Audit of NRCan’s Grants and Contributions Processes and Activities (AU1602)

Audit Branch

Natural Resources Canada

Presented to the Departmental Audit Committee (DAC)

March 2016

TABLE OF CONTENTS

EXECUTIVE SUMMARY

INTRODUCTION

Grants and Contributions (Gs&Cs) programs are one of the key instruments used by the Government of Canada (Government) to further its broad policy objectives and priorities. Gs&Cs programs are a mechanism through which the Government transfers funds to other organizations and individuals thereby enabling and engaging a wide diversity of skills and resources outside the federal government. Transfer payments made through Gs&Cs programs are a major commitment of federal government resources and must be managed accordingly. The objective of the Treasury Board (TB) Policy on Transfer Payments is to ensure that Gs&Cs programs are managed with integrity, transparency and accountability in a manner that is sensitive to risk, are citizen and recipient-focused, and are designed and delivered to address government priorities in achieving results for Canadians.

Gs&Cs programs play a vital role in ensuring that Natural Resources Canada (NRCan) delivers on its responsibilities and helps drive progress on natural resource issues important to Canadians such as clean and renewable energy technologies, and sustainable natural resource development. Through programs such as ecoENERGY for Renewable Power, Investments in Forest Industry Transformation, and the Targeted Geoscience Initiative, amongst others, NRCan provides financial contributions and support to Canadian organizations related to natural resources to help develop their markets and sustain economic growth.

NRCan Sectors are supported in the management of Gs&Cs programs by the departmental Centre of Expertise on Gs&Cs (CoE), established within NRCan’s Finance and Procurement Branch. The CoE ensures that program managers have the tools, advice, and direction needed to manage Gs&Cs programs and provides a central monitoring function. Oversight and strategic advice on the management of Gs&Cs programs is provided by the Transfer Payment Review Committee (TPRC).

The overall purpose of the audit was to provide reasonable assurance on the adequacy and effectiveness of the Department’s corporate Gs&Cs processes and activities, including risk management, controls and governance, in accordance with the TB Policy on Transfer Payments.

STRENGTHS

Overall, the audit found that the Department had designed and implemented governance structures for the management of Gs&Cs programs. The Department has adequate controls in place to support compliance with the requirements of the TB Policy on Transfer Payments. The Department has also established transparent and standardized processes for the management, performance measurement and reporting of Gs&Cs programs.

AREAS FOR IMPROVEMENT

The audit identified opportunities to evaluate the role of the TPRC to ensure clarity of accountabilities and that oversight focuses on areas of significant risk, that administrative processes are proportionate to the level of risk and reflect engagement with stakeholders, and to improve the collaboration and sharing of best practices within NRCan.

INTERNAL AUDIT CONCLUSION AND OPINION

In my opinion, overall, the Department has adequate processes and activities in place to support the management of Gs&Cs programs. Opportunities exist to further strengthen the effectiveness of certain processes and activities, including evaluating the role of the TPRC and supporting administrative processes, and improving collaboration and sharing of best practices within the Department.

I encourage the Department to continue its efforts to bring innovation and cost-effective improvements to Gs&Cs programs.

STATEMENT OF CONFORMANCE

In my professional judgement as Chief Audit Executive, the audit conforms with the Internal Auditing Standards for the Government of Canada, as supported by the results of the Quality Assurance and Improvement Program.

Christian Asselin, CPA, CA, CMA, CFE

Chief Audit Executive

March 10, 2016

ACKNOWLEDGEMENTS

The audit team would like to thank those individuals who contributed to this project and particularly employees who provided insights and comments as part of this audit.

INTRODUCTION

Grants and contributions (Gs&Cs) programs are one of the key instruments used by the Government of Canada (Government) to further its broad policy objectives and priorities. Gs&Cs programs are a mechanism through which the Government transfers funds to other organizations and individuals thereby enabling and engaging a wide diversity of skills and resources outside the federal government. Transfer payments made through Gs&Cs programs are a major commitment of federal government resources and must be managed accordingly. The objective of the Treasury Board (TB) Policy on Transfer Payments is to ensure that Gs&Cs programs are managed with integrity, transparency and accountability in a manner that is sensitive to risks, are citizen and recipient-focused, and are designed and delivered to address Government priorities in achieving results for Canadians.

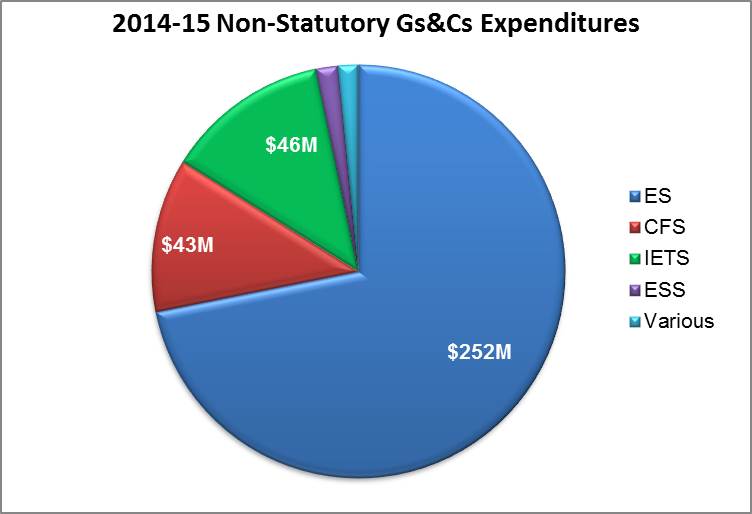

Gs&Cs programs play a vital role in ensuring that Natural Resources Canada (NRCan) delivers on its responsibilities and helps drive progress on natural resource issues important to Canadians such as clean and renewable energy technologies, and sustainable natural resource development. Through programs such as ecoENERGY for Renewable Power, Investments in Forest Industry Transformation, and the Targeted Geoscience Initiative, amongst others, NRCan provides financial contributions and support to organizations related to natural resources to help develop their markets and sustain economic growth. In 2014-15, NRCan spent $353 million on 23 non-statutory Gs&Cs programs of which the Energy Sector (ES), the Canadian Forest Service Sector (CFS), and the Innovation & EnergyTechnology Sector (IETS) accounted for approximately 97%. The remaining 3% reflects Gs&Cs program expenditures in all NRCan Sectors including the Earth Sciences Sector (ESS), and the Minerals and Metals Sector (MMS).

This figure illustrates the distribution by Sector of NRCan's non-statutory Gs&Cs in fiscal year 2014-15, which amounted to a total of $353M. The distribution of spending is as follows: $252 million for the Energy Sector (ES), $46 million for the Innovation & Energy Technology Sector (IETS) , $43M for the Canadian Forest Service Sector (CFS), and the remaining $12M was spent for various sectors including the Earth Sciences Sector (ESS) and the Minerals and Metals Sector (MMS).

Sectors are supported in the management of Gs&Cs programs by the departmental Centre of Expertise on Gs&Cs (CoE), established within NRCan’s Finance and Procurement Branch (FPB). The CoE ensures that Program managers have the tools, advice, and direction needed to manage Gs&Cs programs and provides a central monitoring function. Oversight and strategic advice on the management of Gs&Cs programs is provided by the Transfer Payment Review Committee (TPRC).

NRCan’s non-statutory Gs&Cs program expenditures decreased from $1,347 million in 2010-11 to $353 million in 2014-15.

_Eng.jpg)

This figure illustrates the decrease in NRCan's non-statutory Gs&Cs expenditures between 2010-11 and 2014-15 as follows: 1,347 million in 2010-11, $1,286 million in 2011-12, $423 million in 2012-13, $401 million in 2013-14, and $353 million in 2014-15.

The audit of NRCan’s Gs&Cs Processes and Activities was included in the Department’s 2015-2018 Risk- Based Audit Plan, approved by the Deputy Minister on March 12, 2015.

AUDIT PURPOSE AND OBJECTIVES

The overall purpose of the audit was to provide reasonable assurance on the adequacy and effectiveness of the Department’s corporate Gs&Cs processes and activities, including risk management, controls and governance, in accordance with the TB Policy on Transfer Payments. The audit looked at the processes and activities of the management of Gs&Cs across the Department, specifically whether:

- The Department has designed and implemented effective governance structures and processes for Gs&Cs programs.

- Adequate and effective controls are in place to support compliance with the new requirements of the TB Policy on Transfer Payments relating to Gs&Cs program harmonization, risk management, and the establishment of departmental service standards.

- Processes and activities related to the management, performance measurement and reporting of Gs&Cs programs are adequate, transparent and standardized where possible.

AUDIT CONSIDERATIONS

A risk-based approach was used in establishing the objectives, scope and approach to this audit engagement. A summary of the potential key areas of risk taken into consideration are:

- Effective governance structures and processes have been established to support the management of Gs&Cs programs.

- Adequacy and effectiveness of controls and processes necessary for compliance with the requirements of the TB Policy on Transfer Payments and NRCan’s policies related to Gs&Cs.

- Effectiveness of monitoring processes, including performance measurement and providing sufficient information for senior management decision making.

SCOPE

The audit focussed on corporate level processes and activities that were in place to support the Department’s Gs&Cs programs during the 2013-14 and 2014-15 fiscal years.

The audit also provided assurance on the effectiveness of specific key controls for the programs selected. Specifically, the audit considered the processes and activities of the administration of the Gs&Cs programs across the Department including Program monitoring, clarity and application of the repayable contribution clause in contribution agreements, an assessment of the financial system for timeliness and accuracy, and the general Program approach to select recipients for funding. The audit did not include performing a business needs analysis of the current Gs&Cs financial systems.

APPROACH AND METHODOLOGY

The audit was conducted in accordance with the TB Policy on Internal Audit and Government of Canada Internal Audit Standards and entailed:

- Reviewing relevant policy instruments and business processes;

- Reviewing key documents and relevant background information, including recommendations made in previous audit reports related to Gs&Cs programs;

- Consulting with other federal departments and considering their relevant audits;

- Conducting interviews with key personnel; and,

- Analysis and testing of data utilized for the management of Gs&Cs, including performance measurement, financial and non-financial information.

The conduct phase of this audit was substantially completed in December 2015.

CRITERIA

Please refer to Appendix A for the detailed audit criteria. The criteria guided the audit fieldwork and formed the basis for the overall audit conclusion.

FINDINGS AND RECOMMENDATIONS

Governance Structures and Processes

Summary Finding

The Department has designed and implemented governance structures for the management of Gs&Cs programs. Governance bodies provide leadership and oversight, while also monitoring the overall state of NRCan’s Gs&Cs, including compliance with the TB Policy on Transfer Payments and NRCan policies. Efforts have been made to streamline Gs&Cs administrative processes, and service standards have been established, monitored and the results reported to senior management. Collaboration exists internally and with other departments to achieve efficiency and reduce duplication of effort.

Opportunities exist to evaluate the role of the TPRC and the Gs&Cs risk assessment methodology to ensure that processes for endorsing and amending agreements are proportionate to the level of risk associated with the agreement and action required, and to establish greater collaboration and sharing of best practices regarding the management of Gs&Cs amongst NRCan’s Sectors.

Supporting Observations

The audit sought to determine whether the Department has designed and implemented effective governance structures and processes supporting Gs&Cs program management. Such processes ensure there is clarity of roles, responsibilities and accountabilities among stakeholders and that governance bodies are providing a leadership, oversight and challenge function. The audit also sought to determine whether the Department has adequate and effective controls in place, including monitoring, to support compliance with the requirements of the TB Policy on Transfer Payments. Specifically, the audit sought to determine whether collaboration exists within NRCan and with other departments to harmonize Gs&Cs programs and to standardize administration to achieve efficiencies. The audit also sought to determine whether processes are in place to ensure that administrative requirements are proportionate to the level of risk and are streamlined through engagement with recipients and stakeholders; and reasonable and practical service standards have been established, are monitored and their results are reported for decision making.

Roles, responsibilities, and accountabilities

Overall, the audit confirmed that roles, responsibilities and accountabilities regarding the management of Gs&Cs programs are defined and communicated through the departmental website and policies. Key players include the TPRC, the Centre of Expertise on Gs&Cs (CoE), Assistant Deputy Ministers (ADMs), and Program employees.

The TPRC is an ADM-level advisory and oversight committee that supports the Executive Committee and the Deputy Minister with the intent of applying an integrated risk-based approach to the management of Gs&Cs, while fostering transparency and accountability. Under its current Terms of Reference, the TPRC is responsible for: (1) reviewing transfer payment program design proposals or proposals for modification of existing transfer payment programs at the Treasury Board Submission stage; (2) reviewing agreements and amendments for endorsement where they fall under pre-defined criteria; and (3) monitoring the overall state of NRCan’s Gs&Cs, including findings from Office of the Auditor General (OAG) audits of Public Accounts, internal audits and evaluations and other relevant findings. It is important to note that although the TPRC reviews agreements for endorsement, it is the Sector ADMs who are ultimately accountable for the agreements that are signed within their respective Sectors.

Each Sector has also established its own governance structures to support the day-to-day management of Gs&Cs programs. Sector employees perform various due diligence activities to ensure transparency and accountability around the approval of Gs&Cs funding covering three key aspects: technical, administrative and financial.

The CoE provides a departmental corporate quality assurance function supporting the TPRC, through incremental agreement review prior to agreements being presented to TPRC for endorsement, and reporting of monitoring activities. The CoE’s other key responsibilities include: fostering a collaborative culture among Gs&Cs program managers, liaising with central agencies and directing the implementation of departmental Gs&Cs initiatives, providing advice to employees on the administration of Gs&Cs programs, and providing various tools and training to support the management of Gs&Cs.

Leadership, oversight and challenge provided by governance bodies

Overall, the audit confirmed that the TPRC is providing leadership, oversight and a challenge function regarding the design of Gs&Cs programs, and funding agreements. It also plays an advisory role regarding compliance with the TB Policy on Transfer Payments and NRCan policies. The audit noted that the focus of the TPRC has been on reviewing and endorsing agreements and amendments, with the majority (approximately 80%) of these being identified as ‘low risk’ by Program management. The current criteria for agreements to require TPRC review and endorsement are based on a combination of materiality and risk level (as assessed under the departmental risk methodology); however, the materiality level had been set low enough that, in general, the majority of agreements going to TPRC are based primarily on dollar value. In addition, many of the files sent for TPRC discussion were concerning administrative amendments to contribution agreements, including changes to dates and standard reallocation of funds between categories. Terms and Conditions of individual agreements currently do not have built-in flexibility to allow for minor changes to be made without requiring an amendment, which often incurs substantial incremental administrative processes.

Interviews with various representatives from senior management and program staff confirmed that there was limited value added in having the TPRC endorse ‘low risk’ agreements and amendments, particularly as Sector ADMs are ultimately accountable for the agreements that are signed. Furthermore, the additional documentation requirements and preparation required for presentation of an agreement or amendment at TPRC adds several weeks to the overall approval process, and places additional time burden on the CoE, Program managers and TPRC members. This situation creates delays and inefficiencies that could impact the Department’s ability to achieve program objectives.

It should be noted that, to address the above-mentioned challenges, CoE has recently designed initiatives to reduce administrative burden, reflecting engagement with program management. Examples include streamlining the process for certain administrative amendments, and increasing the TPRC review threshold from $1M to $2M.

Collaboration within NRCan and with other departments

In recent years, the Department has collaborated with other government departments to harmonize Gs&Cs programs and to standardize administration to achieve efficiencies and avoid duplication of efforts where possible. Examples include the collaboration between NRCan and Environment Canada through the Canada’s Biofuels Strategy established in 2007, and the interdepartmental governance committees for some of NRCan’s Gs&Cs programs. The Director of the CoE also participates in a TB led Director/Director General working group supporting collaboration and harmonization across Government.

The audit found that collaboration and sharing of best practices within the Department could be improved, particularly in areas such as program design, developing program Terms & Conditions for Gs&Cs and developing performance measures. A ‘Gs&Cs Management Reform – Consultation Team’ exists that is chaired by the Director of the CoE. This forum met infrequently during the last two years due to capacity constraints.

Gs&Cs Service Standards

The Department has established service standards for all Gs&Cs programs approved after March 31, 2010. Certain older Gs&Cs programs, because of “sunsetting” or expiring, are under less pressure to develop service standards. The Department is monitoring the service standards implementation and reporting the results to senior management to provide insight and direction. The Department’s recent initiatives to reduce administrative burden both internally and externally should have a positive impact on programs’ service standards.

RISK AND IMPACT

Failure of the Department’s governance processes and structures to clearly identify accountabilities would impact the oversight, leadership and implementation of Gs&Cs processes and activities. Moreover, overburdened governance processes regarding low risk files reduces senior management time and focus on providing oversight and leadership on areas of greater risk and significance. Where Gs&Cs processes are not designed in a manner that is sensitive to risks, there is a risk that additional administrative burden could cause delays that ultimately impact whether programs are able to meet their objectives. Ineffective collaboration and a lack of sharing of best practices within the Department could result in inconsistent management of Gs&Cs programs.

RECOMMENDATIONS

1. It is recommended that the Assistant Deputy Minister (ADM) Corporate Management Services Sector (CMSS), in collaboration with Transfer Payment Review Committee (TPRC) members:

- Evaluate the role of the TPRC to ensure that accountabilities are clear, that the TPRC’s activities add value to the overall management of Gs&Cs and promotes collaboration and sharing of best practices across the Department;

- Review and revise the Gs&Cs risk assessment methodology, including materiality levels to determine risk; and,

- Review and revise current Gs&Cs administrative processes, particularly with regards to endorsing and amending agreements, to ensure they are proportionate to the level of risk associated with the agreement and action required.

MANAGEMENT RESPONSE AND ACTION PLAN

Management agrees. In response to recommendation 1, the recommendation aligns with current plans underway to review the overall management of Gs&Cs, including the role of TPRC.

- ADM CMSS, in collaboration with TPRC members, will reflect on the scope of the TPRC, including clarification of roles & responsibilities, and opportunities to promote collaboration & share best practices. This revision is also supported by the ongoing Departmental Grants & Contributions Discussion Forum (GCDF); a group comprised of Program representatives and functional experts. The GCDF will begin meeting on a more regular basis moving forward, providing a forum for the exchange of experiences, tools and best practices. Further, the CoE will continue to offer ongoing consultations with Program Officers.

Deliverable 1: Revised TPRC Terms of Reference (ToR)

Timing: Q2 (September 31), FY 2016-17

Deliverable 2: Revised GCDF ToR

Timing: January 8, 2016 (Completed)

- ADM CMSS, in collaboration with TPRC members, has already undertaken a thorough review of the departmental Gs&Cs Risk Assessment (RA) methodology and supporting guidance framework, including consultations with Other Government Departments (OGDs), and comparisons with their RA framework. This has resulted in the implementation of three additional risk factors. This Tool has been evaluated by programs to ensure applicability, and is currently available to Programs, with training scheduled for this Fiscal Year.

Deliverable: Updated RA Tool

Timing: September 14, 2015 (Completed)

Deliverable: Supporting RA Tool Training

Timing: Q4 (March 31) FY 2015-16

- ADM CMSS, in collaboration with TPRC members, has introduced revisions to the Gs&Cs amendment process, particularly with regard to endorsing and amending agreements. These process busting efforts have been implemented.

Deliverable: Administrative/Minor Amendments and Novations Process for Contribution Agreements – Update

Timing: December 23, 2015 (Completed)

Business Processes

Summary Finding

The Department has established transparent and standardized processes for the management, performance measurement and reporting of Gs&Cs programs. Opportunities for improvement exist to strengthen training and tools to support effective management of Gs&Cs programs, including monitoring repayable contributions and proactive disclosure by the respective programs.

Supporting Observations

The audit sought to determine whether the Department has established standard procedures and processes for management of Gs&Cs programs that are consistently applied, including processes related to application assessment, performance measurement, and reporting; and effective management of real, apparent or potential conflicts of interest. The audit also sought to determine whether policies, tools, guidance and training have been developed and implemented to support effective management of Gs&Cs programs.

Program visibility, application assessment and management of conflict of interest

Processes have been established to ensure that potential recipients have ready access to information about programs. The Department's external website includes a description of each program, its eligibility requirements, the application process, examples of current approved projects, and contact information for follow-up questions. The audit also found that programs had established clear processes for the assessment of project applications through use of program guides, and evaluation tools. These tools were used by evaluation panels/committees to evaluate applications received. Most of these panels/committees included external members, further supporting a fair and transparent assessment process.

To effectively manage and report real, apparent or potential conflicts of interest (CoI), the Department has developed various internal procedures, guidelines, and tools to guide and assist employees. The Department’s Values and Ethics Centre of Expertise provides general training on CoI to all employees, and is well positioned to provide specific guidance on real and potential CoI situations when engaged by the programs. One of the primary tools used specifically for Gs&Cs programs, developed by the CoE, is the attestation regarding consideration of CoI that is required to be completed by program management prior to signing an agreement. The audit noted that, for the sample of Gs&Cs agreements examined, attestations on CoI were consistently completed to ensure that real, apparent and potential conflicts of interest are handled appropriately.

Standard procedures and processes for management of Gs&Cs programs

The Department has developed standard procedures and processes for the full life-cycle of Gs&Cs. The audit found that, for the most part, these procedures have been followed consistently by the programs. The CoE monitors the application of standard procedures to ensure consistency across the Department. One area where opportunities for improvement were noted relates to repayable contributions.

A repayable contribution is a contribution, all or part of which, is repayable or conditionally repayable according to the terms of the contribution agreement. By design, some contributions are required to be repaid and some are not. Treasury Board Policy stipulates whether repayment is to be made in whole or in part based on specific criteria and conditions including, for example, a lack of profit from the funded project. In general, contributions made to for-profit businesses that are intended to allow the businesses to generate profits or increase the value of the businesses are to be repayable. For science & technology programs in general, projects are not expected to become profitable in the short or even medium term, given the lengthy delays between demonstration and market adoption. This delay is typically in the order of 10-20 years or more. Contribution agreements often include a repayability clause, to cover the exceptional cases where technologies are rapidly taken up in the market and recipients, in those cases, achieve profitability within 5-10 years. An example of a repayable contribution program at NRCan is the Wind Power Production Incentive Contribution Program that was set up to help establish wind energy in Canada by providing a financial incentive of approximately 1 cent per kilowatt-hour, which could become repayable based on the market value of electricity.

Responsibility for monitoring repayable contributions resides within the programs. Consistent with previous audits of repayable contributions, the audit found that repayable contributions could be monitored more effectively by programs. Where repayability has been included as a feature of a program there can be considerable administrative burden in monitoring a company’s profits for 5 to 10 years after a project has ended, particularly where there is no intention or expectation that projects will contribute to companies’ profits. Upon further examination, it was observed that certain contribution programs had been designed to include the feature of repayability without documented analysis demonstrating whether this feature was necessary or relevant. The audit noted that there is an opportunity during the design of future programs for further analysis to be conducted of the repayability feature and clauses; and develop such clauses through consultation with Legal Services and other relevant stakeholders. This would ensure that such clauses are included when relevant, with appropriate thresholds triggering repayment for projects that become commercialized, and consider legal requirements and obligations, such as compliance with trade agreements.

NRCan Policies, guidance, tools and training of Gs&Cs programs

The CoE has developed and implemented various policies, guidance documents, and tools to support Gs&Cs programs. The audit noted that the NRCan Policy on Transfer Payments, and related Directives and guidance are currently being updated to reflect the 2012 TB Policy on Transfer Payments; and, aligned to better support programs by providing clearer requirements, removing duplication and reducing administrative burden.

The Agreements Module & SAP Interfaces (AMI) corporate application is one of the tools available to program management for managing Gs&Cs agreements. Program management is responsible for entering information on Gs&Cs agreements into AMI, and the CoE uses this information for various purposes such as monitoring and uploading proactive disclosure information on the Internet. The audit found that program management is not using AMI consistently and often uses external databases/tools to meet program needs, entering only the mandatory information in AMI. Late reporting of Gs&Cs agreements and amendments for proactive disclosure was also identified as a recurring issue by the CoE through its quarterly monitoring activities and occurs for various reasons, such as information not being entered accurately to begin with, or other similar delays in the approval process by Program Management. The CoE has actively followed up with program managers to remind them of their duties regarding disclosure. Delays in updating AMI may result in inaccurate disclosure.

The CoE provides training to program personnel on the use of the Gs&Cs Risk Tool, as well as drafting standard non-repayable contribution agreements several times a year. The CoE also provides training on an as-needed basis when requested by management. Interviews with various program managers indicated that standard training provided by the CoE could be enhanced to better meet their current needs, which go beyond drafting basic contribution agreements.

Performance measurement strategies for Gs&Cs programs

The Department has established and maintained performance measurement strategies for Gs&Cs programs. Performance measures for each of the programs examined had been aligned with the departmental priorities and objectives. The performance measurement results of the Gs&Cs programs are reported to management on a regular basis and form input to Departmental Performance Reports. Program managers recognize the role of Strategic Evaluation to support the programs in further improving performance measurement strategies.

RISK AND IMPACT

Inconsistent application of policy and utilization of standard tools could result in the perception of a lack of transparency in the management of the Department’s transfer payment programs. The Department may encounter issues in delivering its Gs&Cs programs in compliance with the TB Policy on Transfer Payments.

RECOMMENDATIONS

2. It is recommended that the Director General, Finance and Procurement Branch – Corporate Management and Services Sector (CMSS) enhance its training offerings by evaluating the current training and tools provided on Gs&Cs through engagement with program managers, and customize training and tools based on Programs’ feedback to meet the needs of the Department.

3. It is recommended that Sector Assistant Deputy Ministers (ADMs) ensure that an analysis is conducted when designing new Programs, in consultation with Legal Services and other relevant stakeholders, to determine whether or not repayability should be a Program design element and if so ensure the clauses are both relevant and reasonable.

4. It is recommended that Sector Director Generals ensure the timely capture of information within the Agreements Module Interface (AMI) to support proactive disclosure.

MANAGEMENT RESPONSE AND ACTION PLAN

Management agrees. In response to recommendation 2, this recommendation aligns with current plans underway to reflect upon current offerings by the Branch. As part of the Department’s revision to Gs&Cs Management, the Director General, Finance and Procurement Branch – Corporate Management and Services Sector, in collaboration with the Centre of Expertise (CoE), has reviewed the existing departmental policy and guides, and is creating a new and updated NRCan Transfer Payment Guide & Standard Operating Procedures. The new guidance will be consistent with recent changes made to the risk assessment tool, as required.To further training offerings, the Department will bring to the Departmental Grants & Contributions Discussion Forum (GCDF) relevant Gs&Cs topics and tools to support engagement, gain insight and share knowledge.

Deliverable 1: Revised NRCan Transfer Payments Guide and Standing Operating Procedures (SOPs)

Timing: Q4 (March 31), FY 2016-17

Deliverable 2: Review approach to offering guidance

Timing: Q3 (December 31), FY 2016-17

Management agrees. In response to recommendation 3, the Program Sector ADMs, in consultation with the CoE, will ensure that a documented analysis, considering consultations with legal services and other relevant stakeholders, is prepared during the design of new Programs to determine whether or not repayability should be included as an element in order to ensure that the clauses are relevant, reasonable, and administratively cost effective.

Positions responsible: Program Assistant Deputy Ministers

Timing: March 2016

Management agrees. In response to recommendation 4, the Sector DGs will ensure that reconciliation/verification processes are performed and appropriate information recorded in AMI, to ensure that all contribution agreements and material amendments are proactively disclosed on the Departmental website in a timely manner.

Positions responsible: Sector Director Generals

Timing: March 2016

APPENDIX A – AUDIT CRITERIA

The overall purpose of the audit was to provide reasonable assurance on the adequacy and effectiveness of the Department’s corporate Gs&Cs processes and activities, including risk management, controls and governance, in accordance with the Treasury Board’s Policy on Transfer Payments. The audit also looked at the processes and activities of the management of Gs&Cs across the Department.

The following audit criteria were used to conduct the audit:

| Audit Sub-Objectives | Audit Criteria |

|---|---|

| 1. The Department has designed and implemented effective governance structures and processes for Gs&Cs programs. | 1.1 Roles, responsibilities, and accountabilities are clearly defined and communicated. |

| 1.2 The governance bodies are providing a leadership, oversight and challenge function. | |

| 1.3 Compliance with the Treasury Board Policy on Transfer Payments and NRCan policies is monitored to ensure effective implementation. | |

| 2. Adequate and effective controls are in place to support compliance with the requirements of the TB Policy on Transfer Payments, including program harmonization, risk management, and the establishment of departmental service standards. |

2.1 Collaboration exists within NRCan and with other departments to harmonize Gs&Cs programs and to standardize administration to achieve efficiencies. |

| 2.2 Processes are in place to ensure that Gs&Cs administrative requirements are proportionate to the level of risk and are streamlined through engagement with recipients and stakeholders. | |

| 2.3 Reasonable and practical service standards have been established, are monitored, and their results are reported for decision-making. | |

| 3. Effective processes and activities related to the management, performance measurement and reporting of Gs&Cs programs are adequate, transparent, and standardized where possible. | 3.1 Processes are in place to ensure that potential recipients have ready access to information about programs and that the assessment of recipient applications is conducted through an open process and supported by transparent controls. |

| 3.2 Effective standard procedures and processes for management of Gs&Cs programs are consistently applied. | |

| 3.3 Tools, guidance and training have been developed and implemented to support effective management of Gs&Cs programs. | |

| 3.4 Performance measurement strategies are established, maintained and reported to effectively support the evaluation of the relevance of Gs&Cs programs. | |

| 3.5 Processes are in place to guide and assist employees to report and effectively manage real, apparent or potential conflicts of interest. |

Page details

- Date modified: