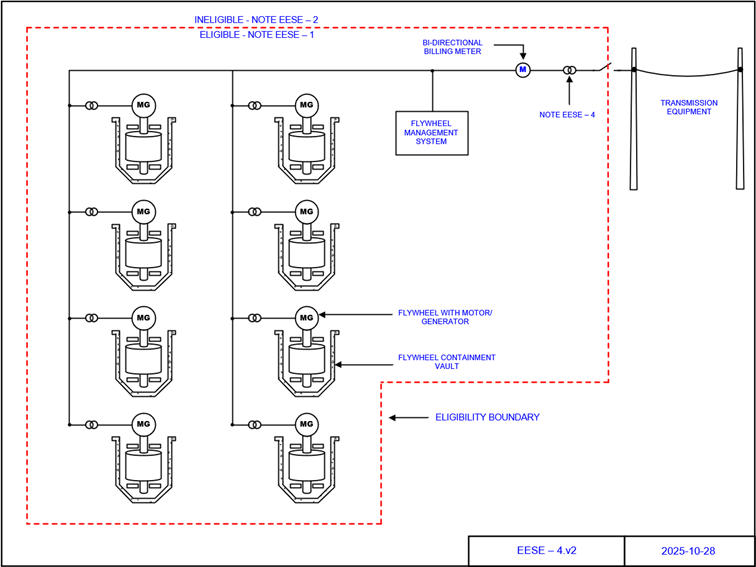

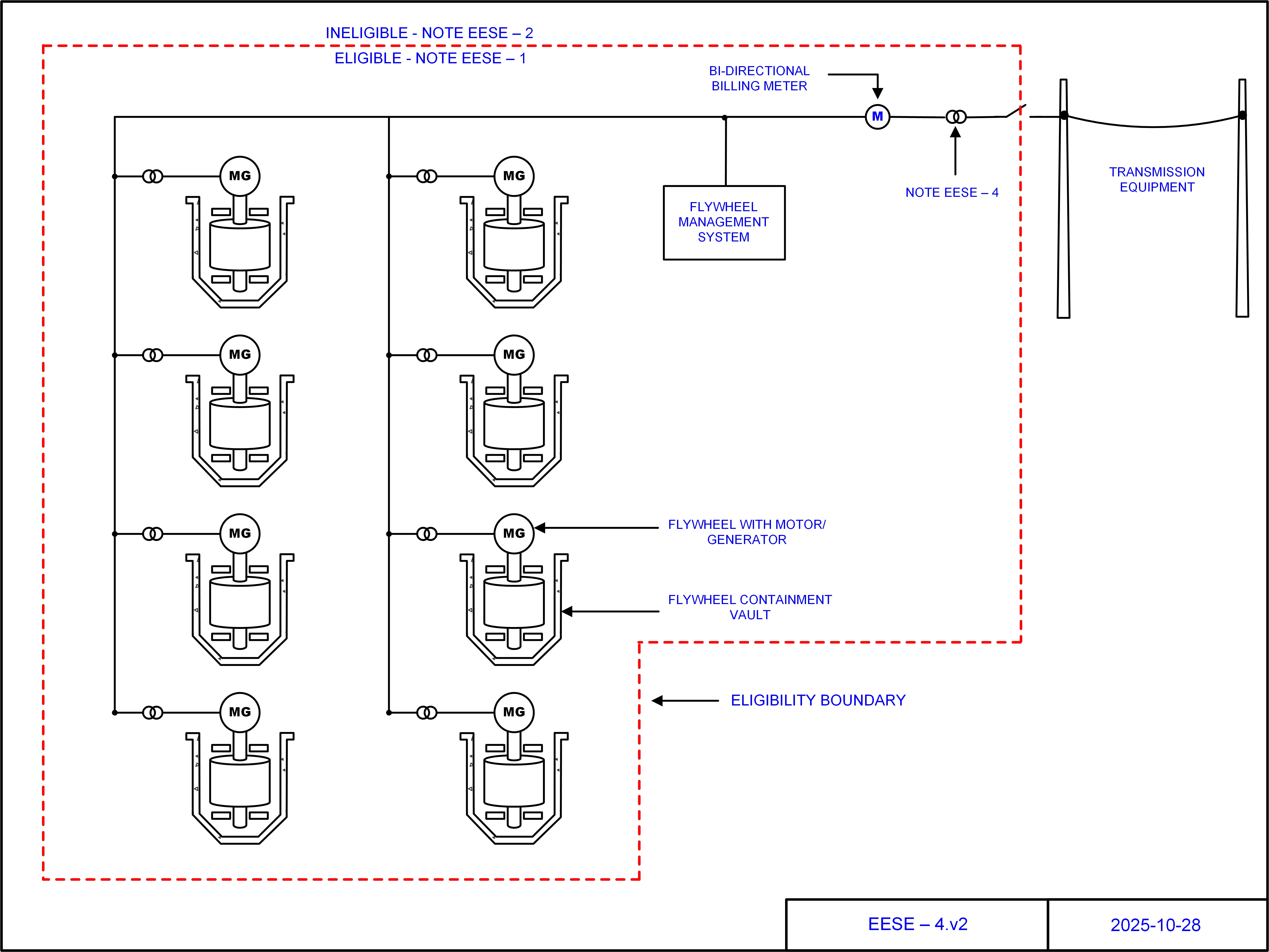

Figure 4 - Flywheel energy storage equipment

{kind=link}

Text version of Figure 4

Schematic illustrating the boundary of a flywheel energy storage equipment. Within the boundary are flywheel containment vault, motor/ generator, transformer and management system, bi-directional billing meter and transformer. For notes on this schematic, please refer to key to notes on schematics for electrical energy storage equipment section.