Information Bulletin, June 2011

Taxation of Mineral Income 2012 – How Canada Compares

Context

Natural Resources Canada (NRCan) is releasing the results of a major upgrade of an international tax comparison that it carried out in 1993. The purpose of the original study was to refute allegations that Canada’s taxes on mining were not competitive internationally. At that time, most criticisms were directed at Canada’s high statutory tax rates. By computing average effective tax rates (AETR), the 1993 study demonstrated that Canada’s tax regimes for mining were competitive when the time value of tax credits and accelerated tax write-offs was taken into account. A 2003 update confirmed the competitiveness of Canada’s taxation regimes for mining.

Base-metal (copper, nickel, lead, zinc, and iron) mines supply commodities in very competitive markets. Accordingly, NRCan decided to focus its re-assessment of Canada’s tax competitiveness on base-metal mines. This is done by comparing the tax regimes of Canadian provinces and territories to that of major base-metal-producing jurisdictions on the basis of their average effective tax rates. The study also analyzes structural differences between Canadian tax regimes and that of foreign jurisdictions to find out where Canada differs from international norms.

Since 2003, Canadian jurisdictions have implemented tax rate reductions of a larger magnitude than any other major mineral-producing jurisdictions while retaining general corporate tax deductions and tax credits specific to the mining sector. As a result, the study indicates that Canada’s tax regimes for base-metal mining are among the most competitive in the world.

In the last few years, there has been an accelerated movement towards reforming ad valorem royalty regimes to make them more responsive to variations in commodity prices and profits. Some of these reforms have just now been completed (Republic of South Africa and Indonesia); Australia’s reform is ongoing, while several other countries are considering substantive changes. The outcome of these most recent developments could not be fully evaluated in the context of the study because the details of the reforms were not known at the time the analysis was carried out. However, it is clear that most of them involve the adoption of a variable royalty rate schedule applied to an ad valorem structure. Thus, the observations and conclusions of the study are believed to remain generally valid.

Methodology

- Tax models representing major mineral-producing jurisdictions are applied to a generic base-metal mine model to produce after-tax cash flows over the life of the mine.

- For the purposes of the discounted cash flow analysis, a discount rate of 7.5% is used for the base case. This is the measured historical weighted average cost of capital for the Canadian mining industry over a period of 20 years (1980-2000).

- Crown royalty charges that are specific to mining are treated as a tax instead of as an operating charge. However, social security, Medicare, unemployment taxes and other payroll charges, and wholesale or retail sales taxes are assumed to be imbedded in the cost structure of the project and are not considered in the tax calculations. Thus, the measured tax burden is the summation of federal and provincial (state) corporate income taxes, profit-sharing arrangements, capital taxes, and crown royalty charges where they apply.

- A ranking of jurisdictions is established based on calculated average effective tax rates, or AETR (see AETR section for details).

Important Notes

- While tax competitiveness is not the most important factor affecting investment decisions (the availability and accessibility of valuable mineral resources are prerequisites), its relevance stems from the fact that it is one of the determinants of investment profitability over which governments exert control.

- Tax competitiveness may be only one of the several policy objectives pursued by governments, and not necessarily the most important. Hence, the tax competitiveness position does not indicate overall performance of a tax regime or performance in respect of other policy objectives.

- Tax competitiveness is most relevant for marginally profitable projects; very profitable projects in a given jurisdiction may proceed even if they are taxed relatively more heavily than in other jurisdictions.

- Average effective tax rates are very sensitive to changes in parameters such as project financing, capital structure (tangible-intangible asset ratio), profitability, length of project life, discount rate used, etc. Comparative results are only valid, and should be interpreted, in the strict context of the assumptions of the financial models.

- Tax calculations are performed assuming that the operator is a single-mine company. To the extent that some jurisdictions (including Canadian) allow the consolidation of deductions from multiple mines owned by the same corporation, the tax burdens calculated for these jurisdictions in this study may be overstated relative to the ones that would be imposed in real life.

Jurisdictions Covered

The study covers nine Canadian jurisdictions: British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, the Northwest Territories, Nunavut, Ontario, Quebec, and the Yukon. For the purposes of calculating Quebec taxes, the mine project is assumed to be located outside the Gaspé region. While being important mineral-producing provinces, Alberta and Saskatchewan are not part of the study because their actual and expected base-metal production is relatively small. The Canadian contingent is compared to eleven foreign jurisdictions representing dominant and emerging base-metal producers, including Australia (South), Australia (Western), Chile, Indonesia, Mexico, Mongolia, Peru, the Republic of South Africa, Tanzania, and the United States (Alaska). While not being a base-metal producer, the United States (Nevada) was also included to represent the most lenient tax treatment of mining income that could possibly apply in any base-metal state in the United States.

Mine Model Assumptions

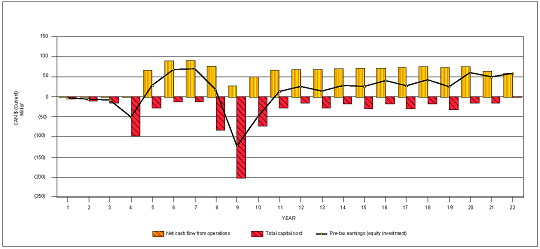

Generic mine models were developed to simulate the cash flow profile of base-metal mines yielding rates of return on investment (before tax and debt leverage) ranging from 5% to 30%. The mine models represent a mine that will be operating in the future for 18 years with 2012 being the initial project year and 2016 the first production year. Hence, tax parameters are applied based on rules and rates that, in January 2010, were known to be effective as of January 1, 2012. Metal (copper, for example) is extracted from an open pit for the first five years and then from underground workings for the rest of the mine life. Commodity prices are assumed to be constant over time in real terms. A 2% annual inflation rate is applied on all costs and revenues for tax calculation purposes. Fifty percent of the pre-production capital expenditures are financed by debt. The base case, a mine with a real internal rate of return (IRR) before tax and debt leverage of 15%, is represented in Figure 1. Variations in profitability are modelled by simulating changes in gross revenues and/or changes in operating costs.

How Average Effective Tax Rates (AETR) Are Constructed and What They Mean

- As any taxpayer knows, the timing of a tax payment is an important financial factor. This is why AETR are calculated using discounted cash flow (DCF) analysis.

- DCF analysis is a method of valuing a project (or an asset) using the concept of the time value of money. This concept recognizes that an amount of money received or paid immediately has more value than the same amount received or paid at a future date. The time value of money, or discount rate, varies among individuals and organizations depending on, among other things, their opportunity cost of capital. For a specific mining project, for example, all future cash flows are estimated and discounted using the discount rate selected by the investor to give their present values (PVs). The sum of the present values of all future cash flows, both incoming and outgoing, is the net present value (NPV), which is taken as the value, or price, of the project in question.

- AETR are defined as the NPV of all taxes payable during the entire life of the mine, divided by the NPV of all yearly net income before tax, expressed as a percentage.

- The net income of any given year is defined as operating revenue, less operating expense, less total capital cost (including interest charges) amortized using the units-of-production depreciation method.

- Effective versus statutory tax rates: By construct, AETR are set to give a tax rate value that is adjusted by the size and timing of actual tax payments over the life of a project. When the tax bases of all taxes taken into account are equal to accounting income, measured AETR are equal to the sum of the statutory tax rates in question. AETR that are lower than statutory rates indicate that yearly tax bases are actually smaller, or delayed, relative to accounting income. Conversely, AETR higher than statutory tax rates indicate yearly tax bases that are larger or that are taken into account earlier than accounting income.

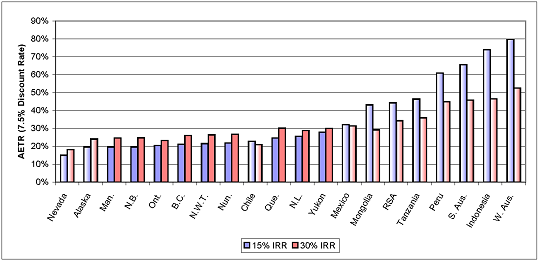

Comparative Results for the Base Case and a High Profitability Case

Comparative results are shown in Figure 2 for both the base case (15% IRR) and a more profitable mine (30% IRR). Jurisdictions are ranked using the AETR results of the base case, for which the relative tax burden is more likely to be a significant determinant for an investment decision. In this case, Canada, the United States, and Chile obtain very similar results and are the most tax-competitive jurisdictions. For the more profitable mine scenario, these three countries still impose the lowest tax burden, but this advantage over other countries is reduced relative to the base case. It is interesting to note that all Canadian jurisdictions fall in a narrow range of results, with six out of nine jurisdictions differing by less than three percentage points for the base case. They also compare well against Nevada which, although not a base-metal producer, has the most lenient tax treatment of mining income in the United States.

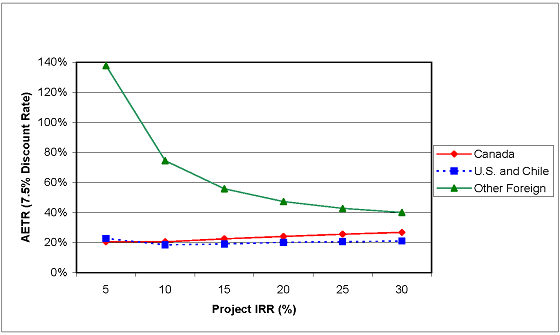

How AETR Vary With Project Profitability

The tax regimes under review are structured in ways that have strikingly different effects on how the tax burden varies with project profitability. As illustrated in Figure 3, there are three different groups based on how AETR behave according to profitability. Canadian tax regimes were found to be slightly progressive (AETR increase with profitability). Regimes in the United States and Chile were found to be neutral (AETR remain relatively constant at all levels of profitability), and that of other countries were found to be regressive (AETR decrease with profitability).

The timing of income tax write-offs and the extent to which royalty regimes are profit-based are the main determinants of the observed differences. For mines operating in Canada, a unique combination of accelerated income tax write-offs and profit-based royalties results in tax payments being deferred to a larger extent, and royalty bases incorporating more deductions of capital expenditures than for mines operating anywhere else. Tax deferrals and additional tax deductions represent a higher proportion of project cash flow (and therefore taxes payable) for marginally profitable projects than for very profitable ones; this, combined with Canada’s profit-based royalty regimes, explains why Canadian jurisdictions were the only ones found to be moderately progressive.

It is interesting to note that Canadian tax regimes remain competitive with other tax regimes at all levels of profitability, but more so when profitability is lower.

Unsurprisingly, higher discount rates increase the value of tax savings realized as a result of accelerated deductions. Hence, the study found that AETR variations to a change in discount rates were inversely proportional to the extent of tax deferrals resulting from accelerated deductions. The greater the tax deferrals in a given tax regime, the more the corresponding AETR will decrease with the application of a higher discount rate. For example, the AETR for Quebec (where deductions are most accelerated) decreases from 28% to 17.9% (a 36% drop) when the discount rate goes from 5% to 15%. In contrast, the AETR for Newfoundland and Labrador (where deductions are accelerated to a lesser extent) decreases from 27.8% to 21.5% (a 23% drop) for the same variation in the discount rate.

More Details About How Canada Compares

At the income tax level, Canada is the only country covered in the study that provides corporate income tax credits for exploration and development expenses, and for capital assets used by the mine in certain locations. Canada is also unique in allowing a 100% immediate write-off for all pre-production expenses, subject to availability of income. In all other jurisdictions, pre-production expenses have to be deducted over several years, and many jurisdictions require such deductions to be taken over the entire life of the project. Overall, Canada’s income tax regimes provide write-offs that are as fast as, or faster than, all other countries under study for all categories of mine expenditures.

In the country sample, only Canada and the United States (Alaska) have pure profit-based royalties. For the most part, other countries have ad valorem royalties, or variations thereof.Footnote 1

Based on the evidence of recent years, Canadian royalty regimes were found to be less subject to major changes or review than those of most other countries. Canadian profit-based royalties are undoubtedly more complex than ad valorem ones, but they are intrinsically more stable since they do not require any adjustments to take significant variations in commodity prices and profit into account.

Canadian tax regimes are competitive with those of Chile and the United States, with average effective tax rates that are well below (less than 30% of pre-tax income) those of other mineral-producing jurisdictions (generally more than 40% of pre-tax income).

Conclusions

As noted previously, the model makes several important assumptions (for example, that the operating environment and cost structure are similar across all jurisdictions and that the operator is a single-mine company). Within this context, Canada’s tax regimes for mining are competitive, particularly at moderate profitability levels where the tax take may be an important determinant of investment decisions.

Canada’s tax regimes do not penalize marginally profitable projects. Others (except the United States and Chile) tend to do so, to the point they may even prevent the bringing into production of marginally profitable projects or force project closure during severe cyclical downturns.

While Canada’s tax burden increases with mine profitability, the tax take remains similar to that of the United States and Chile and is comparatively smaller than for other countries, even for highly profitable projects.

| Jurisdiction | 2003 | 2012 (as of January 2010) | ||

|---|---|---|---|---|

| Combined Corporate Income Tax Rate | Mining Royalty Rate | Combined Corporate Income Tax Rate | Mining Royalty Rate | |

| British Columbia | 42.62% | 13%a | 25% | 13%a |

| Manitoba | 45.62% | 18%a | 27% | 10-17%a |

| New Brunswick | 45.12% | 16%a | 25% | 16%a |

| Newfoundland and Labrador | 43.12% | 15% on 80% of taxable income and 20% on remaining 20%a | 29% | 15% on 80% of income and 20% on remaining 20%a |

| Northwest Territories | 43.12% | 13%a | 26.5% | 13%a |

| Nunavut | 43.12% | 13%a | 27% | 13%a |

| Ontario | 40.12% | 12%a | 25% | 10%a |

| Quebec | 38.02% | 12%a | 26.9% | 16%a |

| Yukon | 44.12% | 13%+a | 30% | 12%a |

| Australia (South)d | 30% | 3.5%b | 30% (29% from 2013) | 3.5% b |

| Australia (Western)d | 30% | 5%b | 30% (29% from 2013) | 5%b |

| Chile | 16.5% | n.a. | 20% (17% from 2013) | 9%c |

| Indonesiae | 30% | 4%b | 25% | 4%b |

| Mexico | 34% + 10% profit sharing | n.a. | 30% + 10% profit sharing | n.a. |

| Mongolia | 30% | 2.5%b | 25% | 5%b |

| Peru | 27% + 8% profit sharing | 3%b | 30% + 8% profit sharing | 3%b |

| Republic of South Africa (RSA)f | 30% | 2%b | 28% | 2%b |

| Tanzania | 30% | 3%b | 30% | 3%b |

| USA (Alaska) | 44.4% | 10%a | 44.4% | 10%a |

| USA (Nevada) | 35% | n.a. | 35% | n.a. |

Notes:

a Profit-based royalty.

b Ad valorem royalty.

c Ad valorem royalty, but rate varies according to gross margin.

d Australia is proposing the implementation of a profit-based federal royalty that would allow a deduction for state royalty payments. To date, the proposed reform is not intended to apply to nonferrous metal mines.

e Indonesia is introducing a 10% profit-based royalty for new projects as a replacement for the 4% ad valorem; since details on allowed deductions were not known at the time of the analysis, the new regime could not be evaluated.

f RSA is introducing a royalty with a rate varying according to a formula pegged to a ratio of earnings before interest and tax (EBIT) to gross receipts.

Figure 1

Base-Case Project Cash Flow Before Tax and Debt Leverage

Figure 2

Average Effective Tax Rates for Projects With 15% and 30% IRR

Figure 3

Average Effective Tax Rates Across a Range of Profitability

© Her Majesty the Queen in Right of Canada, 2011

Page details

- Date modified: