(Version 1.1 – April 2025)

Revisions of this Guide

Changes to this Guide have been made and were published on April 15, 2025. A summary of the changes can be found in the table at the bottom of this page.

Aussi disponible en français sous le titre : Crédit d’impôt à l’investissement pour l’hydrogène propre – Guide sur la validation et la vérification

Foreword

The Clean Hydrogen Investment Tax Credit – Validation and Verification Guidance Document (“this Guide”) outlines requirements and guidance for validation and verification activities required under the Clean Hydrogen Investment Tax Credit (ITC), as well as other taxpayer requirements for clean hydrogen projects, including those that produce ammonia. This version of this Guide is limited to validation requirements. The next version will outline the verification requirements.

Disclaimer

This Guide does not in any way supersede or modify the Income Tax Act (ITA) or the Clean Hydrogen Investment Tax Credit – Carbon Intensity Modelling Guidance Document (“CI Modelling Guidance”). Any information in this Guide that relates to the provisions of the ITA or the CI Modelling Guidance in respect of the Clean Hydrogen ITC is provided for information purposes only and does not offer any interpretation of the ITA or CI Modelling Guidance.

This Guide reflects the ITA and the CI Modelling Guidance as they stand at the time of its publishing. Therefore, taxpayers should always consult the latest versions of the ITA and the CI Modelling Guidance. Where there are any inconsistencies between this Guide and the ITA or between this Guide and the CI Modelling Guidance, the ITA and the CI Modelling Guidance take precedence.

Contents

- List of Figures

- List of Tables

- List of Attestation Forms

- Definitions

- Acronyms and Abbreviations

- 1 Introduction

- 2 Requirements for Qualified Validation Firms

- 2.1 Qualified Validation Firm Qualifications

- 2.2 Training and Experience Requirements for Validation Team and Validation Reviewer(s)

- 2.3 Insurance Coverage

- 2.4 Management of Independence and Arm’s Length Relationship

- 2.5 Complaints Mechanism

- 2.6 Maintenance of Records

- 3 Requirements Relevant to the Validation Process

- 3.1 Introduction

- 3.2 Validation Criteria

- 3.3 Pre-Validation

- 3.4 Validation Execution and Evidence-Gathering Activities

- 3.5 Validation Report

- 3.6 Validation Review and Record-Keeping

- 4 Requirements Relevant to the Verification Process (coming in a future version of this Guide)

- 5 Other Taxpayer Requirements

- Appendix A: Project Documentation Stages

- Appendix B: Validation Report

- Appendix C: Examples of Opinions in Validation Declarations

- Appendix D: Minimum Validation Records

- Appendix E: Uncertainty

- Appendix F: Data Sampling

- Appendix G: Sample Questions for Validators

- Appendix H: Complete Monitoring Plan and Measurement Requirements

- Revision History

List of Figures

- Figure 1-1: Timing of Validation and Verification in the Clean Hydrogen ITC

- Figure 2-1: Summary of Requirements for Validation Team and Validation Reviewer(s)

- Figure 3-1: Concept of Inadequate Disclosure

- Figure 3-2: Example of Uncertainty in CI

- Figure 3-3: Validation Report Composition

- Figure 3-4: Decision Tree for Validation Opinion Types

List of Tables

- Table 2-1: Examples of Threats to Independence and Potential Mitigation Measures

- Table 3-1: Summary of Validation Criteria

- Table 3-2: Documentation Required for FEED Study or Equivalent Study

- Table 3-3: Project Carbon Intensity Documents

- Table 3-4: Ammonia Justification Documents

- Table 3-5: Monitoring Plan Requirements at Different Stages of Clean Hydrogen Project

- Table 3-6: Qualitative Materiality Examples

- Table 3-7: Inadequate Disclosure Qualitative Materiality Examples

- Table 3-8: Modified Opinion - Example Disclosures

- Table 5-1: Qualitative Material Change Examples

- Table A-1: Minimum Requirements for Documentation at Different Stages of Clean Hydrogen Project

- Table H-1: Measurement Point Information

List of Attestation Forms

DefinitionsFootnote 1

actual carbon intensity (intensité carbonique réelle): means the carbon intensity of hydrogen that is produced by a qualified clean hydrogen project of a taxpayer, based on the actual inputs to the production of hydrogen and actual emissions from the production of hydrogen by the project (ITA s. 127.48[1]).

advanced modelling (modélisation avancée): one of two modelling approaches described in the Clean Hydrogen Investment Tax Credit – Carbon Intensity Modelling Guidance Document. It is applicable when the hydrogen production process and all supporting equipment and activities could be represented by more than one unit process, such as the following unit processes defined in the Clean Hydrogen Investment Tax Credit – Carbon Intensity Modelling Guidance Document: B—Oxygen and nitrogen generation system (AM), C—Carbon dioxide (CO2) capture, at HPS (AM), and D—Electricity and heat generation system, in addition to A—Hydrogen production, at HPS (AM).

allocation (affectation): partitioning the input or output flows of a process or a product system between the product system under study and one or more other product systems (ISO 14040).

arm’s length (lien de dépendance)Footnote 2: see ITA s. 251(1).

average actual carbon intensity (intensité carbonique réelle moyenne): the average of the reported actual carbon intensities for each operating year of the project’s compliance period, weighted by quantity of hydrogen produced in each year (ITA s. 127.48[1]).

captured carbon (carbone capté): means captured carbon dioxide that (a) would otherwise be released into the atmosphere or (b) is captured directly from the ambient air (ITA s. 127.44[1], s. 127.48[1]).

carbon dioxide equivalent (équivalent en dioxyde de carbone): means the carbon dioxide emissions that would be required to produce a warming effect equivalent to the emissions of any specified greenhouse gas, as determined in accordance with the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document published by the Government of Canada over an assessment period of 100 years (ITA s. 127.48[1]).

carbon intensity (intensité carbonique): means the quantity in kilograms of carbon dioxide equivalent per kilogram of hydrogen produced (ITA s. 127.48[1]).

CCUS process (processus de CUSC): means the process of carbon capture, utilization and storage that includes the (a) capture of carbon dioxide (i) that would otherwise be released into the atmosphere, or (ii) directly from the ambient air, and (b) storage or use of the captured carbon (ITA s. 127.48[1], s.127.44[1]).

CFR carbon intensity (intensité carbonique selon le RCP): means carbon intensity as defined in subsection 1 of the Clean Fuel Regulations (ITA s. 127.48[1]).

clean ammonia (ammoniac propre): means ammonia produced from clean hydrogen (ITA s. 127.48[1]).

clean hydrogen (hydrogène propre): means hydrogen produced, whether solely or in conjunction with other gases, that has a carbon intensity of less than four (ITA s. 127.48[1]).

clean hydrogen project (projet pour l’hydrogène propre): means a project involving (a) the operation of eligible clean hydrogen property; (b) the production of clean hydrogen; and (c) if applicable, the production of clean ammonia that uses a feedstock of clean hydrogen produced by the project of the taxpayer (ITA s. 127.48[1]).

clean hydrogen project plan (plan de projet pour l’hydrogène propre): see ITA s. 127.48(1) and Section 1.3.1 of this Guide.

controls (contrôles): taxpayer’s policies and procedures that help to ensure that the statement (e.g., expected CI or actual CI and actual hydrogen production, as appropriate) and report (e.g., validation information package or compliance report, as appropriate) are free from material misstatement with respect to the criteria and conform to the criteria.

compliance period (période de conformité): period during which the taxpayer’s operating activities will be subject to compliance monitoring and verification, and over which the average actual carbon intensity will be calculated. In respect of a clean hydrogen project of a taxpayer, compliance period means the period of time beginning on the first day of the compliance period of the project and ending on the last day of the fifth operating year of the project (ITA s. 127.48[1]).

cradle-to-gate (berceau à la porte): scope of a carbon intensity which covers all life cycle stages up to the production facility gate.

criteria (critères): a policy, procedure, or requirement used as a benchmark against which the statement (e.g., expected CI or actual CI and actual hydrogen production, as appropriate) and report (e.g., validation information package or compliance report, as appropriate) are compared.

data trail (piste de données): a complete record by which information can be traced to its source.

dedicated geological storage (stockage géologique dédié): in respect of a CCUS project, means a geological formation that is (a) located in a designated jurisdiction; (b) capable of permanently storing captured carbon; (c) authorized and regulated for the storage of captured carbon under the laws of the designated jurisdiction; and (d) a formation in which no captured carbon is used for enhanced oil recovery (ITA s. 127.44[1]).

designated jurisdiction (juridiction désignée): means (a) the provinces of British Columbia, Saskatchewan and Alberta; and (b) any other jurisdiction within Canada (including the exclusive economic zone of Canada) or the United States for which a designation by the Minister of the Environment under subsection (13) is in effect (ITA s. 127.44[1]).

eligible clean hydrogen property (bien admissible pour l’hydrogène propre): means property that (a) is acquired by a qualifying taxpayer and becomes available for use in respect of a qualified clean hydrogen project of the taxpayer in Canada on or after March 28, 2023; (b) has not been used, or acquired for use or lease, by any person or partnership for any purpose whatever before it was acquired by the taxpayer; and (c) is a property situated in Canada and meets all other requirements stipulated in the definition in ITA s. 127.48(1).

eligible hydrocarbon (hydrocarbure admissible): means, at any time, (a) natural gas; (b) a substance sourced all or substantially all from raw natural gas; (c) an eligible renewable hydrocarbon or (d) a substance that is (i) a by-product from processing one or more substances described in paragraphs (a) or (b), and (ii) included in the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document published by the Government of Canda at that time (ITA s. 127.48[1]).

eligible pathway (méthode admissible): means the production of hydrogen (a) from electrolysis of water; or (b) from the reforming or partial oxidation of eligible hydrocarbons, with carbon dioxide captured using a CCUS process (ITA s. 127.48[1]).

eligible power purchase agreement (entente pour l’achat d’électricité admissible): a written agreement that allows or will allow a taxpayer to purchase electricity from an eligible electricity generation source and in compliance with the definition in ITA s. 127.48(1).

eligible renewable hydrocarbon (hydrocarbure renouvelable admissible): a hydrocarbon produced from non-fossil carbon that is included in the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document, for which a CFR carbon intensity can be calculated, and that meets the requirements outlined in the ITA s. 127.48(1).

eligible use (utilisation admissible): means (a) the storage of captured carbon in dedicated geological storage; or (b) the use of captured carbon in producing concrete in Canada or the United States using a qualified concrete storage process (ITA s. 127.44[1]).

emissions (émissions): a release of greenhouse gases to the atmosphere, but in this Guide it is also used as an abbreviation for emissions, removal, and storage for brevity.

evidence (preuves): information to support the taxpayer’s statement and report (validation information package or compliance report, as appropriate).

evidence-gathering activities (activités de collecte de preuves): activities that collect evidence upon which to base a validation/verification opinion. Evidence-gathering activities can include observation, inquiry, analytical testing, confirmation, recalculation, examination, retracing, tracing, control testing, sampling, estimate testing, cross-checking, and reconciliation.

expected carbon intensity (intensité carbonique attendue): means the carbon intensity of hydrogen that is expected to be produced by a particular clean hydrogen project of a taxpayer, as documented in the taxpayer’s clean hydrogen project plan in respect of the project. The expected carbon intensity is calculated according to s. 127.48(6) based on the projected performance of the clean hydrogen project and is validated by the qualified validation firm (ITA s. 127.48[1]).

feedstock type (type de charge d’alimentation): category of feedstock included in the Fuel LCA Model and as specified in the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document.

first day of the compliance period (premier jour de la période de conformité): the day the compliance period begins, either one hundred and twenty (120) days after the clean hydrogen project first produces hydrogen or up to two years and 120 days after, if appropriate elections are filed by the taxpayer (ITA s. 127.48[1]).

Fuel LCA Model (Modèle d'ACV des combustibles): means the Government of Canada’s Fuel Life Cycle Assessment Model that is published by the Minister of the Environment (ITA s. 127.48[1]).

functional unit (unité fonctionnelle): quantified performance of a product system for use as a reference unit (ISO 14040).

greenhouse gas (gaz à effet de serre): gaseous constituent of the atmosphere, both natural and anthropogenic, that absorbs and emits radiation at specific wavelengths within the spectrum of infrared radiation emitted by the Earth’s surface, the atmosphere, and clouds.

ineligible use (utilisation non admissible): means (a) the emission of captured carbon into the atmosphere, other than (i) for the purposes of system integrity or safety, or (ii) incidental emission made in the ordinary course of operations; (b) the storage or use of captured carbon for enhanced oil recovery; and (c) any other storage or use that is not an eligible use (ITA s. 127.44[1]). Any captured carbon subject to an ineligible use is treated as an emission to the atmosphere for the purposes of calculating expected or actual CI under the Clean Hydrogen ITC (ITA s. 127.48[6]).

input (intrant): product, material, or energy flow that enters a unit process (ISO 14040).

intended users (utilisateurs cibles): are the Minister of Natural Resources (Natural Resources Canada), the Minister of National Revenue (Canada Revenue Agency), and the Minister of the Environment (Environment and Climate Change Canada), who rely on the reported information to administer the Clean Hydrogen ITC.

level of assurance (niveau d’assurance): a degree of confidenceFootnote 3 in a statement. There are two levels: limited and reasonable. The Clean Hydrogen ITC requires a reasonable level of assurance for verifications. There is no level of assurance for validation as the validator is required to address all applicable GHG related activity characteristics in the design of the validation and collect sufficient and appropriate evidence to support their conclusion.

material change (changement important): generally, any change to a clean hydrogen project design that can modify the decisions of the intended users. Material changes to projects are discussed in Section 5.2 of this Guide and include changes that the taxpayer reasonably expects will increase the CI of the project by more than 0.5 kg CO2e/kg H2 (ITA s. 127.48[7]).

materiality (importance relative): concept that individual misstatements or the aggregation of misstatements could influence the intended users’ decisions.

materially modified (modifié substantiellement): means modified in such a way as to reasonably be expected to cause a quantitatively material change to the expected CI, or in a sufficiently complex manner that NRCan considers a detailed re-evaluation necessary to estimate the quantitative or qualitative impact.

misstatement (déclaration erronée): a difference between the amount reported, classification, presentation, or disclosure of an item and the amount reported, classification, presentation, or disclosure that is required for the item to be in accordance with the criteria. Misstatements could arise from errors or fraud. Misstatements can also be classified as errors, omissions and misreportings, where misreportings include differences in classification, presentation and disclosure.

modified opinion (avis modifié): opinion that is issued by the validator/verifier when there are no material misstatements and the validation information package/compliance report has been prepared in accordance with the criteria; however, there is a departure from the requirements of the criteria, deficiencies in the assumptions used to develop future estimates (validation only), or a scope limitation.

openLCA (openLCA): free and open-source software into which the Fuel LCA Model must be imported.

operating year (année d’exploitation): means each cumulative 365-day period, the first of which begins on the first day of the compliance period of a taxpayer’s clean hydrogen project, disregarding any period during which the project is not operating (ITA s. 127.48[1]).

output (extrant): product, material or energy flow that leaves a unit process (ISO 14040).

product system (système de produits): defined as a collection of unit processes with elementary and product flows, performing one or more defined functions, and which models the life cycle of a product (ISO 14040).

qualified concrete storage process (processus de stockage dans le béton admissible): means a process evaluated against the ISO 14034:2016 standard Environmental management — Environmental technology verification for which a validation statement confirming that at least 60% of the captured carbon that is injected into concrete is expected to be mineralized and permanently stored in the concrete has been issued by a professional or organization that (a) is accredited as a verification body, under ISO 14034:2016, Environmental management – Environmental technology verification and ISO/IEC 17020:2012, Conformity assessment — Requirements for the operation of various types of bodies performing inspection, by the Standards Council of Canada, the ANSI National Accreditation Board (U.S.) or any other accreditation organization that is a member of the International Accreditation Forum; and (b) meets the requirements of a third-party inspection body described in ISO/IEC 17020:2012, Conformity assessment — Requirements for the operation of various types of bodies performing inspection (ITA s. 127.44[1]).

qualified validation firm (firme admissible de validation): an independent, arm’s length professional engineer or professional engineering firm that meets the experience, training, jurisdictional, insurance, and other requirements outlined in ITA s. 127.48(1) and in Section 2 of this Guide. Qualified validation firms are permitted to validate expected carbon intensity for clean hydrogen project plan submissions under the Clean Hydrogen ITC.

qualifying taxpayer (contribuable admissible): means a taxable Canadian corporation (ITA s. 127.48[1]).

qualified verification firm (firme admissible de vérification): an independent, arm’s length professional engineer, professional engineering firm, or verification body accredited under the Clean Fuel Regulations that meets the experience, training, jurisdictional, insurance and other requirements outlined in ITA s. 127.48(1) and in Section 4 of this Guide. Qualified verification firms are permitted to verify actual carbon intensity for final compliance report submissions under the Clean Hydrogen ITC.

reasonableness (caractère raisonnable): generally means that the clean hydrogen project design is for a facility that provides the intended service or product, does not violate fundamental physical laws, assumes efficiencies that are aligned with typical equipment in that service, has operating parameters that are within the specifications of the process and equipment, is designed to survive the anticipated life of the facility (consumables, repairs, and replacements excluded), and enables future verification.

simplified modelling (modélisation simplifiée): one of two modelling approaches described in the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document and is applicable when the entire hydrogen production process and all supporting equipment and activities, can be represented by only one unit process.

specified greenhouse gas (gaz à effet de serre déterminé): means (a) carbon dioxide; (b) methane; (c) nitrous oxide; (d) sulphur hexafluoride; and (e) any other greenhouse gases listed in the Fuel LCA Model and included in the Clean Hydrogen Investment Tax Credit—Carbon Intensity Modelling Guidance Document at the time that a taxpayer files its most recent clean hydrogen project plan with the Minister of Natural Resources (ITA s. 127.48[1]).

specified percentage (pourcentage déterminé): tax credit rate (percentage) applicable to the capital cost of eligible clean hydrogen property. The specified percentage varies depending on the specific carbon intensity of hydrogen to be produced and when the property was acquired and became available for use. A different tax credit rate applies to clean ammonia equipment and certain equipment used solely in connection with clean ammonia equipment acquired for use in a clean hydrogen project (ITA s. 127.48[1]).

statement (déclaration): factual and objective taxpayer declaration that provides the subject matter for the validation or verification (e.g., expected CI, or actual CI and actual hydrogen production, as appropriate).

system process (processus agrégé): aggregation of unit processes that models the life cycle emission factors of a certain activity.

taxpayer (contribuable): the proponent of the clean hydrogen project. In this Guide, the term “applicant” may be used interchangeably with “taxpayer”.

uncertainty (incertitude): a parameter associated with quantification, which characterizes the dispersion of the values that could be reasonably attributed to the quantified amount.

unit process (processus élémentaire): smallest element considered in the life cycle inventory analysis for which input and output data are quantified (ISO 14040/44).

unmodified opinion (avis non modifié): opinion that is issued by the validator/verifier when there are no material misstatements and the validation information package/compliance report has been prepared in accordance with the criteria.

validator (validateur): competent and independent person, with responsibility for performing and reporting on the validation process (i.e., member of the validation team as defined in Section 2.2.1 of this Guide).

validation (validation): process for evaluating the reasonableness of the assumptions, limitations and methods that support a statement about the outcome of future activities.

validation information package (dossier d'information pour la validation): documentation required for validation as described in Section 3.3.2 of this Guide.

validation/verification opinion (avis de validation ou de vérification): written attestation by the validator/verifier to the intended user that provides confidence on the statement and report.

validation/verification reviewer (examinateur de la validation ou de la vérification): competent person, not a member of the validation/verification team, who reviews the validation/verification team and validation/verification activities.

verification (vérification): process for evaluating a statement of historical data and information to determine if the statement is materially correct and conforms to criteria.

verifier (vérificateur): competent and independent person, with responsibility for performing and reporting on the verification process (i.e., member of the verification team).

Acronyms and Abbreviations

| Acronym or abbreviation | Meaning |

|---|---|

| AM | Advanced Modelling |

| ANSI | American National Standards Institute |

| CCUS | Carbon Capture, Utilization, and Storage |

| CFR | Clean Fuel Regulations |

| CH-ITC | Clean Hydrogen Investment Tax Credit |

| CI | Carbon Intensity |

| CO2e | Carbon Dioxide Equivalent |

| CRA | Canada Revenue Agency |

| ECCC | Environment and Climate Change Canada |

| FEED | Front-End Engineering Design |

| GHG | Greenhouse Gas |

| GWP | Global Warming Potential |

| HPS | Hydrogen Product System |

| IFC | Issued for Construction |

| ISO | International Organization for Standardization |

| ITA | Income Tax Act |

| KPI | Key Performance Indicator |

| LCA | Life Cycle Assessment |

| LDL | Lower Detection Limit |

| MOU | Memorandum of Understanding |

| NRCan | Natural Resources Canada |

| OPS | Other Product System |

| P&ID | Piping and Instrumentation Diagram |

| PPA | Power Purchase Agreement |

| PSA | Pressure Swing Adsorption |

| SM | Simplified Modelling |

| TS | Technical Specification |

| UFD | Utility Flow Diagram |

| UP | Unit Process |

1 Introduction

1.1 Purpose of this Guidance Document

This Guide has been written for taxpayers, qualified validation firms, qualified verification firms, validation/verification teams and validation/verification reviewers working with Natural Resources Canada (NRCan) and the Canada Revenue Agency (CRA) to support the administration of the Clean Hydrogen ITC under the ITA. The document lays out requirements and guidance for validation and verification (future version of this Guide) activities required under the Clean Hydrogen ITC. Additionally, this Guide provides guidance on the structure of validation reports (Section 3.5), compliance reports (future version of this Guide), verification reports (future version of this Guide), as well as other taxpayer requirements for clean hydrogen projects, including those producing ammonia (Section 5.2).

1.2 Background

The Clean Hydrogen ITC is described in s. 127.48 of the ITA and supports projects that produce clean hydrogen through a refundable investment tax credit. The tax credit rates are based on the expected carbon intensity (CI) of the hydrogen that will be produced (i.e., kilogram [kg] of carbon dioxide equivalent [CO2e] per kg of hydrogen), among other factors (e.g., when the property was acquired and became available for use). The credit applies to the capital cost of eligible clean hydrogen property that is acquired and that becomes available for use in respect of a qualified clean hydrogen project of the taxpayer in Canada on or after March 28, 2023, and before 2035, subject to a reduced credit rate in 2034.

To qualify for the Clean Hydrogen ITC, the taxpayer must assess the expected CI of the hydrogen that will be produced based on the design of the project using the Fuel LCA Model that is maintained by Environment and Climate Change Canada (ECCC). The expected CI must be validated by a qualified validation firm that is always independent of, deals at arm’s length with and is not an employee of the taxpayer.

Once operating, qualified clean hydrogen projects must demonstrate that the actual carbon intensity (CI) of the hydrogen they produce falls into the same tax credit tier as the expected CI over the compliance period for the project. At the end of the compliance period, the actual CI of the hydrogen produced during each operating year of the compliance period must be verified by a qualified verification firm.

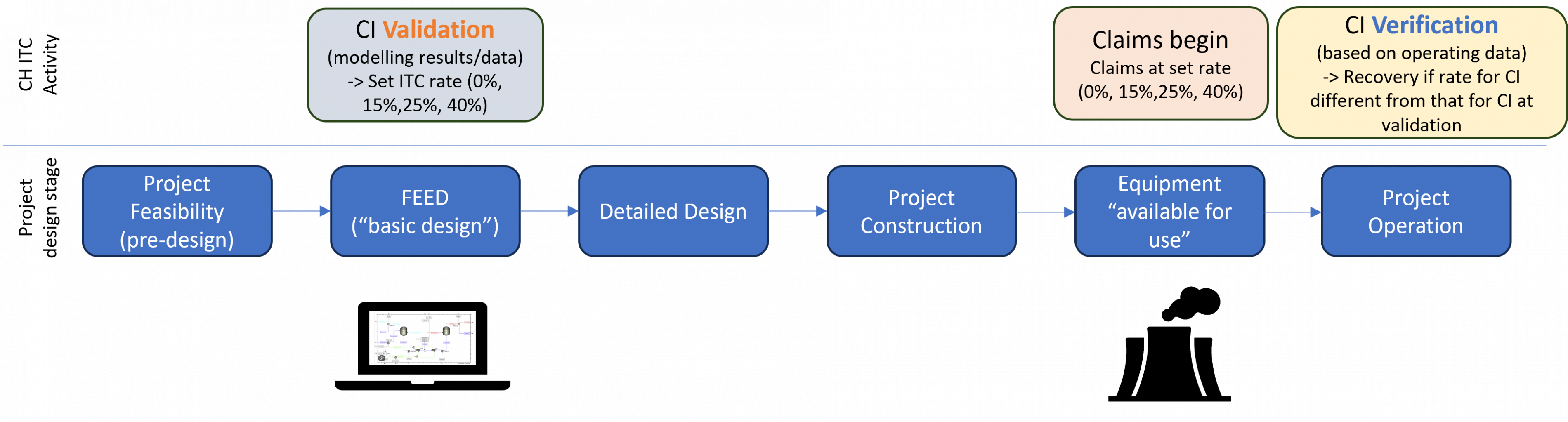

Recovery is triggered if the average actual carbon intensity (CI) is more than 0.5 kg CO2e/kg H2 higher than the expected CI and if the average actual CI would qualify for less or no support. Figure 1-1 illustrates the timing of Clean Hydrogen ITC validation and verification activities in reference to typical design and implementation stages of a project.

Figure 1-1: Timing of Validation and Verification in the Clean Hydrogen ITC

Text version

Typical project design stages are shown from project feasibility (pre-design) to project operation with the corresponding Clean Hydrogen ITC validation and verification activities. The determination of expected CI, which represents a major validation activity, occurs at the earliest, at the front-end engineering design (FEED) stage. The claim period corresponds, at the earliest, to the stage when equipment becomes available for use, which occurs after project construction but before project operation. The determination of average actual CI, which represents a major verification activity, occurs during project operation.

1.3 Validation in the Clean Hydrogen ITC

Under s. 127.48(1) of the ITA, taxpayers are required to submit a report prepared by a qualified validation firm (Section 2) in respect of the project (i.e., validation report, see Section 3.5) as part of the clean hydrogen project plan (Section 1.3.1) filed with the Minister of Natural Resources (i.e., “submitted to Natural Resources Canada [NRCan]”). To become a qualified clean hydrogen project, the Minister of Natural Resources must confirm the taxpayer’s clean hydrogen project plan in writing.

Validation differs from verification in that it provides assurance on the assumptions used to estimate CI values during future operations of a facility (expected CI). Verification provides assurance on actual CI values and thus examines historical information from an operating qualified clean hydrogen project. Consequently, the assurance differs between expected (i.e., validated expected CI values) and historical (i.e., verified actual CI values) in that validation provides negative assuranceFootnote 4 on the assumptions and verification provides positive assuranceFootnote 5 on the CI values.

The validation process is iterative. The taxpayer will present a draft expected CI value and supporting documentation to the validator in the validation information package (Section 3.3.2). If material misstatements or other issues requiring disclosure are encountered during the process of validation, the taxpayer and the validator will work together to calculate an expected CI and develop supporting documentation that appropriately represents the project design and its expected CI. The expected CI calculations, supporting documentation, and an accompanying validation report are then submitted to NRCan as part of the clean hydrogen project plan. Validation is generally not a pass/fail evaluation, but an assessment of the assumptions, limitations and variability that the clean hydrogen project may encounter and a best estimate of the expected CI value. Validation acts as a control on the proper application of guidance, reasonableness of assumptions, and assessment of uncertainty.

Key elements of validation include the validation opinion (Section 3.5.2) and disclosures (Section 3.5.3) in the validation report. NRCan will not confirm the clean hydrogen project plan until the validator reaches a conclusion (i.e., issues an unmodified opinion or modified opinion as described in Section 3.5.2) and no material misstatements remain.

1.3.1 Clean Hydrogen Project Plan

As described in s. 127.48(1) of the ITA, a “clean hydrogen project plan” is a plan for a clean hydrogen project of a taxpayer that includes the following:

- A front-end engineering design study (or an equivalent study as determined by the Minister of Natural Resources) for the project

- The expected sources of electricity to be consumed in connection with the project, including sources described in any eligible power purchase agreements

- The expected carbon intensity of the hydrogen to be produced by the project, determined in accordance with s. 127.48(6) of the ITA and supported by a report prepared by a qualified validation firm

- Any additional information required by guidelines published by the Minister of Natural Resources, including this Guide

The report prepared by the qualified validation firm must contain attestations by the firm that the assumptions in the modelling of the expected carbon intensity are reasonable and that the expected carbon intensity was determined in accordance with the Clean Hydrogen Investment Tax Credit – Carbon Intensity Modelling Guidance Document. See Section 3.5 of this Guide for further guidance on validation report requirements.

If the project is intended to produce clean ammonia, the plan must also demonstrate

- that the project can reasonably be expected to have sufficient hydrogen production capacity to satisfy the needs of the taxpayer’s ammonia production facility (Section 5.2.1); and

- if the taxpayer’s hydrogen production facility and its ammonia production facility are not co-located, the feasibility of transporting hydrogen between the facilities (Section 5.2.1).

The taxpayer must file the clean hydrogen project plan with the Minister of Natural Resources for confirmation, in the form and manner determined by the Minister of Natural Resources. Ultimately, confirmation by the Minister of Natural Resources is a requirement for the project to become a “qualified clean hydrogen project”.

1.4 Verification in the Clean Hydrogen ITC

Under s. 127.48(16) of the ITA, taxpayers must file annual compliance reports detailing the quantity and actual CI of hydrogen produced during that year, any shutdown time of the project during the year, as well as additional information as described in Section 4. At the end of the compliance period, a qualified verification firm must verify the actual CI of the hydrogen produced during each operating year of the compliance period and prepare a verification report that must be included in the taxpayer’s final compliance report.

The verification process is also iterative. The taxpayer will present draft actual CI values for each operating year and supporting data and documentation to the verifier. If material misstatements or other issues requiring disclosure are encountered during the verification process, the verifier and taxpayer will work together to provide a verification report that appropriately represents the project’s operations and actual CI values. Verification, which is based on historical evidence, is more of a pass/fail evaluation than validation as the actual operations can be determined. Verification, from NRCan’s perspective, is a control on the most appropriate average actual CI value to include in the taxpayer’s final compliance report. NRCan will only consider final compliance reports in which the verifier is able to reach a conclusion and no material misstatements remain. Compliance reporting and verification will be based on the data collection and calculation methods established in the monitoring plan. More information on qualified verification firm requirements and verification activities will be provided in a future version of this Guide.

1.5 Criteria

Criteria are the policies, procedures, or requirements used as a reference against which the statement (e.g., expected CI or actual CI and actual hydrogen production, as appropriate) and reports (validation information package or compliance report, as appropriate) are compared, and serve as the benchmark for comparison in validation and verification. The objective of validation under the Clean Hydrogen ITC is to assess the degree to which the taxpayer’s expected CI calculation and other information in the validation information package conform to the criteria. In verification, the objective is to assess the degree to which the taxpayer’s compliance reports and actual CI calculations conform to the criteria.

- Criteria common to both validation and verification are described in Section 1.5.1 below

- Criteria that are specific to validation are presented in Section 3.2

- Criteria that are specific to verification will be presented in a future version of this Guide

1.5.1 Criteria Common to Verification and Validation

For determining whether the expected and actual CI values have been quantified appropriately under the Clean Hydrogen ITC, and that the validation information package and compliance reports have been appropriately prepared, the following common criteria are used:

- Section 127.48 of the ITA

- The Fuel LCA Model and associated documents (Section 1.5.2)

- This Guide, which outlines requirements for taxpayers, qualified validation firms, and qualified verification firms in preparing CI documentation required for the Clean Hydrogen ITC

- The Clean Hydrogen ITC website

- Any instructions contained in relevant templates (i.e., CH-ITC Workbook, Project KPI Workbook)

1.5.2 Fuel LCA Model and Associated Documents

The Fuel LCA Model is a tool used to calculate the life cycle CI of fuels and energy sources used and produced in Canada. The Model helps to support the delivery of regulations and programs as part of Canada's actions on climate change. For example, the Clean Fuel Regulations use the Model to determine the CI of fuels, material inputs and energy sources for credit creation.

The following documents and tools should be consulted and used in parallel for calculating a CI value using the Fuel LCA Model in the context of the Clean Hydrogen ITC:

- The Clean Hydrogen Investment Tax Credit – Carbon Intensity Modelling Guidance Document (“CI Modelling Guidance”) is intended for use by taxpayers and provides comprehensive CI modelling instructions for assessing the CI of a clean hydrogen project with the Model. It also provides the main instructions to enter data in the CH-ITC Workbook and in the Fuel LCA Model.

- The CH-ITC Workbook contains spreadsheets that help to convert applicant data into data for input into the Fuel LCA Model and document the modelling of the hydrogen product system. It must be used to carry out all calculations prior to data entry in the Fuel LCA Model. This could include unit conversions, weighted average calculations, etc.

- The Clean Fuel Regulations (CFR) Specifications for Fuel LCA Model CI Calculations is the central document to consult to determine a CI value using the Fuel LCA Model under the CFR. The CI Modelling Guidance is based on the CFR Specifications to ensure consistency between the CI modelling within Government of Canada regulations and programs, although there are some key differences. The CFR specifications may also be required for the CI modelling of some feedstocks and fuel inputs covered by the CI Modelling Guidance.

- The Data Library and Fuel Pathways are the main components of the Fuel LCA Model that must be uploaded in the openLCA modelling software. The Data Library provides a selection of life cycle emission factors (called system processes) that can be used to populate the hydrogen pathway (cradle-to-gate – mass basis) stored in the “Fuel Pathways” folder of the Fuel LCA Model.

2 Requirements for Qualified Validation Firms

2.1 Qualified Validation Firm Qualifications

Subsection 127.48(1) of the ITA defines a “qualified validation firm” as follows:

[…] in respect of a clean hydrogen project of a taxpayer, an engineer or engineering firm that

- is registered and in good standing with a professional association that has the authority or recognition by law of a jurisdiction in Canada to regulate the profession of engineering in

- the jurisdiction where the project is located, or

- if there is no professional association in the jurisdiction described in subparagraph (i), a jurisdiction in Canada where a professional association regulates the profession of engineering;

- has appropriate insurance coverage;

- has expertise in modelling using the Fuel LCA Model and engineering expertise in production processes for hydrogen and, if applicable, ammonia;

- at all times, is independent of, deals at arm’s length with and is not an employee of the taxpayer; and

- meets the requirements described in guidelines published by the Minister of Natural Resources, including the Clean Hydrogen Investment Tax Credit – Validation and Verification Guidance Document.

The requirements for qualified validation firms are further described in Sections 2.2, 2.3, 2.4, 2.5, and 2.6 below.

Note: the qualified validation firm must be registered and in good standing with a professional association in the jurisdiction where the project is located. For the purposes of this work, the project location is considered to be the physical location where the hydrogen facility has been or will be built.

2.2 Training and Experience Requirements for Validation Team and Validation Reviewer(s)

Validation is executed by the validation team (Section 2.2.1), who performs the validation, and the validation reviewer(s) (Section 2.2.2.1), who are not a part of the validation team but review the validation team’s work and conclusions. The validation team is responsible for executing the validation, and the validation reviewer(s) are a mandatory quality control point for the validation and review the validation prior to submission to the taxpayer. This structure follows the general guidelines of ISO 14064-3.

NRCan requires that the validation team leader be an employee of the qualified validation firm (or the licensed individual who is the qualified validation firm in jurisdictions where firms are not licensed). It is also preferred that validation reviewer(s) be employee(s) of the qualified validation firm. When this is not possible, the validation reviewer(s) may be subcontractor(s), provided they are familiar with the qualified validation firm’s risk tolerance and associated risk management procedures.

Other validation team positions can be filled by employees or subcontractors. NRCan encourages the use of subcontractors for roles that require expertise that may not be housed within the qualified validation firm. Figure 2-1 shows a summary of the individuals that take part in the validation process and their connection with the qualified validation firm.

Figure 2-1: Summary of Requirements for Validation Team and Validation Reviewer(s)

Text version

An overview of the individuals that take part in the validation process is presented. The qualified validation firm has specific requirements under the legislation, including being an engineering firm and other requirements set out in this Guide. The validation team may be composed of one individual (which would be the validation team leader) or multiple individuals. The team leader must be employed by the qualified validation firm or, in jurisdictions where firms are not licensed, must be the firm itself. The team leader must therefore be registered as a professional engineer, among other requirements. Other team members may be also employed by the qualified validation firm or be its subcontractors. Regardless of how many individuals make up the validation team, it must, as a composite, have all the necessary competencies and specialties to conduct the validation. The validation process is completed by the validation reviewers, who are not part of the validation team. The validation reviewers must, at a minimum, have the same competencies as specified for the team leader. It is preferred that the reviewers be employed by the qualified validation firm to ensure the complete understanding of the firm’s policies and procedures, particularly the risk management aspects. Should the reviewers not be employed by the qualified validation firm, they need to be familiar with its risk tolerance and associated risk management procedures.

2.2.1 Validation Team

The validation team may be comprised of one or more individuals, provided the team, as a composite, has all the necessary training and experience to conduct the validation. It is mandatory that a single individual be designated validation team leader, but the other roles may not require additional individuals if members of the team have the experience to fulfill multiple roles (e.g., a one-individual validation team would be comprised of a team leader who meets the experience and training requirements for all validation team roles).

Additional expertise may be required in the areas of life cycle assessment, process design, IT systems, etc. to ensure that the subject matter of the validation information package is adequately addressed. Of note, each validation reviewer must be a separate individual who is not part of the validation team.

2.2.1.1 Validation Team Leader

As this work falls within the scope of the practice of professional engineering, the team leader must be an engineer that is registered and in good standing with a professional association, understand the requirements of the Clean Hydrogen ITC, and have sufficient validation knowledge as described in ISO 14064-3, ISO 14065, and ISO 14066, which includes

- understanding of the validation process including the design, typical evidence-gathering activities, significant decision points, materiality interpretations

- understanding of the qualified validation firm procedures

- technical competence in the applicable sector(s)

- understanding of the validation documentation, including the documentation of misstatements and data gaps in conclusion and their resolution; and

- sufficient knowledge to manage the validation team, including each member’s competencies, in order to complete a validation assignment

The team leader must

- successfully complete ISO 14064-3:2019 formal trainingFootnote 6

- have Fuel LCA Model training and/or relevant experience

- attend the CH-ITC Validation Information Session (Section 2.2.3)

The team leader has the authority to approve validation plans and evidence-gathering plans and is responsible for the validation work. There is no additional certification process for becoming a validation team leader.

2.2.1.2 LCA Specialist

For each validation assignment, the validation team must include an individual who meets the below requirements of a qualified LCA specialist.

The specialist must understand and be able to apply the requirements of life cycle assessment according to the most recent versions of

- Standard ISO 14040 Environmental management — Life cycle assessment — Principles and framework

- Standard ISO 14044 Environmental management — Life cycle assessment — Requirements and guidelines

- Technical Specification – ISO/ TS 14071 Environmental management — Life cycle assessment — Critical review processes and reviewer competencies: Additional requirements and guidelines to ISO 14044:2006

The LCA specialist must have knowledge of all of the following:

- The use of the Fuel LCA Model, CI Modelling Guidance and current LCA practice

- The use of the Clean Fuel Regulations (CFR) Specifications for Fuel LCA Model CI Calculations (if a CFR carbon intensity [CI] is used)

- LCA dataset generation and LCA dataset review

- Critical reviews of LCA

- All scientific and engineering disciplines relevant to the LCA being reviewed

- Environmental, technical, and other relevant performance aspects of any product system assessed

The LCA specialist must have all of the following experience:

- Has actively participated in at least two LCAs as an LCA practitioner that addressed life cycle inventory, GHG emissions inventory or the global warming impact category and were compliant with ISO 14040/14044 standards

- Carried out or participated in at least one LCA review as an internal expert or two LCA reviews as an external expert within the last ten yearsFootnote 7

- Fuel LCA Model training and/or relevant experience

The LCA specialist must conduct their review in accordance with subsection 6.2 of ISO 14044.

2.2.1.3 Process Modelling Specialist

The validation team must include a process modelling specialist with the expertise to critically review the process model used to provide inputs for the LCA. The process modelling specialist must have all of the following experience:

- Applying established calculation and design methods to model industrial processes

- Producing mass and energy balances using simulation software (e.g., Aspen HYSYS, Aspen Plus, CHEMCAD, gPROMS, ProSimPlus and DWSIM)

- Determining and preparing process equipment specifications

- Interpreting process flow diagrams (PFD) and piping and instrumentation diagrams (P&ID)

2.2.1.4 CFR Specialist

For each validation assignment where the project proposes to use eligible renewable hydrocarbons for the purpose of producing hydrogen (i.e., uses CFR CI), the validation team must include an individual who has sufficient knowledge of all of the following in the context of the determination of a CFR CI:

- The use of the Fuel LCA Model, and current LCA practice

- The use of the CFR Specifications for Fuel LCA Model CI calculations

- The use of a CFR CI in the Clean Hydrogen ITC

- CFR verification practices

There are no threats to independence for a member of a validation team or a validation firm validating a clean hydrogen project plan who also supports the client with CFR reporting.

2.2.2 External to Validation Team

2.2.2.1 Validation Reviewer(s)

Each validation is reviewed by at least one qualified validation reviewerFootnote 8. If required, there may be more than one validation reviewer to address the competencies for the review. The validation reviewer(s) are selected such that they are competent and not part of the validation team. The validation reviewer(s) may provide feedback to the validation team but cannot participate in planning or execution of validation activities.

The validation reviewer(s) may be an employee or subcontractor of the qualified validation firm, or a validator from another independent qualified validation firm. The validation reviewer(s) must have, as a minimum, the same competencies as specified for the validation team leader. See Section 3.6.1 for a detailed description of the scope of evaluation for validation reviewer(s). Validation reviewer(s) must have the following skills and experience:

- Experience and a theoretical understanding of the validation process, as applicable, including the design, typical evidence-gathering activities, significant decision points, and materiality interpretations

- An understanding of the requirements of the Clean Hydrogen ITC

- An understanding of the requirements of an independent reviewer as described in ISO 14064-3

- An understanding of the qualified validation firm procedures

- Technical competence in the applicable sector(s) (e.g., Fuel LCA Model experience, hydrogen production engineering experience, and ammonia production engineering experience, if applicable)

The validation review may be conducted concurrently with the validation process to allow significant issues identified by the validation reviewer(s) to be resolved before the opinion is issued, provided that the independence of the validation reviewer(s) is maintained, and the activities planned and undertaken by the validation reviewer(s), including the results, are documented.

2.2.3 Clean Hydrogen ITC Specific Validation Information Sessions

To qualify as a validation team leader or validation reviewer under the Clean Hydrogen ITC, individuals must complete the following:

- CH-ITC Validation Information SessionFootnote 9 which addresses Clean Hydrogen ITC requirements and the validation process. Upon completing the information session, the individuals may decide to test their understanding using the optional self-assessment. NRCan will not record the scores on the self-assessment quiz. For greater certainty, these information sessions are only intended to provide basic information and should not be, in any way, considered as constituting sufficient knowledge to become a validator.

- An Attestation of Participation (PDF, 149 KB) in the CH-ITC Validation Information Session must be completed and included in the validation report.

- Annual Update for Clean Hydrogen ITC Validators (one-hour online session) containing NRCan’s prior year’s validation observations and any Clean Hydrogen ITC updates.

- Validators will have the option of meeting with NRCan to address general Clean Hydrogen ITC and project-specific questions. To qualify for this service, the validator must

- satisfy the requirements of Section 2.2,

- be working with a client who is preparing a clean hydrogen project plan for submission, and

- consent to NRCan publishing their question(s) and NRCan’s response(s) on the Clean Hydrogen ITC website, while keeping the proprietary information of taxpayer confidential.

More information on these services and information sessions will be available in the future version of this Guide and on the Clean Hydrogen ITC website.

2.2.4 Familiarity with Evidence-Gathering Activities

The validation team and validation reviewer(s) should be familiar with evidence-gathering activities and techniques (e.g., those specified in ISO 14064-3) and the level of evidence they provide. The following table lists common evidence-gathering activities in their general order of strength.

| Evidence-Gathering Activity | Higher |

|---|---|

| Observation (of activities) |

|

| Examination (of documents and records) | |

| Analytical Testing | |

| Confirmation | |

| Recalculation | |

| Inquiry | Lower |

These evidence-gathering activities can be used in techniques such as the following:

- Retracing (vouching): following data trails back to source records or measurements to determine accuracy

- Tracing: following data trails to final reported values to determine completeness

- Estimate testing: assessment of the appropriateness of the estimate methodology, the applicability of the assumptions in the estimate, and the quality of the data used in the estimate

- Control testing: testing the mechanisms that ensure that the estimate of CI value is correct

- Sampling (sites and data)

- Site visits (if possible): to examine the infrastructure and collect further evidence

- Cross checking

- Reconciliation

2.3 Insurance Coverage

Qualified validation firms must have appropriate insurance coverage as per s. 127.48(1) of the ITA. That is, the qualified validation firms (i.e., the work of all members of the validation team and the validation reviewer[s]) must be insured against professional liability under a policy of a professional liability insurance. The policy must comply with the professional liability insurance requirements set forward by the geographic region:

- Policy values must be the higher of

- professional liability insurance requirements set forward by the province or territory in which the qualified validation firm is licensed, or

- professional liability insurance as appropriate for the range of activities undertaken in the geographic regions in which the qualified validation firm operates

- All requirements must be satisfied with respect to claim and aggregate coverage amounts, deductibles, coverage duration, cancellation provisions and insurance types, as applicable.

For example, projects in certain provinces may require the professional liability insurance policy as follows:

- Policy limit for each single claim of not less than $1,000,000 and an aggregate policy limit for all claims of not less than $2,000,000 per year or an automatic policy limit reinstatement feature.

- A maximum deductible amount under the policy of the greater of $5,000 or 5% of the annual fees the holder billed in the 12 months immediately before the issuance of the policy.

- Coverage for liability for errors, omissions and negligent acts arising out of the performance of all services within the practice of professional engineering offered or provided to the public by the insured subject to such exclusions and conditions and otherwise on such terms as are consistent with normal insurance industry practice from time to time.

- A provision that neither party may cancel nor amend the policy of insurance in a way that results in non-compliance with this Guide without first giving the other party at least 45 days written notice or, in the event of non-payment of premiums, 15 days written notice.

- The insurance must be placed with an insurer with an aggregate capital and surplus of at least $20,000,000 or an underwriter or syndicate of underwriters operating on the plan known as Lloyds.

An Attestation of Insurance Coverage (PDF, 112 KB) must be signed and provided with the validation report.

2.4 Management of Independence and Arm’s Length Relationship

The qualified validation firm, members of the validation team and validation reviewer(s) must not be employees of the taxpayer, and must also maintain an arm’s length relationship (Section 2.4.1) with and be independent (Section 2.4.2) from, the taxpayer. The firm/individuals may not be considered independent if there are threats to their independence, which are discussed further below. As part of the validation report, validators will need to sign an Attestation of Independence (PDF, 274 KB) confirming the arm’s length relationship and independence of the qualified validation firm, validation team members, and validation reviewer(s), and that they are not employees of the taxpayer.

2.4.1 Arm’s Length Relationship

The qualified validation firm, members of the validation team, and the validation reviewer(s) must deal at arm’s length with the taxpayer. An arm’s length relationship is described in the Income Tax Act s. 251. See the following Income Tax Folio for reference: Income Tax Folio S1-F5-C1, Related Persons and Dealing at Arm's Length - Canada.ca.

2.4.2 Threats to Independence

Threats to independence may

- exist at the present time;

- be reasonably foreseen to exist in the future; or

- be perceived as such by a reasonably well-informed observer, who could assume that a threat to independence exists, whether or not it is the case.

Threats to independence may include the following:

- Self-interest (Section 2.4.2.1)

- Self-review (Section 2.4.2.2)

- Advocacy (Section 2.4.2.3)

- Familiarity (Section 2.4.2.4)

- Intimidation or economic implications (Section 2.4.2.5)

2.4.2.1 Self-Interest

A self-interest threat occurs when the qualified validation firm, a member of the validation team, and/or a validation reviewer could directly benefit, financially or otherwise, based on the conclusion of the validation. Examples of self-interest include, but are not limited to, the following:

- Directly owning shares of the taxpayer being validated/verified

- Having a close business relationship with the taxpayer

- Contingent fees relating to the results of the validation

- Seeking potential employment with the taxpayer

- Acting as a broker-dealer (registered or unregistered), promoter, or underwriter on behalf of the taxpayer

- Taking an equity position in the clean hydrogen project that has or will submit a project plan to NRCan or a qualified clean hydrogen project

- Taking equity or payment in the form of future revenues from a project

2.4.2.2 Self-Review

A self-review threat occurs when the qualified validation firm, a member of the validation team, and/or a validation reviewer could be able to review their own work. Examples of self-review include, but are not limited to, the following:

- Developing the process model used in the design of the project being validated/verified

- Providing consulting services that directly impinge on the report or application being validated/verified, such as designing or implementing the data management systems

- Validator of the validation information package becoming a verifier of the project’s compliance report

- LCA specialist for validation of the validation information package becoming a verifier for the project’s compliance report

- Compiling or reporting the information for the validation information package or compliance report being validated/verified

2.4.2.3 Advocacy

An advocacy threat occurs when qualified validation firm, a member of the validation team, and/or a validation reviewer may be perceived to promote a taxpayer’s position or opinion to the point that objectivity may be, or may be perceived to be, compromised. Examples of advocacy include, but are not limited to, the following:

- Participating in the development of relevant fuel pathways for the Fuel LCA Model

- Advocating on behalf of the taxpayer to advance a position or point of view on an issue that directly affects the clean hydrogen project plan or compliance report

- Acting as an advocate on behalf of the taxpayer in litigation or in resolving disputes with other third parties

2.4.2.4 Familiarity

A familiarity threat occurs when the qualified validation firm, a member of the validation team, and/or a validation reviewer, by virtue of a close relationship with the taxpayer, its directors, officers, or employees, becomes overly sympathetic to the taxpayer’s interests. Examples of a familiarity threat include, but are not limited to, the following:

- A person on the validation team has a close personal relationship with a person who is employed in a critical compilation role with the taxpayer

- Acceptance of significant giftsFootnote 10 or hospitality from the taxpayer

2.4.2.5 Intimidation/Economic Implications

An intimidation or economic implications threat occurs when the qualified validation firm, a member of the validation team and/or a validation reviewer is deterred from acting objectively and exercising professional skepticism because of threats, actual or perceived, from the directors, officers or employees of the taxpayer, and their independence is potentially threatened. Examples of intimidation/economic implications include, but are not limited to, the following:

- The threat of being replaced as qualified validation firm due to a disagreement with the validation process

- Fees from the taxpayer represent a large percentage of the overall revenues of the validator

- The application of pressure to inappropriately reduce the extent of work performed to reduce or limit fees

- Threats arising from litigation with a taxpayer

2.4.3 Requirements for Managing Circumstances of Threats to Independence

In preparation for a validation engagement, the qualified validation firm evaluates whether all members of the validation team, including subcontractors, and the validation reviewer(s) meet the applicable requirements for providing an opinion independent of any interference from the taxpayer or partnership.

The taxpayer is responsible to disclose to the Minister of Natural Resources any threats to the independence of the qualified validation firm, members of the validation team and/or the validation reviewer(s) that exist.

If there is a threat to their independence, the qualified validation firm, member of the validation team or the validation reviewer whose independence is threatened cannot perform any validation activities. If the threat to independence in question can be managed, written evidence describing the actions that will be taken to mitigate the threat must be provided to the Minister of Natural Resources by the taxpayer. The Minister of Natural Resources will provide a response within 30 days of the receipt of either the disclosure of the threat to independence or the evidence describing the mitigation actions. Upon written notification by the Minister of Natural Resources that he is satisfied that the threat to independence can be effectively managed, the firm/individuals whose independence will be managed may proceed.

Table 2-1 includes a non-exhaustive list of examples of threats to independence and corresponding potential mitigation measures.

Table 2-1: Examples of Threats to Independence and Potential Mitigation Measures

| Threat | Situation | Mitigation Measures |

|---|---|---|

| Self-Interest | A validation team member’s spouse sits on the Board of Directors of the taxpayer. | The member of the board abstains from voting on any decisions involving the validation. |

| Self-Review | A person consults on the taxpayer’s project and later takes a position with a qualified validation firm and is part of the validation team that is hired to validate the same project that they originally consulted. | The qualified validation firm would ensure that this person is not part of the validation team for the taxpayer’s project until five years has passed. |

| Familiarity | The taxpayer invites the validation team to a sports game (e.g., soccer, hockey) in the corporate box. | The validation team provides compensation for the tickets. |

2.5 Complaints Mechanism

The qualified validation firm must have a documented complaints mechanism to address cases of complaints, disputes, challenges, appeals and/or conflicts filed about any element of its validations.

All qualified validation firms must be an engineer or engineering firm that is registered and in good standing with a professional association that has the authority or recognition by law of a jurisdiction in Canada to regulate the profession of engineering. Qualified validation firms may rely on the complaints mechanism of one or more professional engineering associations that have the authority or recognition by law of a jurisdiction in Canada to regulate the profession of engineering in that jurisdiction, provided that it ensures all of the following:

- Individuals who conducted any of the validation activities are not involved in the complaints-handling process

- The confidentiality of the individual or qualified validation firm filing a complaint and the subject of the complaint, when applicable

- Transparent and timely communication with all the parties involved throughout the complaints management process

- The work of all validation team members and the validation reviewer(s) is subject to the mechanism (i.e., that the LCA specialist and validation reviewer(s) are engineers or employees of an engineering firm registered and in good standing with one of the professional engineering associations)

- A formal notice of the outcome is issued to the complainant and NRCan

2.6 Maintenance of Records

Qualified validation firms must document and store the working papers and evidence related to validation activities that they performed for a minimum of fifteen years. A minimum list of records appears in Appendix D.

3 Requirements Relevant to the Validation Process

3.1 Introduction

Validation is a process that evaluates the reasonableness of the assumptions, limitations, and methods used to estimate the expected CI and respond to other requirements of the clean hydrogen project plan based on the information in the validation information package. Pre-validation requirements are discussed in Section 3.3, including the contents of the validation information package (Section 3.3.2). Execution of the validation is discussed in Section 3.4.

The output of the validation process is a validation report (Section 3.5), that is used to provide NRCan assurance on the following:

- Recognition of clean hydrogen project: the project is recognized as eligible under the Clean Hydrogen ITC.

- Recognition of clean ammonia, if applicable: the project satisfies other eligibility requirements under the Clean Hydrogen ITC, if the taxpayer’s project is intended to produce clean ammonia (Section 5.2).

- Reasonableness of project design: the assumptions, limitations, and methods for designing the process and for modelling and calculating the expected CI are reasonable.

- CI calculation: the expected CI is quantified in a materially correct manner and is presented in conformance with the validation criteria (Sections 1.5 and 3.2).

- Monitoring plan: the monitoring plan will enable future verification of the actual CI of the hydrogen produced in each year of the compliance period (Section 3.3.2.4).

NRCan expects that validation reports will be more extensive than verification reports because of the following:

- The design nature of the hydrogen facility

- The degree of disclosure needed to correctly detail the variability and uncertainty that can be expected in the CI value

- Specific equipment selection and minor design changes that remain in the facilities’ design

Depending on the stage of project evolution, applicants at an earlier stage in their design may need to contend with more uncertainty and larger validation reports; however, the advantage is an early indication of Clean Hydrogen ITC support level (specified percentage).

NOTE: Assessing the eligibility of specific process equipment, and the calculation of dual-use factors, etc. for capital support under the Clean Hydrogen ITC is not a responsibility of the validator.

3.2 Validation Criteria

Criteria that are specific to validation are summarised in the table below. The complete criteria used to validate the clean hydrogen project are described in the relevant documentation listed Section 1.5.1.

Table 3-1: Summary of Validation Criteria

| Criteria Element | Summary of Validation Criteria |

|---|---|

| Clean hydrogen project recognition |

The taxpayer’s project must:

|

| Clean ammonia recognition, if applicable |

If the taxpayer’s project is intended to produce clean ammonia, the project must satisfy other eligibility requirements under the ITA. The taxpayer must demonstrate:

See Section 5.2 for further guidance on adherence to these requirements. |

| Reasonableness of project design |

The assumptions, limitations, and methods for designing the process and for modelling and calculating the expected CI must be reasonable. A reasonable project design must,

|

| Expected CI calculation |

The expected carbon intensity of the hydrogen to be produced by the project must be

|

| Monitoring plan | The monitoring plan must enable future verification of the actual CI of the hydrogen produced in each operating year of the compliance period (see Section 3.3.2.4 for complete monitoring plan requirements). |

| Reporting | The validation information package must be complete (as per Section 3.3.2), consistent, and comprehensible. |

3.3 Pre-Validation

3.3.1 Validation Contract

Prior to the validation, the qualified validation firm and taxpayer must have a signed contract. The validation contract must include the following two provisions:

- The qualified validation firm will maintain records relevant to the validation services as laid out in Section 3.6.2

- In the event of an audit related to the administration of the Clean Hydrogen ITC by NRCan and/or CRA, the qualified validation firm will provide the records retained for review and will make themselves available for interview

Additionally, the recommended minimum information in an appropriate validation contract includes all the following:

- The type of engagement (validation)

- The objectives of the validation (to assess the reasonableness of the assumptions and methods used to calculate the expected CI and in the project’s design, and to ensure that the quantification and presentation of the expected CI value and validation information package conform to the validation criteria (Sections 1.5 and 3.2)

- The scope of the life cycle (cradle-to-gate) including the facilities, physical infrastructure, activities, technologies, and processes

- The point in time in the facility’s design that the validation occurs and the period for which the CI value is deemed to be appropriate

- The materiality used in the validation

Two critical aspects of the contract are: (1) the scope of the life cycle to be examined and (2) the materiality to be used as these define, to a large extent, the validator’s level of effort.

3.3.2 Validation Information Package – Documents Required for Validation

To adequately perform the validation, a validation information package must be provided to the validator by the taxpayer. A validation information package includes the following:

- Front-End Engineering Design (FEED) study or equivalent study (Section 3.3.2.1)

- Project Carbon Intensity Documents (Section 3.3.2.2)

- Ammonia Justification Documents (if applicable, see Section 3.3.2.3)

- Monitoring Plan (Section 3.3.2.4)

- Supporting Documents (Section 3.3.2.5)

Note that any of the above documents can be preliminary in nature at the validation stage. See Section 3.3.2.6 for further information on preliminary documentation.

3.3.2.1 FEED Study or Equivalent Study

For each clean hydrogen project, you must complete a Front-End Engineering Design (FEED) study or an equivalent engineering study and submit it as part of your clean hydrogen project plan submission. An equivalent engineering study would be an engineering package at the Front-End Loading 3 (FEL-3) stage or higher. Final detailed engineering designs should be submitted if they are ready at the time of validation information package preparation. Documents provided for the FEED (or equivalent) study must cover all elements relevant to the expected carbon intensity determination in the production of clean hydrogen and requirements of the clean hydrogen project plan, including, as applicable:

- The clean hydrogen production facility (including any on-site fuel or feed storage or preparation equipment)

- Any carbon capture, transportation, or storage equipment

- Any on-site clean hydrogen storage

- Any on-site clean hydrogen transportation infrastructure

- The clean ammonia production facility, applicable to clean hydrogen projects that produce clean ammonia

- Any infrastructure related to transportation of clean hydrogen between the hydrogen production facility gate and the ammonia production facility inlet, applicable to clean hydrogen projects that produce clean ammonia.

Table 3-2: Documentation Required for FEED Study or Equivalent Study

| Item Number | Document Name | Requirements |

|---|---|---|

| 1 | Design Basis and Process Description |

Documents should include

|

| 2 | Block Flow Diagrams (BFD) |

Block flow diagrams for the process presenting the major process and utility areas, and the interconnections between them, as well as

|

| 3 | Process Flow Diagrams (PFD) |

Standard engineering diagrams labelled according to standard engineering practices and presenting all, but not limited to

|

| 4 | Utility Flow Diagrams (UFD) |

Standard engineering diagram labelled according to standard engineering practices and presenting all, but not limited to

|

| 5 | Energy and Material Balances |

Energy and material balances for all streams shown in the PFDs and UFDs, including all, but not limited to

|

| 6 | Piping and Instrumentation Diagrams (P&ID) |

Standard engineering diagrams labelled with standard engineering symbols and notation, including all, but not limited to

|

| 7 | Legend and Symbol Sheets | Standard legend and symbol documentation providing details on engineering symbols and annotations (e.g., equipment symbol legends, piping specification keys) used in P&ID, PFDs, and UFDs. |

| 8 | Equipment and Instrumentation Documentation |

Documentation should include

|

| 9 | Electrical and Control Documentation |

Documentation should include

|

| 10 | Site and Plot Plans and General Arrangement Drawings |

Civil engineering diagrams and general arrangement drawings showing the location and plans for construction, such as

|

| 11 |

Itemized Class 3 Cost Assessment* * Cost assessment must be consistent with a Class 3 cost estimate, as outlined by the Association for the Advancement of Cost Engineering. |

This cost assessment will not be used by CRA for determination of equipment eligibility as it is strictly a part of the design package. An itemized list of costs that includes

|

| 12 | Level 3 Schedule |

A schedule that spans the whole project and includes all, but is not limited to

|

As part of the validation information package, the taxpayer must prepare a set of annotated drawings from the FEED (or equivalent) study to support the expected CI calculation.

The annotated drawings that support the expected CI calculation and that are included in the validation information package must include sufficient detail so that an individual, who is an engineer but otherwise not familiar with the process, would be able to identify the source of data in the validation information package that was used to populate the CH-ITC Workbook. To provide a clear trail from the FEED study or equivalent study to the CH-ITC Workbook, the taxpayer must follow the instructions below for preparing the requested diagrams for the FEED study or equivalent:

- Clearly label all locations on relevant diagrams that delineate the process boundary between the hydrogen product system (HPS) and other production system(s) (OPS), as well as the process boundaries between unit processes (UP) within the HPS (as applicable). The process boundaries must be delineated with coloured dashed lines (different colour for each system/process) that are distinct from any other labelling on each diagram.

- Clearly label each flow that is included in the CH-ITC Workbook Activity Map.

3.3.2.2 Project Carbon Intensity Documents

The taxpayer must submit the project carbon intensity documents listed in the following table as part of the validation information package.